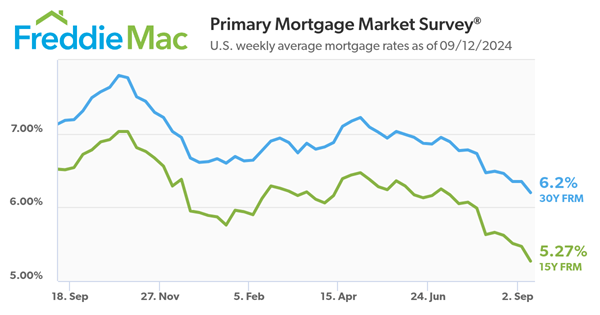

Freddie Mac (OTCQB: FMCC) today released the results of its Primary Mortgage Market Survey® (PMMS®), showing the 30-year fixed-rate mortgage (FRM) averaged 6.20 percent.

“Mortgage rates have fallen more than half a percent over the last six weeks and are at their lowest level since February 2023,” said Sam Khater, Freddie Mac’s Chief Economist. “Rates continue to soften due to incoming economic data that is more sedate. But despite the improving mortgage rate environment, prospective buyers remain on the sidelines, as they negotiate a combination of high house prices and persistent supply shortages.”

The 30-year FRM averaged 6.20 percent as of September 12, 2024, down from last week when it averaged 6.35 percent. A year ago at this time, the 30-year FRM averaged 7.18 percent.

The 15-year FRM averaged 5.27 percent, down from last week when it averaged 5.47 percent. A year ago at this time, the 15-year FRM averaged 6.51 percent.

The PMMS® is focused on conventional, conforming, fully amortizing home purchase loans for borrowers who put 20 percent down and have excellent credit.

Now that you’ve decided to buy a home and are ready to make it happen, it’s a good idea to plan ahead for the costs that are a typical part of the homebuying process. And while your down payment is probably the number one expense on your mind, don’t forget about closing costs. Here’s what you need to know.

What Are Closing Costs?

Simply put, your closing costs are the additional fees and payments you have to make at closing. And while they’ll vary based on the price of the home and how it’s being financed, every buyer has these, so they shouldn’t be a surprise. It’s just that some people forget to budget for them. According to Freddie Mac, this part of the homebuying process typically includes:

Application fees

Credit report fees

Loan origination fees

Appraisal fees

Home inspection fees

Title insurance

Homeowners insurance

Survey fees

Attorney fees

Some of these are one-time expenses that are baked into your closing costs. Others, like homeowners’ insurance, are initial installment payments for ongoing responsibilities you’ll have once you take possession of the home.

“Closing costs vary greatly depending on your location and the price of your home. Typically, you should be prepared to pay between 2% and 5% of the home purchase price in closing fees.”

With that in mind, here’s how you can get an idea of what you’ll need to budget. Let’s say you find a home you want to purchase at today’s median price of $422,600. Based on the 2-5% Freddie Mac estimate, your closing fees could be between roughly $8,452 and $21,130.

But keep in mind, if you’re in the market for a home above or below this price range, your numbers will be higher or lower.

Tips To Reduce Your Closing Costs

If you’re wondering if there’s any way to inch that down a little bit, NerdWallet lists a few things that could help:

Negotiate with the Seller: Some sellers are willing to cover part or all of these expenses — especially since homes are staying on the market a bit longer now. Sellers may be more motivated to compromise, and you’ll find you have a bit more negotiation power. So don’t hesitate to ask them for concessions like paying for the home inspection or giving you a credit toward closing costs.

Shop Around for Home Insurance: Since rising home insurance is a challenge in many areas of the country right now, take the time to get a clear picture of all your options. Each insurance company offers their own policies and coverage, so get multiple quotes and see how they compare. Choosing a policy that provides reliable coverage at a competitive rate can make a difference.

Look into Closing Cost Assistance: Just like there are programs out there to help with your down payment, options exist to get support with closing costs too. While they’ll vary by area, there are programs for various income levels, certain professions, and specific towns or neighborhoods too. If you want to learn more, Experian says:

“Your real estate professional should be able to steer you toward applicable programs, and the U.S. Department of Housing and Urban Development (HUD) maintains a helpful resource for finding homebuying assistance programs in every state.”

Bottom Line

Planning for the fees and payments you’ll need to cover when you’re closing on your home is important – and it doesn’t have to be a big surprise. With the right experts on your side, you can make sure you’re prepared. Let’s connect so you have someone you can go to for more tips and advice.

