Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

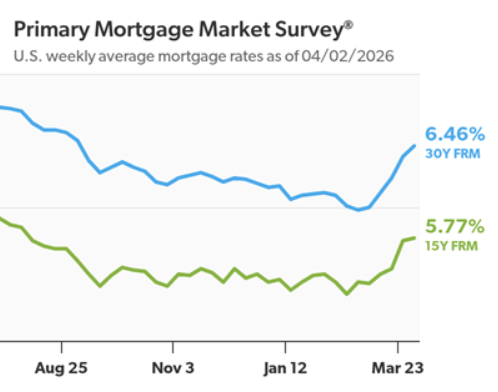

30-Year Mortgage Rate Averages 6.46%

Freddie Mac today released the results of its Primary Mortgage Market Survey® (PMMS®), showing the 30-year fixed-rate mortgage (FRM) averaged 6.46%.

“The 30-year fixed-rate mortgage edged up, averaging 6.46% this week,” said Sam Khater, Freddie Mac’s Chief Economist. “With spring homebuying season in full swing, aspiring buyers should remember to shop around for the best mortgage rate, as they can potentially save thousands of dollars by getting multiple quotes.”

- The 30-year FRM averaged 6.46% as of April 2, 2026, up from last week when it averaged 6.38%. A year ago at this time, the 30-year FRM averaged 6.64%.

- The 15-year FRM averaged 5.77%, up from last week when it averaged 5.75%. A year ago at this time, the 15-year FRM averaged 5.82%.

The PMMS® is focused on conventional, conforming, fully amortizing home purchase loans for borrowers who put 20% down and have excellent credit.

Before You Fall in Love with a House, Do This First.

Be honest. Have you started looking at homes online yet? If you have, it’s already time to get pre-approved. Because here’s what not enough people know.

If buying a home is on your radar – even if it’s more of a someday plan than a right now plan – you don’t want to wait until later on in the process to tackle this step.

No matter what you’ve heard, pre-approval isn’t about commitment. It’s about clarity.

And here are the two big ways pre-approval sets you up for success.

You Know Your Numbers Up Front

During the pre-approval process, a lender will walk through your finances and tell you what you can borrow based on your income, debts, credit score, and more. And once you have that number, your search becomes a lot more focused.

With a mortgage pre-approval, you know what you can borrow, so it’s easier to figure out your ideal price point, and what you can actually afford. And that clarity is key.

Because if you just start browsing online and just guess at your price point, you run the risk of falling for a house that’s outside of your price range – or missing out on ones that aren’t.

You want this number to be clearly defined before your search. Here’s why.

You Can Move Quickly When You Find the One

This is how a lot of home searches go today. You scroll through listings just to see what’s out there, and then it happens. You fall in love with something you’ve seen online.

If you’re already pre-approved? You’re probably in great shape.

But if you’re not…

Instead of being able to jump on that house and quickly make an offer, you have to scramble to get a lender, gather the financial documents, and then submit the necessary pre-approval paperwork first. And while you’re waiting to hear back from your lender, someone else who’s more prepared could beat you to the house. As Bankrate explains:

“The best time to get a mortgage preapproval is before you start looking for a home. If you find a home you love but don’t have a preapproval in hand, you likely won’t have time to get preapproved before you need to make an offer . . .”

And that’s avoidable, with the right prep.

Because while you can’t control when the right home shows up, you can be ready for it. Think of it like showing up to the starting line with your shoes tied and your warm-up done – while everyone else is still looking for parking.

It’s not about rushing your timeline. It’s about removing the delay between finding the right home and being able to move on it.

One Thing You Need To Know About Pre-Approvals

Speaking of timing, pre-approvals do have an expiration date. So, be sure to ask your lender how long it’s good for. The Mortgage Reports explains:

“Mortgage preapproval letters are typically valid for anywhere from 30 to 90 days. However, a preapproval can be updated and extended if the lender re-checks your information.”

Doing the right prep and knowing this information can make the whole process a lot smoother.

You don’t have to be ready to buy to be ready to buy.

