“Mortgage rates remain near their lowest levels in three years, which is encouraging for potential homebuyers who have waited to enter the market for some time,” said Sam Khater, Freddie Mac’s Chief Economist. “Lower rates, combined with strong income growth, have led to a steady increase in purchase applications compared to last year. We’re also seeing more homeowners refinancing their mortgages to benefit from these lower rates, as shown by the rise in refinance applications over the past year.”

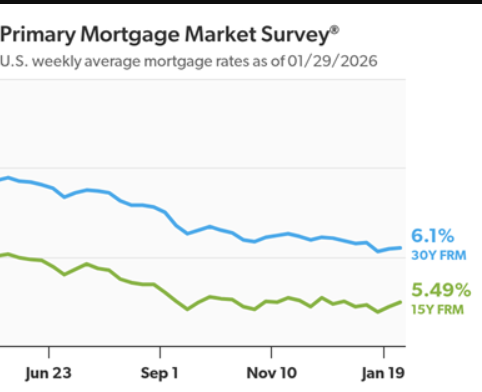

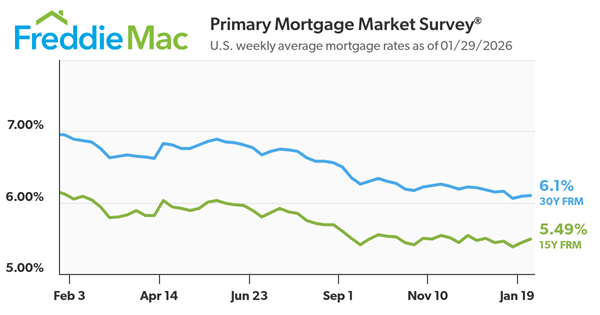

The 30-year FRM averaged 6.10% as of January 29, 2026, up slightly from last week when it averaged 6.09%. A year ago at this time, the 30-year FRM averaged 6.95%.

The 15-year FRM averaged 5.49%, up from last week when it averaged 5.44%. A year ago at this time, the 15-year FRM averaged 6.12%.

The PMMS® is focused on conventional, conforming, fully amortizing home purchase loans for borrowers who put 20% down and have excellent credit.

“With the economy improving and the average 30-year fixed-rate mortgage nearly a percentage point lower than last year, more homebuyers are entering the market,” said Sam Khater, Freddie Mac’s Chief Economist. “Buyers always should shop around for the best rate, as multiple quotes can potentially save them thousands.”

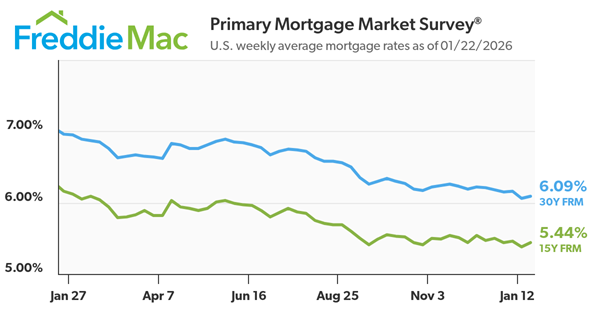

The 30-year FRM averaged 6.09% as of January 22, 2026, up from last week when it averaged 6.06%. A year ago at this time, the 30-year FRM averaged 6.96%.

The 15-year FRM averaged 5.44%, up from last week when it averaged 5.38%. A year ago at this time, the 15-year FRM averaged 6.16%.

The PMMS® is focused on conventional, conforming, fully amortizing home purchase loans for borrowers who put 20% down and have excellent credit.

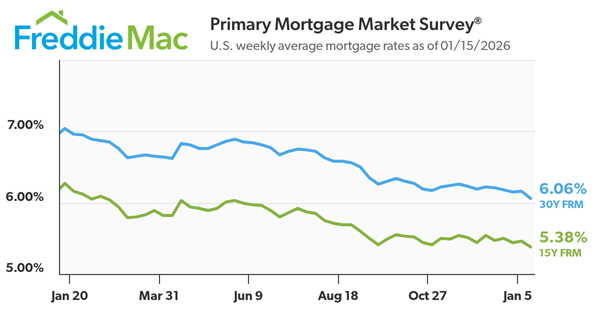

“Late last week, mortgage rates dropped, driving the weekly average down to its lowest level in more than three years,” said Sam Khater, Freddie Mac’s Chief Economist. “The impacts are noticeable, as weekly purchase applications and refinance activity have jumped, underscoring the benefits for both buyers and current owners. It’s clear that housing activity is improving and poised for a solid spring sales season.”

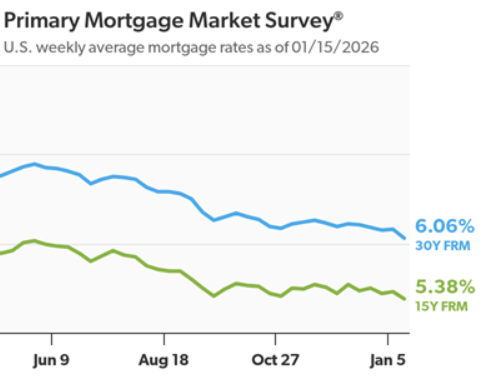

The 30-year FRM averaged 6.06% as of January 15, 2026, down from last week when it averaged 6.16%. A year ago at this time, the 30-year FRM averaged 7.04%.