Why Pre-Approval Should Be at the Top of Your Homebuying To-Do List

Since the supply of homes for sale is growing and mortgage rates are coming down, you may be thinking it’s finally your moment to jump into the market. To make sure you’re ready, you need to get pre-approved for a mortgage.

That’s when a lender looks at your finances, including things like your W-2, tax returns, credit score, and bank statements, to figure out what they’re willing to loan you. After that process, you’ll get a pre-approval letter to show what you can borrow. Here are two reasons why this is essential in today’s market.

Pre-Approval Helps You Know Your Numbers

While home affordability is finally starting to show signs of improving, it’s still tight. So, it’s a good idea to talk to a lender about your loan options and how today’s changing mortgage rates will impact your monthly payment. The pre-approval process is the perfect time for that. In addition to determining the maximum amount you can borrow, pre-approval also helps you understand this piece of the puzzle. As Investopedia says:

“Consulting with a lender and obtaining a pre-approval letter allows you to discuss loan options and budgeting with the lender; this step can clarify your total house-hunting budget and the monthly mortgage payment you can afford.”

You should use this information to tailor your home search to what you’re actually comfortable with budget-wise. Since mortgage rates have inched down some lately, you may find you’re able to afford a bit more than you’d expect for your monthly payment, but you still want to avoid overextending. As CNET explains:

“In many cases, a lender may preapprove you for more than you need to spend on a home. And while it can be tempting to look at houses outside your budget, it won’t help you in the long run. Before you start touring homes, figure out how much you can realistically afford and stick to your budget.”

Pre-Approval Makes Your Offer More Appealing

And once you do find a home you want in your budget, pre-approval has another big perk. It not only makes your offer stronger, it also shows sellers you’ve already undergone a credit and financial check. When a seller sees you as a serious buyer, they may be more attracted to your offer because it seems more likely to go through. As Greg McBride, Chief Financial Analyst at Bankrate, says:

“Preapproval carries more weight because it means lenders have actually done more than a cursory review of your credit and your finances, but have instead reviewed your pay stubs, tax returns and bank statements. A preapproval means you’ve cleared the hurdles necessary to be approved for a mortgage up to a certain dollar amount.”

As mortgage rates trend down, more buyers are going to be ready to jump back into the market. And while demand is still limited right now, there’s the potential for competition to pick back up, especially in hot markets. So, why not stack the deck in your favor and make sure you’re putting yourself in the best position possible when you find a home you love?

Bottom Line

If you’re planning on buying a home, don’t forget to get pre-approved early in the process. It can help you get a more in-depth understanding of what you can borrow and shows sellers you mean business.

There are a number of reasons you may be thinking about selling your house. And as you weigh your options, you may find you’re unsure how you’re going to deal with one thing about today’s housing market – and that’s affordability. If that’s your biggest concern, understanding how much equity you have in your house could help make your decision that much easier. Here are two key factors that have a big impact on your equity.