Getting pre-approved doesn’t mean you’re committing to buy right now. It just means you’ve taken a step to understand your numbers. And when a home catches your attention, you’re prepped and good to go.

Bottom Line

Ask yourself this: if your perfect home popped up tomorrow, would you be ready to make a move?

If the answer is no and you want to buy, it may be time to get pre-approved. You don’t feel behind before your search even officially kicks off.

Will This Change What You Think About Investors in Today’s Housing Market

There’s a lot of noise out there right now about investors in the housing market.

Some headlines make it sound like big Wall Street firms are buying up everything in sight. And if you’re trying to purchase a home yourself, that can make it feel like the odds are stacked against you.

But when you take a closer look at the data, a very different picture starts to come into focus.

Most Investors Are Just Everyday Owners

For starters, when you hear the word investor, you probably picture big corporations. And that misconception is a large part of what’s feeding into the myth that they’re buying up all the homes.

Most investors aren’t big companies, at all.

They’re everyday people just like you.

They’re someone who owns a second home (like a vacation house at the river), a neighbor who has 1 or 2 rentals, or even a homeowner who tried to sell their home, didn’t get the price they wanted, and decided to rent it instead.

And when all of these groups are lumped together in the headlines, the number of investors sounds high – especially if you’re operating under the assumption all investors are big investors.

But here’s what the numbers really show when you drill down.