The 15-year FRM averaged 5.38%, down from last week when it averaged 5.46%. A year ago at this time, the 15-year FRM averaged 6.27%.

The PMMS® is focused on conventional, conforming, fully amortizing home purchase loans for borrowers who put 20% down and have excellent credit

Would-be homebuyers aren’t sitting on the sidelines because they don’t want to buy. They’re sitting out because they think they can’t. And sometimes, it’s their credit score that’s holding them back.

According to a Bankratesurvey, 2 out of every 5 (42%) Americans believe you need excellent credit to qualify for a mortgage. That may be why, when renters are asked why they don’t own yet, “my credit isn’t good enough” comes up often.

Maybe you’re in the same boat. You look at your score, see it’s not where you want it to be, and assume buying your first place just isn’t realistic right now.

But here’s what you need to know.

Even though a lot of people assume you need flawless credit to buy a house, that’s not necessarily the case.

You Don’t Need Perfect Credit To Buy a Home

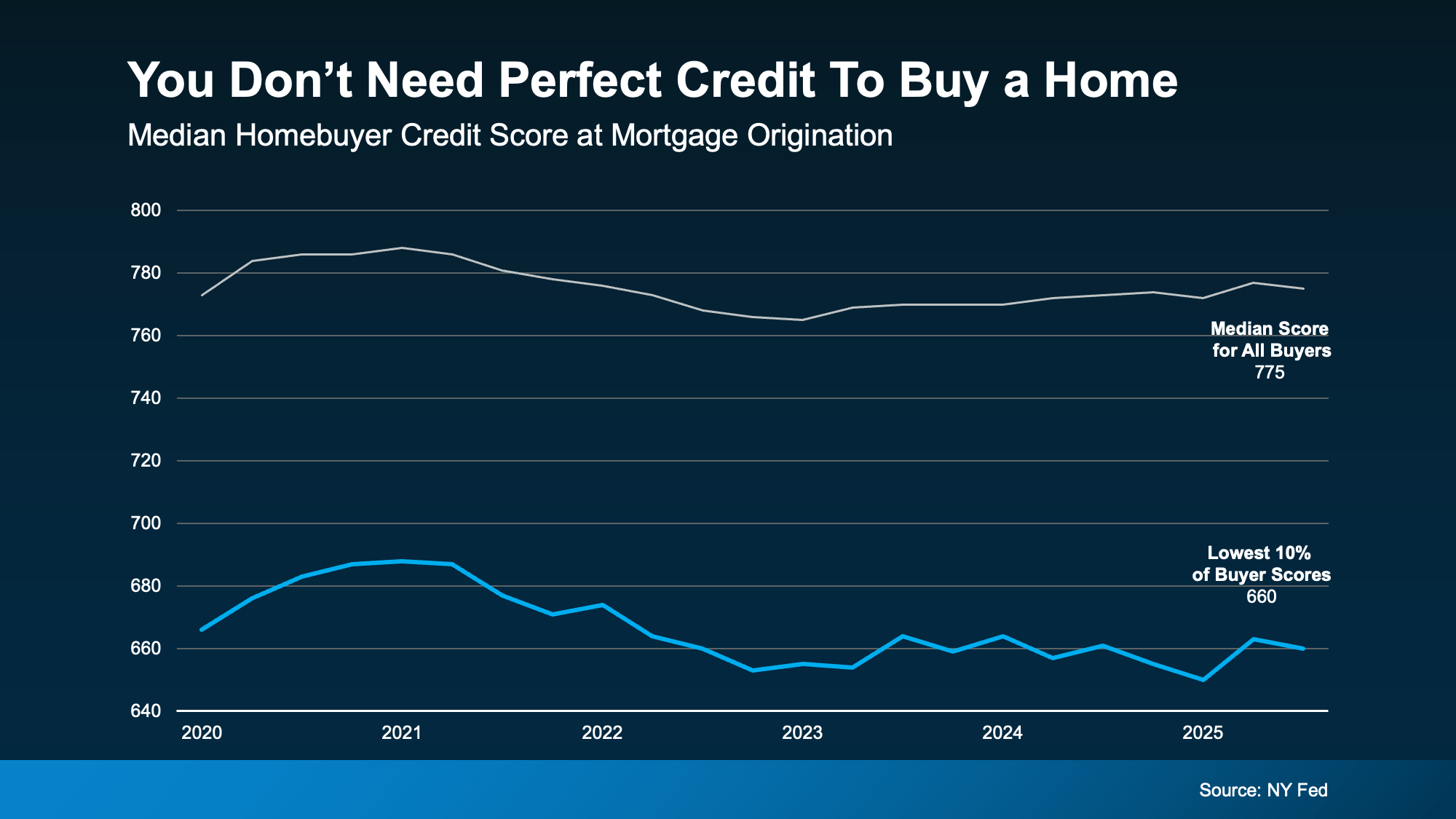

So, where’s this myth come from? Part of the confusion stems from the fact that the typical homebuyer today does have a fairly strong credit score. In fact, according to data from the NY Fed, the median credit score for all buyers is 775.