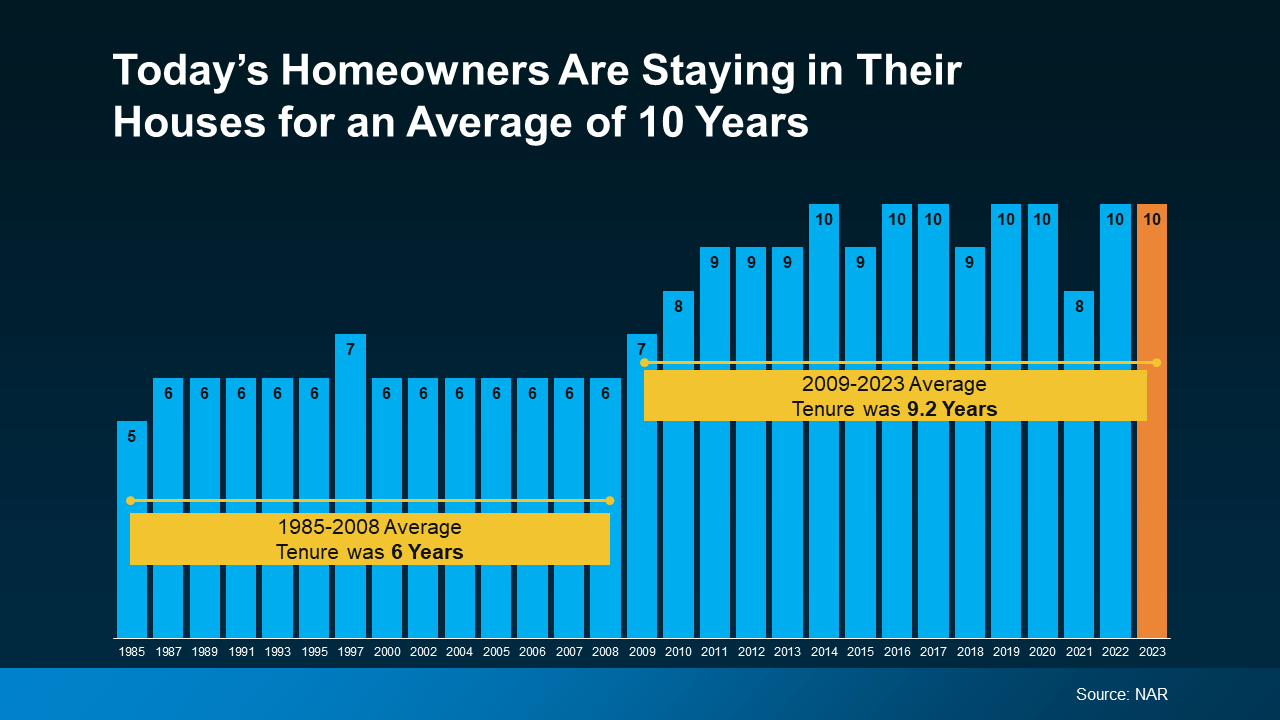

How Long You’ve Been in Your Home

First up is homeowner tenure. That’s how long homeowners live in a house, on average, before selling or choosing to move. From 1985 to 2009, the average length of time homeowners stayed put was roughly six years.

But according to the National Association of Realtors (NAR), that number has been climbing. Now, the average tenure is 10 years (see graph below):

Here’s why that’s such a big deal. You gain equity as you pay down your home loan and as home prices climb. And when you combine all of your mortgage payments with how much prices have gone up over the span of 10 years, that adds up. So, if you’ve lived in your house for a while now, you may be sitting on a pile of equity.

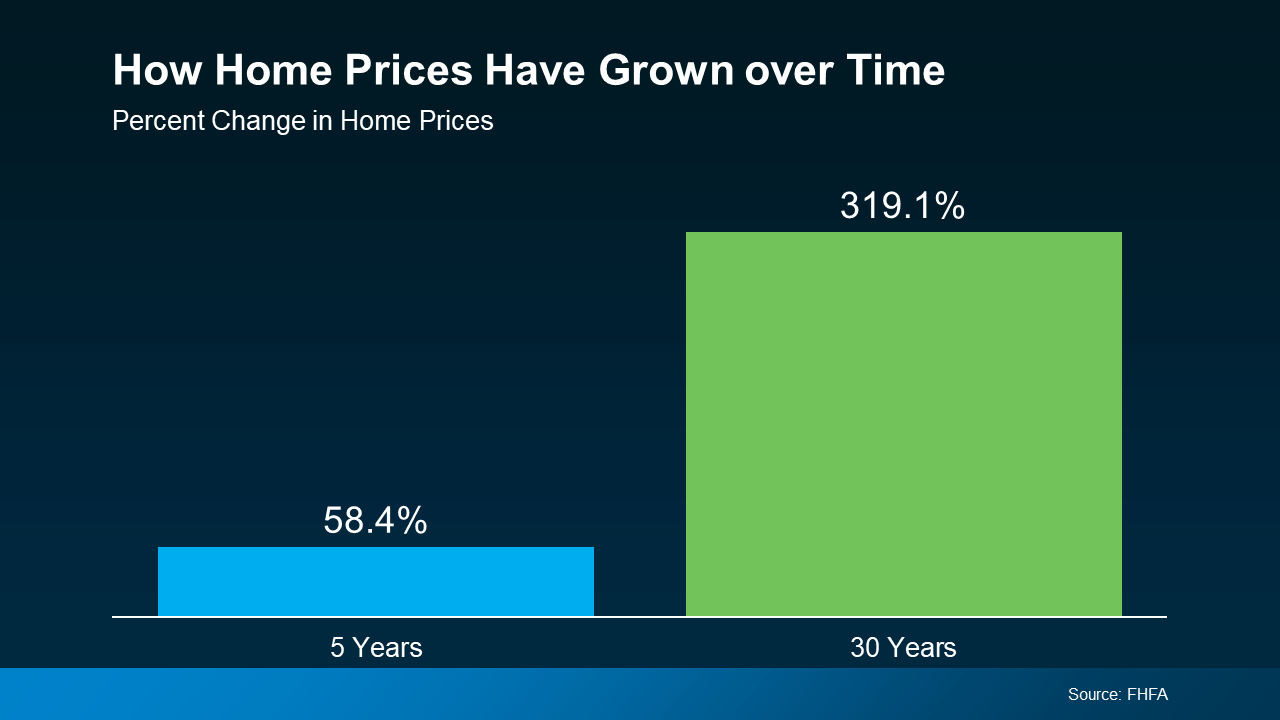

How Home Prices Appreciate over Time

To help show how much the price appreciation piece adds up, take a look at this data from the Federal Housing Finance Agency (FHFA) (see graph below):

Here’s what this means for you. While home prices vary by area, the typical homeowner who’s been in their house for five years saw it increase in value by nearly 60%. And the average homeowner who’s owned their home for 30 years saw it more than triple in value in that time.