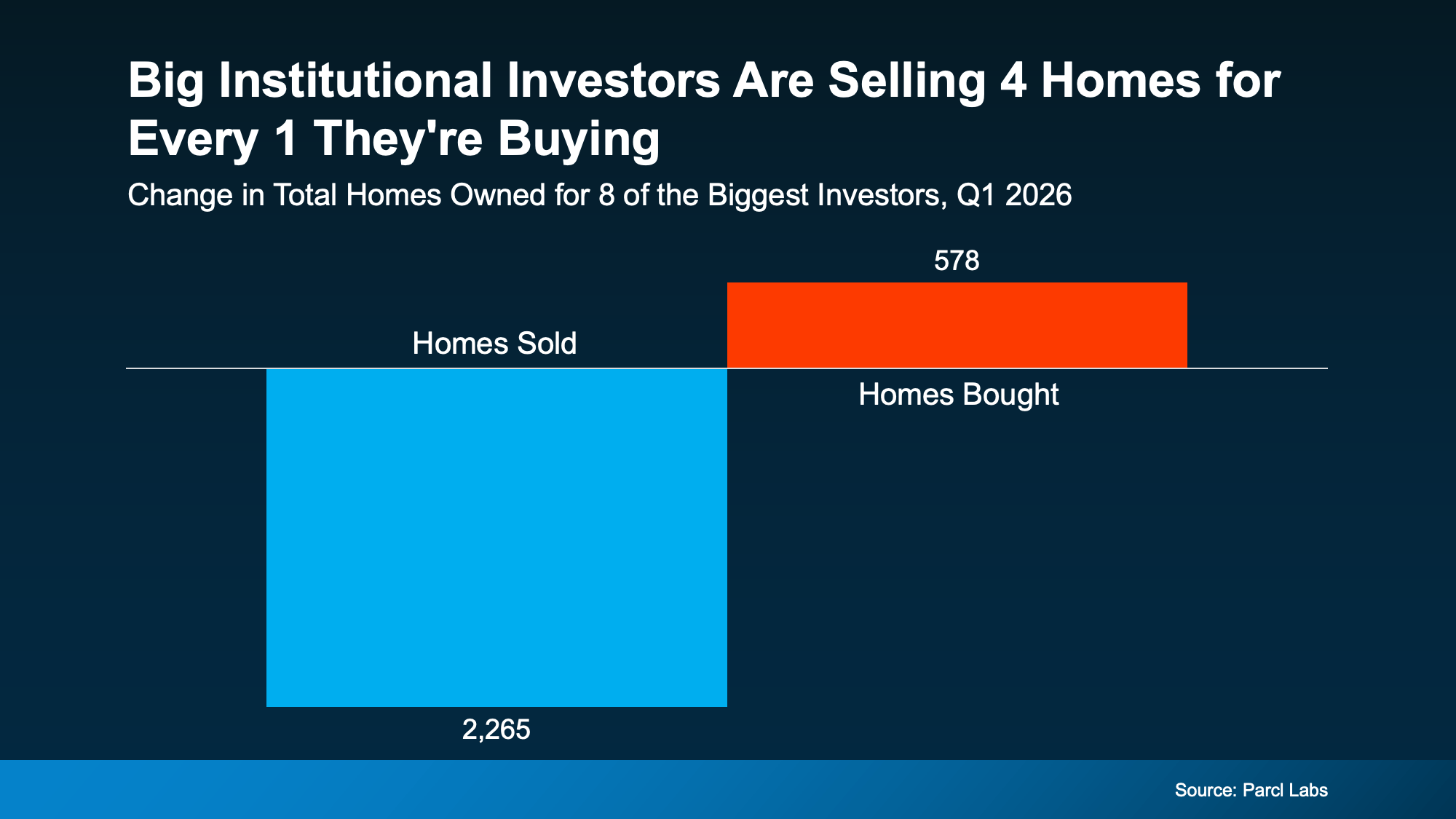

Institutional Investors Are a Small Slice of the Housing Market

Large institutional investors, those big companies buying homes, actually make up a very small share of the overall housing market.

According to BatchData, the largest investors (those with 1,000+ homes) own just 0.4% of the 86 million single-family homes in the country. And their share of the market is actually shrinking.

Data from Parcl Labs shows big investors are selling 4 homes for every 1 they’re buying right now (see visual below):

That means they’ve actually added almost 1.7k homes back into the market lately.

That means they’ve actually added almost 1.7k homes back into the market lately.

What This Means for You

The story is clear. Instead of aggressively buying up homes, most of these companies are stepping back, which means less competition from them than you might expect. If you were someone who thought they were dominating the market, let that give you some peace of mind.

Most of the competition you’ll face is from other everyday buyers – people just like you. And with most large investors stepping back, there may be more opportunity in the market than you think.

Bottom Line

It’s easy to assume big investors are taking over the housing market, but the data tells a different story. If you want an expert’s opinion on what investor activity looks like in our area, let’s talk.

Because odds are, it’s not as big a factor as you may think.

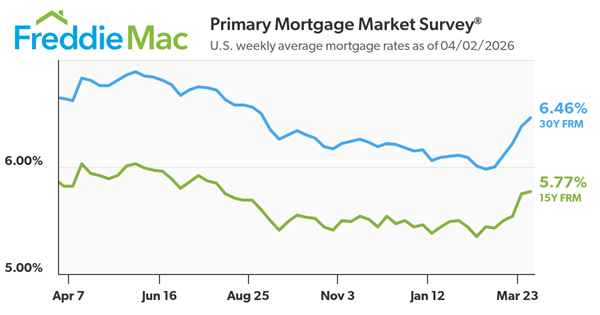

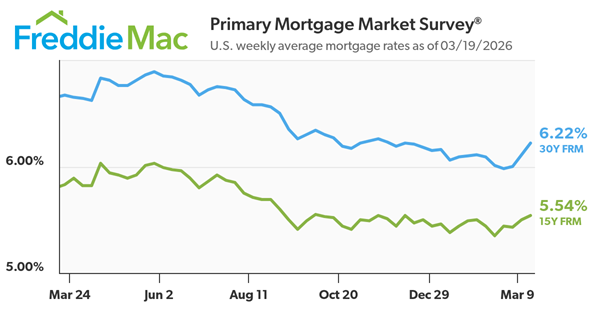

30-Year Mortgage Rate Averages 6.38% For The Week

Freddie Mac (OTCQB: FMCC) today released the results of its Primary Mortgage Market Survey® (PMMS®), showing the 30-year fixed-rate mortgage (FRM) averaged 6.38%.

“Mortgage rates this week averaged 6.38%,” said Sam Khater, Freddie Mac’s Chief Economist. “The housing market continues to show gradual improvements compared to a year ago amid recent rate volatility. Purchase and refinance applications are up year-over-year, and rates remain lower than last year when they averaged 6.65%.”