But that doesn’t mean you need a score that high to qualify.

Looking at recent homebuyers, a number were able to get a mortgage with scores below that threshold. Data shows 10% of scores were around 660. Which means some were higher than that and some were lower, but the median in that lowest 10th percentile was around that range (see graph below):

So, even if your score isn’t as high as you want, that doesn’t automatically close the door. FICO explains there is no universal credit score you absolutely have to have when buying a home:

“While many lenders use credit scores like FICO Scores to help them make lending decisions, each lender has its own strategy, including the level of risk it finds acceptable. There is no single ‘cutoff score’ used by all lenders, and there are many additional factors that lenders may use . . .”

The best thing to do is to talk to a trusted lender to see what’s possible for you. Because a portion of buyers are buying with scores in the 600s – and maybe that means you can too.

Bottom Line

Your credit score is important. But that doesn’t mean it has to be perfect.

If credit has been the reason you’ve been waiting to buy a home, it might be time to take another look at your options. If you want help understanding where you stand and what your next step could be, connect with a local lender.

You don’t need to have everything figured out to start the conversation.

Momentum is quietly building in the housing market. New data from NerdWallet shows more Americans are starting to think about buying a home again. Last year, 15% of respondents said they planned to buy a home in the next 12 months. This year, that number rose to 17%.

That 2% increase might not sound like a big jump, but in a market where buyer demand has been cooling for the past few years, it’s a sign things are starting to shift. More people are feeling ready (or at least closer to ready) to take the leap and buy a home in 2026.

And if you’re in that camp and buying a home is on your goal sheet this year, this is your nudge to connect with a local agent and a trusted lender to start laying the groundwork now.

Planning To Move in Early 2026? Start with These 4 Steps

If you’re eager to get the ball rolling right away, here’s what to tackle first:

Get pre-approved. A pre-approval gives you a real understanding of your buying power and what your payment could be at today’s rates. But keep in mind, Experian says most pre-approvals are only good for 30-90 days, so this step makes the most sense as you’re ready to get serious.

Run the numbers. Look closely at all your expenses to come up with your budget. Consider what you’re spending on other bills and what your monthly mortgage payment would be once you buy. That way you go in with open eyes and you don’t stretch too far.

Define your non-negotiables. Once you know the numbers work, figure out your must-haves. This includes your desired location, commute, layout, school district, lifestyle needs, etc. Getting clear on these now makes decisions easier once you start looking at homes.

Choose your agent early. Look at reviews online and talk to multiple agents to find one you trust that you also click with. The right agent does more than show homes. They help you understand pricing, competition, timing, and strategy before you ever write an offer.

Thinking about Buying Later in the Year? This Is Still Your Window To Prepare

Even if buying feels like a late-2026 goal, this moment still matters. The buyers who feel the most confident later are usually the ones who quietly prepared earlier.

That doesn’t mean big financial commitments or major lifestyle changes. It just means setting yourself up so you’re ready when the timing is right. Here are a few low-stress ways to do that:

Work on your credit. While you don’t need to have perfect credit to buy a home, your score can have an impact on your loan terms and even your mortgage rate. So, working to bring up your score has its perks. Paying down debt now and making payments on time can help bring your score up.

Automate your savings. If you have to remember to transfer money into your homebuying savings manually, you may forget to do it. So, you may want to set up automatic transfers to drive consistency and remove the temptation to spend the money elsewhere.

Lean into your side hustles: Do you have a gig you do (or have done before) to net some extra cash? Taking on part-time work, freelance jobs, or picking up a side hustle can help give your savings a boost.

Put any unexpected cash to good use: If you get any sudden windfalls, like a tax refund, bonus, inheritance, or cash gift from family, put it toward your house fund. You’ll thank yourself later.

The common thread here? The right prep work makes a difference.

Bottom Line

If buying a home in 2026 is on your radar, let’s start the conversation today. Not to rush a decision, but to make sure you know how to get ready for your moment.

Because every move (whether it’s next year or later) is smoother when it starts with a plan. And if you need help coming up with one that works, let’s connect.

Finding the right home feels exciting – but being pre-approved for your loan is what makes it possible. Whether you’re planning to buy soon or still just thinking about it, getting pre-approved is one of the best moves you can make. Here’s why.

1. What Is Pre-Approval, Really?

Pre-approval is much more than a guess. It means a lender has reviewed your finances (things like your income, assets, credit score, debts, and savings) and told you how much they’re willing to let you borrow for your loan.

It’s basically a reality check for your home search, so you can make sure it aligns with your budget and shop confidently when you’re ready to go.

2. Why It’s a Power Move (Especially Right Now)

The housing market’s been shifting lately with mortgage rates moving, prices moderating, and inventory rising. So, knowing what you’re working with in the current market is a big reason why pre-approval matters. Here’s what it gives you:

Clarity: You’ll know what you can afford before you fall in love with a house that’s potentially out of reach.

Confidence: Sellers will take your offer seriously when they see you’re pre-approved because you’re not a risky buyer.

Control: If rates come down and you want to jump on the moment, you’re already a step ahead with your plan.