- The 30-year FRM averaged 6.38% as of March 26, 2026, up from last week when it averaged 6.22%. A year ago at this time, the 30-year FRM averaged 6.65%.

- The 15-year FRM averaged 5.75%, up from last week when it averaged 5.54%. A year ago at this time, the 15-year FRM averaged 5.89%.

The PMMS® is focused on conventional, conforming, fully amortizing home purchase loans for borrowers who put 20% down and have excellent credit.

When’s The Best Week To List Your House?

When’s The Best Week To List Your House? It’s Just Around the Corner!

While the Spring season consistently offers up some of the best conditions for home sellers, Realtor.com says there’s one window where the stars really seem to align year after year. And it’s coming up fast.

Based on their analysis of historical trends, the ideal week to put your house on the market this year is: April 12–18.

And here’s why this window stands out as being particularly seller-friendly:

- Buyers Are More Active. According to the research coming out of Realtor.com, homes listed during this week typically get about 16.7% more views than in a normal week. And in a market where buyers have options, getting that extra attention can set the tone for your entire sale.

- Sales Happen Faster. Realtor.com also explains the added demand from buyers sets you up for a faster process. While homes have been taking longer to sell lately, homes up for sale this week were on the market for 17% less time than usual. And that’s a difference you’ll be able to feel.

- A Better Price for Your House. Since the number of homes for sale has grown, it’s normal for buyers to ask for credits, repairs, and price adjustments today. But, during this early Spring window, about 18.9% fewer homes do a price cut. That gives you a better chance of getting your full asking price.

- More Profit in Your Pocket. According to the study, well-prepped homes listed this week can command a price that’s about $5,300 more than the average week (and $26,000 more than homes at the start of the year).

And what seller doesn’t want more eyes on their house, getting an offer in hand sooner (rather than later), and their best shot at selling for top dollar?

What You Need To Do To Get Ready

If you’re already thinking about selling and you want to take advantage of this sweet spot, your next step is shockingly simple. Just talk to a local agent.

Their expertise on your area is going to be key over the next few weeks. Because these trends are going to vary by state, city, and even neighborhood. And your agent will use that insider knowledge to help you figure out what you need to do now to get your house ready. Including:

- What you’ll want to spruce up before listing

- How to prioritize any repairs (and contractors that can help)

- Quick wins that’ll have a big impact

- What buyers care most about today

For some sellers, that’s a few easy fixes they can knock out in the next couple of weeks. A fresh coat of paint. Some new mulch. Or some light Spring cleaning.

For others, it’s worth taking another month or so to make some minor updates before listing. And that’s okay. Because while this mid-April window may give sellers an advantage, it’s not your only opportunity to sell.

Zillow says the best time to list is in May. And that means the golden window for sellers isn’t closing after this one week. It’s open all season long.

Bottom Line

Getting your house on the market in mid-April may give you an extra edge, but the bigger opportunity is the Spring season as a whole. The real question is:

Do you know what you need to do before you can list?

Because it’s officially go-time for any seller planning a Spring move.

If you want your house to hit the market this week (or even this season), let’s talk about what it’ll take to get it ready.

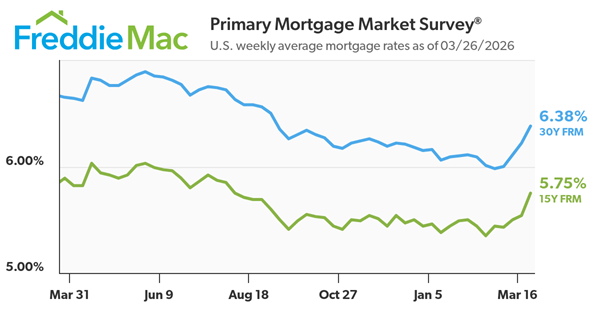

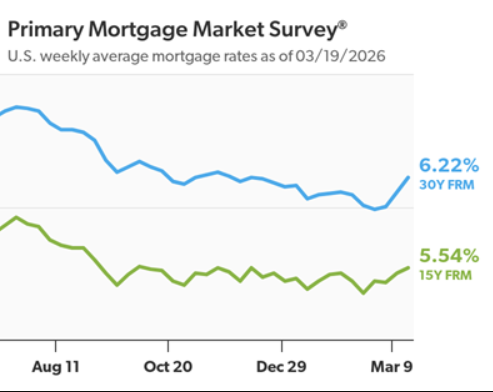

Mortgage Rates Average 6.22% For The Week

Freddie Mac (OTCQB: FMCC) today released the results of its Primary Mortgage Market Survey® (PMMS®), showing the 30-year fixed-rate mortgage (FRM) averaged 6.22%.

“The 30-year fixed-rate mortgage edged up this week to 6.22% but remains nearly half a percentage point lower than the same time last year,” said Sam Khater, Freddie Mac’s Chief Economist. “Potential homebuyers are poised for a more affordable spring homebuying season than last with the market experiencing improvements in purchase applications and pending home sales.”

- The 30-year FRM averaged 6.22% as of March 19, 2026, up from last week when it averaged 6.11%. A year ago at this time, the 30-year FRM averaged 6.67%.

- The 15-year FRM averaged 5.54%, up from last week when it averaged 5.50%. A year ago at this time, the 15-year FRM averaged 5.83%.

The PMMS® is focused on conventional, conforming, fully amortizing home purchase loans for borrowers who put 20% down and have excellent credit.

Must-Do’s for First-Time Home Buyers

Buying your first home is exciting, but it can also be a little nerve-wrecking because it’s something you’ve never done before. And trying to think of everything you need to do can feel like a lot. But here’s the key.

You don’t have to figure everything out on your own. And you don’t have to do it all at once. Just tackle it one thing at a time.

Here’s a simple list of 3 main things you should focus on to help you get started.

1. Assemble Your Team: Don’t Do This Alone

Buying a home is a team sport. And having the right professionals by your side can make a world of difference. Here’s who you need to find:

- A local real estate agent is your guide from the first showing to closing day. They’ll make sure you understand all the details along the way, so you feel confident in your decision.

- A trusted lender will walk you through loan options, monthly payments, and what’s realistic for your situation. That information is something you’re going to want early on.

2. Prep Your Finances: Set the Foundation First

This is what determines what you can afford, how competitive you’ll be, and how confident you’ll feel when it’s time to make an offer. Here’s how to get ready:

- Check your credit score. Your credit score impacts the loan options you’ll qualify for and even the mortgage rate you’ll get. Knowing this number early gives you time to work on raising your score, if you want to.

- Save for your down payment and closing costs. Most buyers focus on the down payment, but closing costs matter too. Having savings set aside for both helps you avoid last-minute stress and surprises.

- Look into assistance programs. Many first-time buyers qualify for programs that’ll give their homebuying savings a boost. This can make buying possible sooner than you expect.

- Talk to a lender about mortgage options. Fixed-rate, adjustable-rate, FHA, VA, and conventional loans all work differently. Understanding the options helps you choose what fits your goals best.

- Get pre-approved. A pre-approval tells you what a lender would be willing to give you for your home loan. This’ll help you figure out your price range and set you up to move fast when the right home comes along.

- Figure out your budget. Your mortgage is just one part of homeownership. Budgeting for your utilities, home insurance, and everyday expenses and maintenance will help make sure your payment feels comfortable, not stressful.

3. Gather Your Documents: Save Time (and Stress)

When you’re officially ready to kick off the buying process, lenders are going to need to verify your income, assets, and financial history. Having these documents ready-to-go upfront can speed up the process and reduce back-and-forth. Here’s what Bankrate says you need to prep:

- W-2s and tax documents (past 2 years). These show income stability and help

- Recent pay stubs (generally the past 1–2 months). Pay stubs confirm your current income and employment status.

- Bank statements (past 2–3 months). These show your savings, spending patterns, and where your down payment funds are coming from.

- Investment account statements (past 2-3 months). If you’re using investments as part of your financial picture, lenders may ask for these as well.

- Copy of your driver’s license. This verifies your identity and is required for loan processing.