As Experian explains:

“. . . you’ll want to make sure you receive your preapproval letter before you start looking at homes so you can submit a strong offer as soon as you find what you want. The process can take anywhere from a day to a few weeks, so if you procrastinate, you may lose out to a competing offer.”

And once you find a home you want to put an offer on, pre-approval has another big perk. It not only makes your offer stronger, it shows sellers you’ve already undergone a credit and financial check. As Greg McBride, Chief Financial Analyst at Bankrate, says:

“Preapproval carries more weight because it means lenders have actually done more than a cursory review of your credit and your finances, but have instead reviewed your pay stubs, tax returns and bank statements. A preapproval means you’ve cleared the hurdles necessary to be approved for a mortgage up to a certain dollar amount.”

Translation: Pre-approval helps you make stronger, more informed decisions – and it helps you avoid missing out on a home or getting stuck on the sidelines when the right one hits the market. Because the reality is, competition might be lower these days, but desirable homes (especially the ones that are priced well) still go quickly.

3. Don’t Wait Until You’re “Ready”

Think of it this way: pre-approval doesn’t mean you’re buying a house tomorrow. It just means you’ll be ready when the time comes. And most pre-approvals are good for 60–90 days and can be refreshed easily if your plans change.

So, here’s a good place to start. Ask yourself this question: “If the perfect home came along today, would you be ready to make an offer?”

If your answer is “not quite,” then pre-approval is your next step.

Bottom Line

Pre-approval doesn’t box you in. It opens doors.

In today’s market, buyers who win aren’t the ones who wait. They’re the ones who plan. So, if you’re even thinking about buying in the next few months, get ahead of the game by connecting with your agent and a trusted lender.

They’ll help you understand what how the process works and walk you through every step along the way, so when the right home pops up, you’re ready.

One of the biggest homebuying advantages you can give yourself today is surprisingly simple: a flexible wish list.

Think of it like this. Your wish list and your budget are the guardrails of your search. And when your budget needs to hold firm, there’s another lever you can pull. That’s seeing if you truly need all of your desired features. Because the truth is, a small compromise could be the difference between feeling stuck and getting the keys to your next home.