- Residential history (past 2 years). Lenders use this to confirm stability and background information.

- Statements for any outstanding debts (past 2 months). Student loans, auto loans, and credit cards affect your debt-to-income ratio, so lenders will want to know about them.

- Proof of supplemental income. Bonuses, commissions, side work, or child support may count toward your income if documented properly.

Note: the exact time frames and list of documents may vary lender to lender. This is just a general rule of thumb to help you get the ball rolling.

Bottom Line

Buying your first home doesn’t mean you have to have everything figured out. It just requires a plan.

If you start with your finances, organize your documents, and surround yourself with the right people, you’ll be in great shape when the time comes to make a move.

And if you want more information on anything in this list or just need help getting started, don’t hesitate to reach out.

Why Buyers Walk Away

The #1 Reason Buyers Walk Away (And How To Get Ahead of It)

You may have seen headlines on social saying the number of buyers backing out of their contracts is on the rise – and has recently reached a high not seen since 2017. That can sound intimidating. But it varies a lot by market.

And here’s the key thing to understand if you want to sell. A lot of the time, there’s one common cause. And it’s something you can actually control.

Here’s what you can do to get ahead of the biggest dealbreaker before it ever becomes a problem.

The Top Dealbreaker: Issues That Pop Up During the Inspection

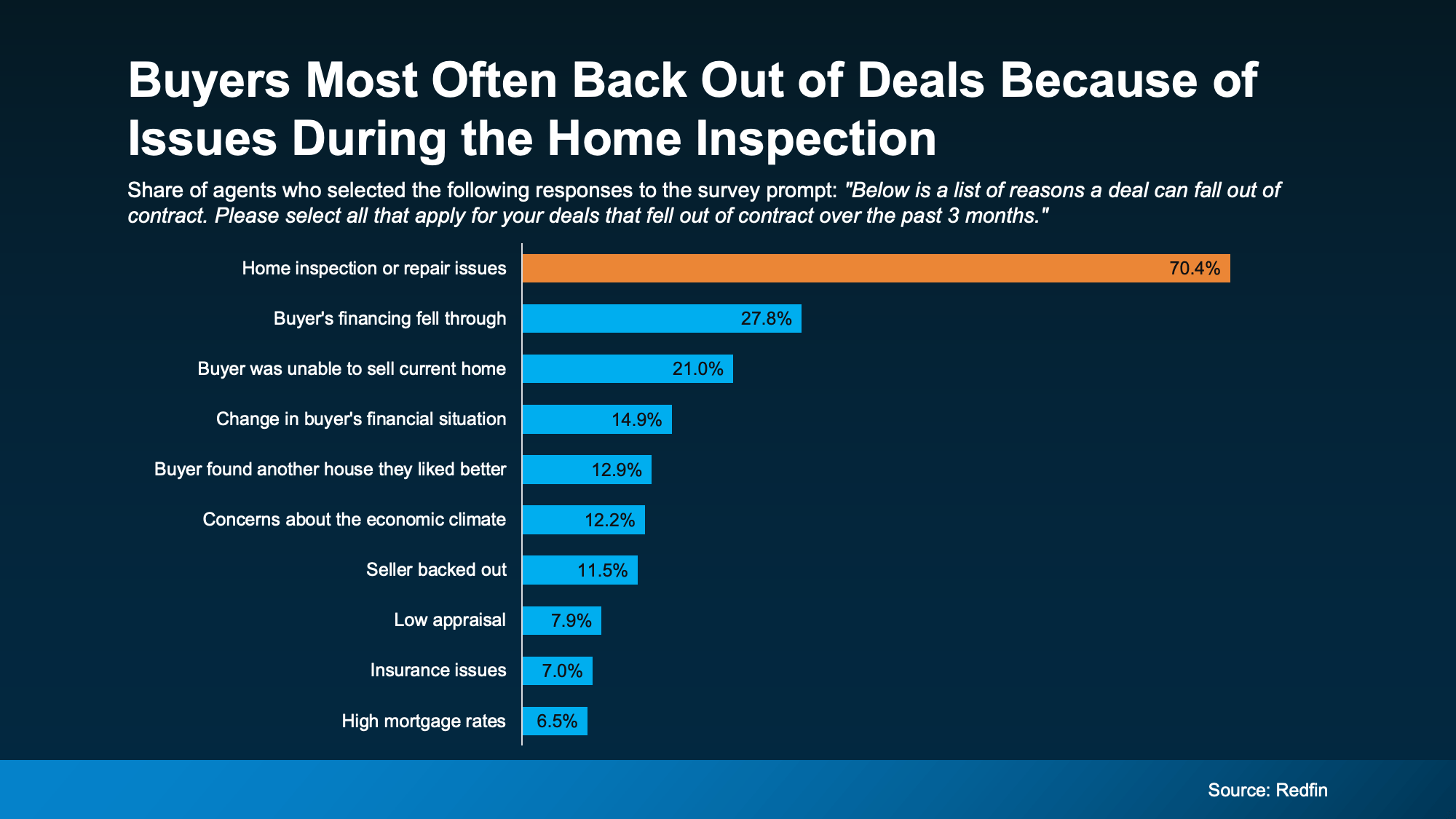

A Redfin survey shows over 70% of recently cancelled contracts happened because of issues during the home inspection (see graph below):

And that makes sense. Because today’s buyers have something they didn’t have a couple of years ago: options.

And that makes sense. Because today’s buyers have something they didn’t have a couple of years ago: options.

Why Fixing Things Before You List Matters More Today

A few years back, when buyers felt rushed or boxed in due to the limited number of homes for sale, they were more willing to overlook issues.

But in today’s market, skipping essential repairs is one of the fastest ways to lose a deal.

Now that there are more homes to choose from, buyers can be more selective. If a house feels risky, outdated, or like it’s hiding expensive surprises, they’re a lot more likely to walk away. So, what do you have to fix? Just ask an agent.

How Your Agent Can Help Give You the Edge