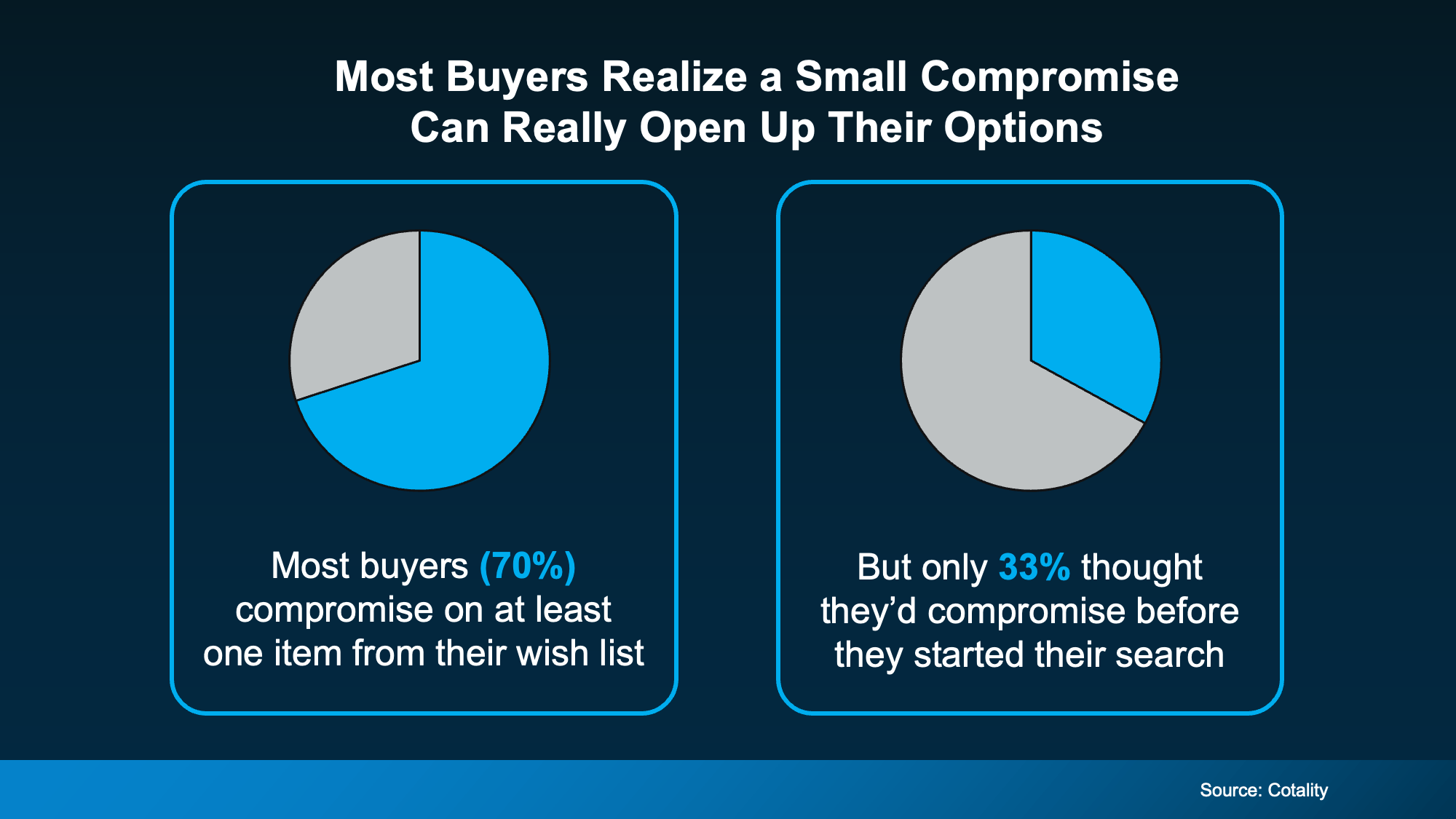

The data shows more buyers are using that strategy to offset affordability hurdles in today’s market. A recent study from Cotality found most buyers (70%)ended up compromising on one or more items from their original wish list. But before they started searching, only 33% expected to compromise at all:

What changed? They realized something during the search. The things you can’t change matter far more than the things you can update later.

You can:

Install hardwood floors

Put in those marble countertops

Upgrade the bathrooms down the line.

You can’t as easily:

Add land

Tack on more bedrooms or bathrooms

Move the house closer to people you care about

In the end, things like the location, layout, and overall bones matter far more than the cosmetic features you can change later. And that realization is power.

A Simple Step That’ll Open More Doors

So, if you’re hitting a wall in your search or you’re browsing online and just not seeing “it,” here’s an easy exercise that can reset the whole experience. Write down everything you want in a home, then sort it into three buckets:

Must-Haves: Your non-negotiables. The things that make daily life workable: the number of bedrooms, the length of your commute, accessibility, safety, or being close to your family or support system.

Nice-to-Haves: Features you’d absolutely enjoy but aren’t truly essential. Some examples: a fenced-in backyard, dual closets in the owner’s suite, or a stamped patio.

Dream Features: The extras that would truly be over the top. They’re the things you think about when you say “one day, I want to have…” It’s great if you get them, but totally fine if you don’t (for now).

Once you divide your list, you’ll notice something. Your wish list can either limit your options or open them up.

Sometimes you’re treating “nice-to-haves” like “must-haves.” Loosen that up even a little, and suddenly more homes come into range – including homes you may have scrolled past that could actually work for your lifestyle.

Small Flexibility, Big Payoff

Your next home doesn’t need to check every box. It just needs to check the right ones.

Maybe that means considering a house that needs light cosmetic updates. Maybe it means choosing a slightly smaller yard for a better location.

These aren’t sacrifices. They’re worthwhile trade-offs that get you into a home. Just remember, anything cosmetic can be upgraded over time. But getting the right bones, the right layout, the right location? That’s what sets you up for the long run.

An Agent Helps You See the Possibilities

If you’re not sure what to hold firm on and where you can flex, that’s where a trusted agent can be a game changer. They’ll help you spot the opportunities, walk you through what features you truly shouldn’t budge on, and determine which ones you can add later – when the time is right.

Bottom Line

If you’re ready to find a home that fits both your budget and your life, let’s take a look at your wish list together. With a local expert on your side, it’s easier to see where a little flexibility can open up a lot more opportunity.

Spring gets all the attention, but it’s not always the best time to sell a house. Yes, more buyers show up, but so do a lot of other sellers.

Winter is different even here in South Florida. With fewer homes on the market, your house has a much better chance of standing out. And that one advantage can make a big difference.