A local agent will be able to walk through your house and offer advice on what to tackle based on your specific home, your market, and what buyers are prioritizing in your area. They’ll also have first-hand knowledge about some of the biggest turnoffs for buyers today. And you can use that expertise to prevent future headaches.

For example, according to Zillow, these are some of the issues buyers will care the most about:

- Roof leaks or damage: sagging, leaking, etc.

- Plumbing problems: standing water, leaks, water damage, etc.

- Electrical concerns: outdated or exposed wiring, missing GFCI outlets, etc.

- HVAC issues: non-functioning units

- Pest or insect damage: termite colonies, etc.

- Hazardous materials: lead, mold, asbestos, etc.

- Safety/code violations: missing smoke detectors, windows stuck closed, etc.

- Structural problems: cracks in the foundation, sagging floors, etc.

Odds are not all of this even applies to your house. Maybe only 1-2 things do. Or maybe none of them do. It just depends. But an agent will have the tools and resources to help you figure it out and stay one step ahead.

The Benefits of a Pre-Listing Inspection

To buyers, these aren’t cosmetic issues. They’re trust issues. And that’s what you need to watch out for today. Once buyers start wondering “what else might be wrong,” it’s hard to recover momentum.

That’s why some agents are even recommending a pre-listing inspection as a sneak peek into what buyers will see on their own inspection. With that insight, you can:

- Fix concerns before you list, or disclose issues upfront

- Avoid having to respond or negotiate under pressure

- Stop scrambling to find contractors with availability before your closing date

But remember, you don’t have to fix everything. You just have to be strategic about what you do tackle, so you and your buyer aren’t caught off guard.

And that’s why you need an agent who can:

- Decide if a pre-listing inspection is worth it where you live

- Recommend a trusted inspector (if you decide to get one)

- Look at the results with you to identify true dealbreakers in your market

- Help you decide what to fix or what to credit

- Make sure you avoid over-spending or under-preparing

Bottom Line

One of the biggest dealbreakers for buyers today is inspection issues – and that’s something you can control. You just need to be proactive about high-impact repairs before you list.

If you want help figuring out where to focus, let’s connect so we can keep your sale on track from day one.