Winter Is When Your Listing Stands Out

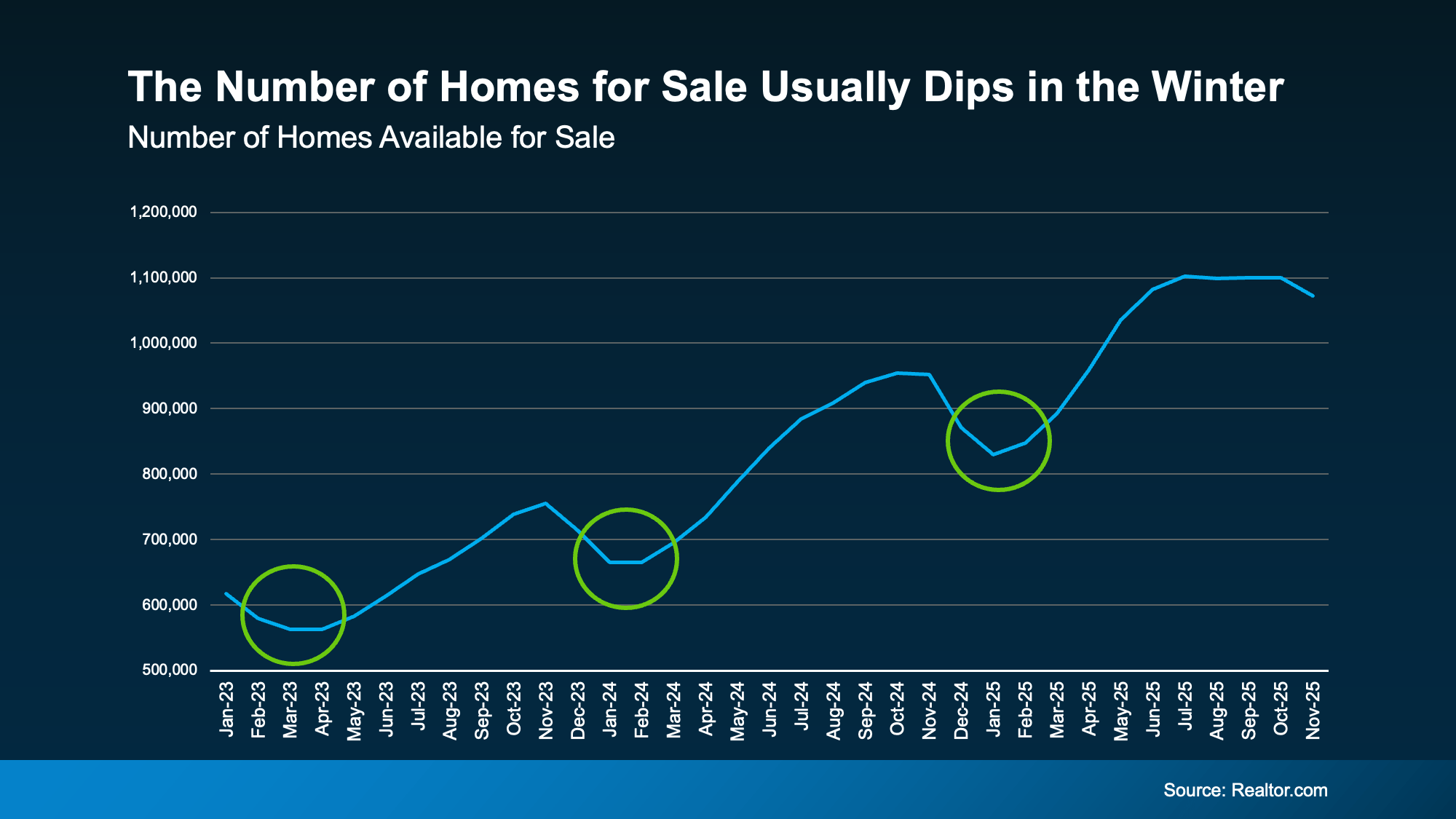

History shows the number of homes for sale tends to drop during the winter months. It’s a trend that’s predictable almost every year.

Data from Realtor.com shows this pattern clearly. Inventory dips in the winter (the green circles in the graph below), then climbs again as soon as spring approaches:

And based on the latest data available, it looks like that pattern may be true again in 2025. The graph shows the supply of homes for sale is starting to come down as we head into the end of the year. And if history is any indicator of where it goes next, it’ll continue to fall just like it usually does.

Here’s why knowing this gives you an edge.

While inventory is higher now than it’s been in the last few years, there are still not as many homes for sale as there’d be in a normal market (2017-2019). And we may even be poised for inventory to dip a bit as the weather cools.

That gives you an opportunity. If you work with an agent to list now, you’ll sell while other homeowners are taking their homes off the market and before the number of homes for sale climbs this spring.

Less competition from other sellers now = more attention on your house this season.

Why wait until everyone else lists in the spring when you can get ahead of the crowd?

Winter Buyers Are Serious Buyers

Another big perk is the buyers looking right now usually need to move.

They’re not just browsing for fun. They’re relocating for work, dealing with a lease ending, making a big life change, or simply ready to move forward sooner rather than later. As U.S. News explains:

“. . . buyers who are trudging through wintry weather often have a good reason for being out in the cold – they need to move. Whether it’s a relocation for a new job, a divorce or the arrival of a new baby, buyers who brave the elements are usually serious and able to make quick decisions.”

That means fewer weekend wanderers and more highly motivated, qualified buyers walking through your door.

And since we know inventory usually drops this time of year, odds are they’ll have a little less to choose from compared to the fall. If you price and prep your house right, maybe your house will be the one that catches their eye.

Bottom Line

Winter might not get the same buzz as spring, but that’s exactly why it works in your favor. Less competition from other sellers, more motivated buyers, and a chance for your house to truly stand out.

If you’re thinking about selling, this season can give you a real advantage. Let’s connect and talk through what listing now could look like for you.

New home construction today is giving buyers something it feels like they haven’t gotten much lately: a real shot at both the home they want and the deal they need. More brand-new options are on the market right now, and builders are rolling out incentives that make these homes more affordable than many people expect.

It’s a combination that doesn’t come around often – and it’s putting buyers in a surprisingly strong position this season. Here’s why this moment matters and why it’s worth partnering with your own local agent to take advantage of it.

1. More New Homes Are Available Now – and That May Not Last

There’s more new construction on the market today than normal. And for buyers, that means:

More cutting-edge communities

More move-in-ready homes

More floor plans to pick from

More upgraded designs and modern features

But that variety may not last.

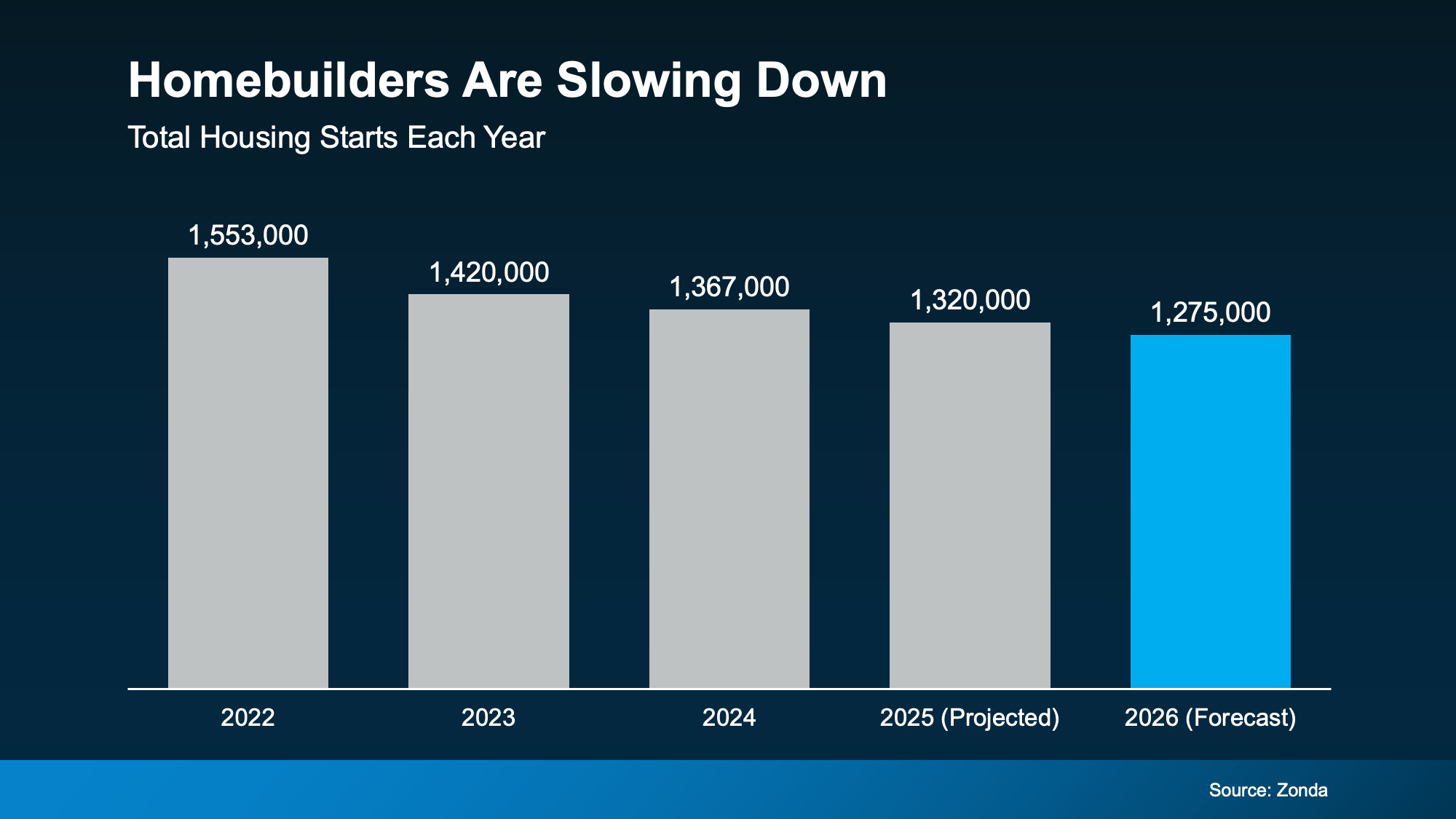

Data from Zonda shows that even though it feels like new homes are popping up just about everywhere, builders have actually started pulling back. The number of starts (that’s when builders break ground) has been slowly but steadily declining over the past few years. And that’s good because it prevents overbuilding nationally.

But here’s the real insight that can give you an edge. Forecasts show that slight downward trend should continue next year (see graph below):

It’s a signal that the new inventory we have now may be your widest pool of all-new options for a while.

Today, Redfin says roughly 1 in 3 homes (27%) on the market are new builds. That’s higher than the norm, but the lowest share in four years. And it makes sense based on the graph above.

That means if you want more options to choose from, now’s the time to look.

And if you’re wondering: why the pullback? It’s simple. Since there are already more new homes for sale than usual, builders want to focus on selling down the supply they already have on the market rather than adding more new homes. And that leads to point two.

2. Builder Incentives Just Hit an All-Time High

Here’s where things get even better for buyers. To make sure the inventory they have now keeps moving, builders are offering incentives at levels not seen in years – and many of those perks directly help buyers with affordability. Buyers today are getting:

Lower Prices: Builders are dropping the prices on their brand-new homes to draw in buyers.

Help with Closing Costs: Some builders are covering thousands of dollars in fees to reduce the upfront cost of buying.

Extra Upgrades: Think premium finishes, appliance packages, and designer features, all added at no extra cost.

Mortgage Rate Buydowns: This is when the builder pays to get you a lower mortgage rate, which reduces your monthly payments and helps with affordability.

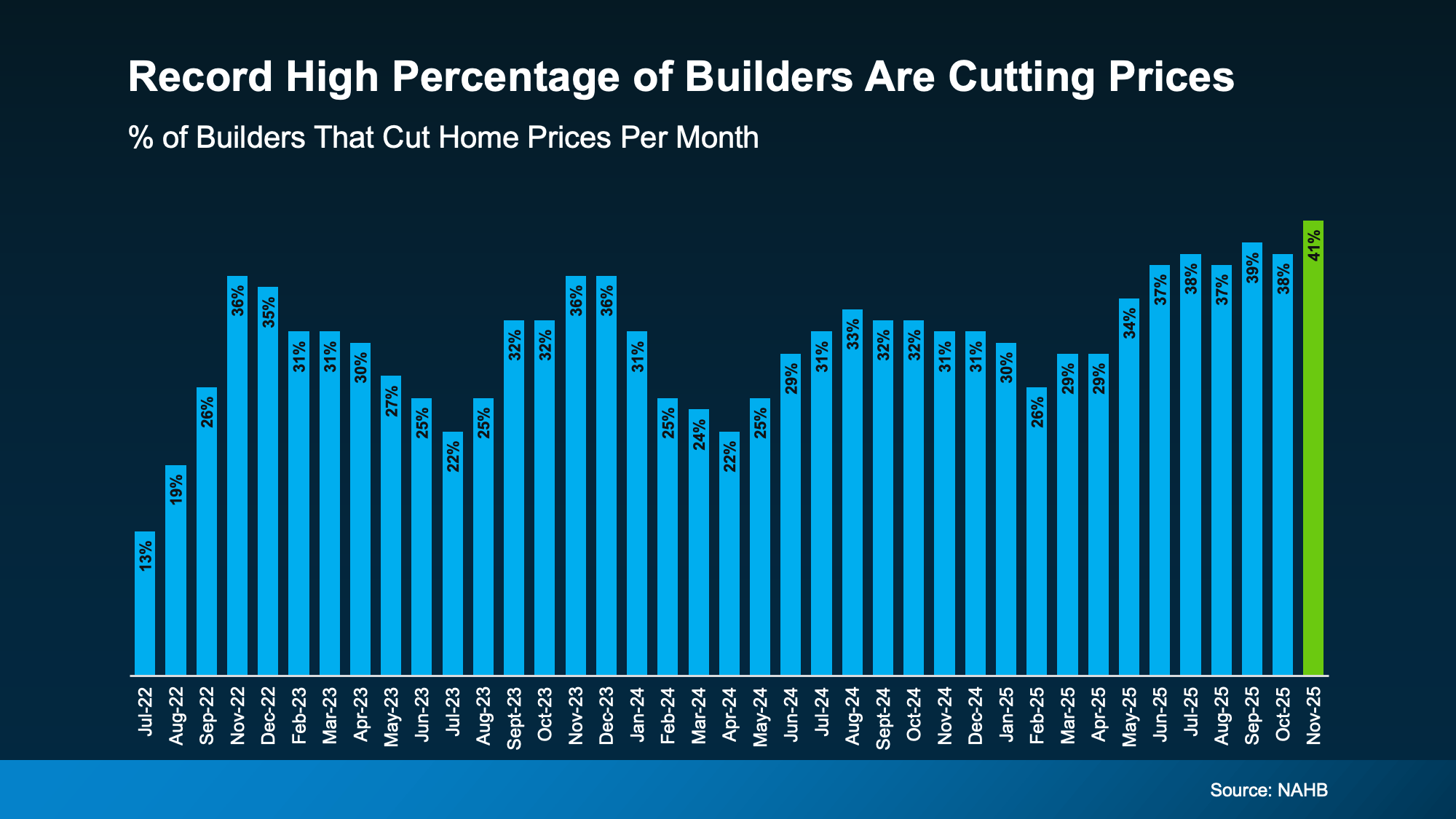

But you don’t have to be lucky to see these types of perks. The truth is, the vast majority of builders are offering advantages like these right now. According to the National Association of Homebuilders (NAHB) 65% of builders say they’re using some type of sales incentive and:

“. . . 41% of builders reported cutting prices in November, a record high in the post-Covid period and the first time this measure has passed 40%.”

That’s a big deal. It shows how willing builders are to negotiate right now.

And if you look closely at the graph, you’ll notice the use of incentives typically falls in the early part of the year, as buyer demand rises going into the spring. So, you have an edge if you act now. This may be your ideal window to find the most options and better prices.

If you lean on your own agent and you’re savvy about what you ask for, you could walk away with some of the best perks buyers have seen in years. And when every dollar counts and any incentive helps your bottom line, that’s worth looking into.

More options and more savings = an offer too good to pass up.

Bottom Line

With most builders offering generous incentives and a wider selection of new homes for sale, buyers may be looking at one of the best times in years to buy a new build.

Let’s connect if you want to know which communities, builders, and incentives offer the most value today. Having your own agent (not the builder’s representative) makes the sale and negotiation process that much easier for you.

If you could have a brand-new home for less than you may expect, would you be interested?

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link