Whether you’re looking to downsize, relocate to a dream destination, or move so you can live closer to friends or loved ones, your equity can be a game changer.

Bottom Line

If you want to find out how much equity you’ve built up over the years and how you can use it to buy your next home, let’s connect.

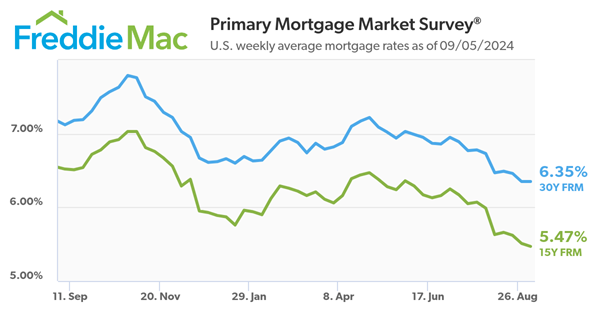

Freddie Mac (OTCQB: FMCC) today released the results of its Primary Mortgage Market Survey® (PMMS®), showing the 30-year fixed-rate mortgage (FRM) averaged 6.35 percent.

“Mortgage rates remained flat this week as markets await the release of the highly anticipated August jobs report,” said Sam Khater, Freddie Mac’s Chief Economist. “Even though rates have come down over the summer, home sales have been lackluster. On the refinance side however, homeowners who bought in recent years are taking advantage of declining mortgage rates in order to lower their monthly payments.”

The 30-year FRM averaged 6.35 percent as of September 5, 2024, unchanged from last week. A year ago at this time, the 30-year FRM averaged 7.12 percent.

The 15-year FRM averaged 5.47 percent, down from last week when it averaged 5.51 percent. A year ago at this time, the 15-year FRM averaged 6.52 percent.

The PMMS® is focused on conventional, conforming, fully amortizing home purchase loans for borrowers who put 20 percent down and have excellent credit.

Here’s reaction from National Association of Realtors Deputy Chief Economist and VP of Research, Jessica Lutz

Facts: The average 30-year fixed mortgage rate from Freddie Mac remained unchanged at 6.35% this week from last week. At 6.35%, with 20% down, a monthly mortgage payment on a home with a price of $400,000 is $1,991. With 10% down, the typical payment would be $2,240.

Positive: Although mortgage rates did not move, there was a slight increase in mortgage applications for purchase from the Mortgage Bankers Association. Some buyers are taking advantage of lower rates and more housing inventory.

Negative: While mortgage rates are significantly lower than in recent months, anticipation of a Fed rate cut in two weeks may have buyers reticent to jump in so they can wait for even lower rates. However, as nearly everyone has forecasted a Fed Funds rate cut, it is unlikely to lower mortgage interest rates significantly.

Now that it’s September, all eyes are on the Federal Reserve (the Fed). The overwhelming expectation is that they’ll cut the Federal Funds Rate at their upcoming meeting, driven primarily by recent signs that inflation is cooling, and the job market is slowing down. Mark Zandi, Chief Economist at Moody’s Analytics, said:

“They’re ready to cut, just as long as we don’t get an inflation surprise between now and September, which we won’t.”

But what does this mean for the housing market, and more importantly, for you as a potential homebuyer or seller?

Why a Federal Funds Rate Cut Matters

The Federal Funds Rate is one of the key factors that influences mortgage rates – things like the economy, geopolitical uncertainty, and more also have an impact.

When the Fed cuts the Federal Funds Rate, it signals what’s happening in the broader economy, and mortgage rates tend to respond. While a single rate cut might not lead to a dramatic drop in mortgage rates, it could contribute to the gradual decline that’s already happening.

As Mike Fratantoni, Chief Economist at the Mortgage Bankers Association (MBA), points out:

“Once the Fed kicks off a rate-cutting cycle, we do expect that mortgage rates will move somewhat lower.”

And any upcoming Federal Funds Rate cut likely won’t be a one-time event. Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), says:

“Generally, the rate-cutting cycle is not one-and-done. Six to eight rounds of rate cuts all through 2025 look likely.”

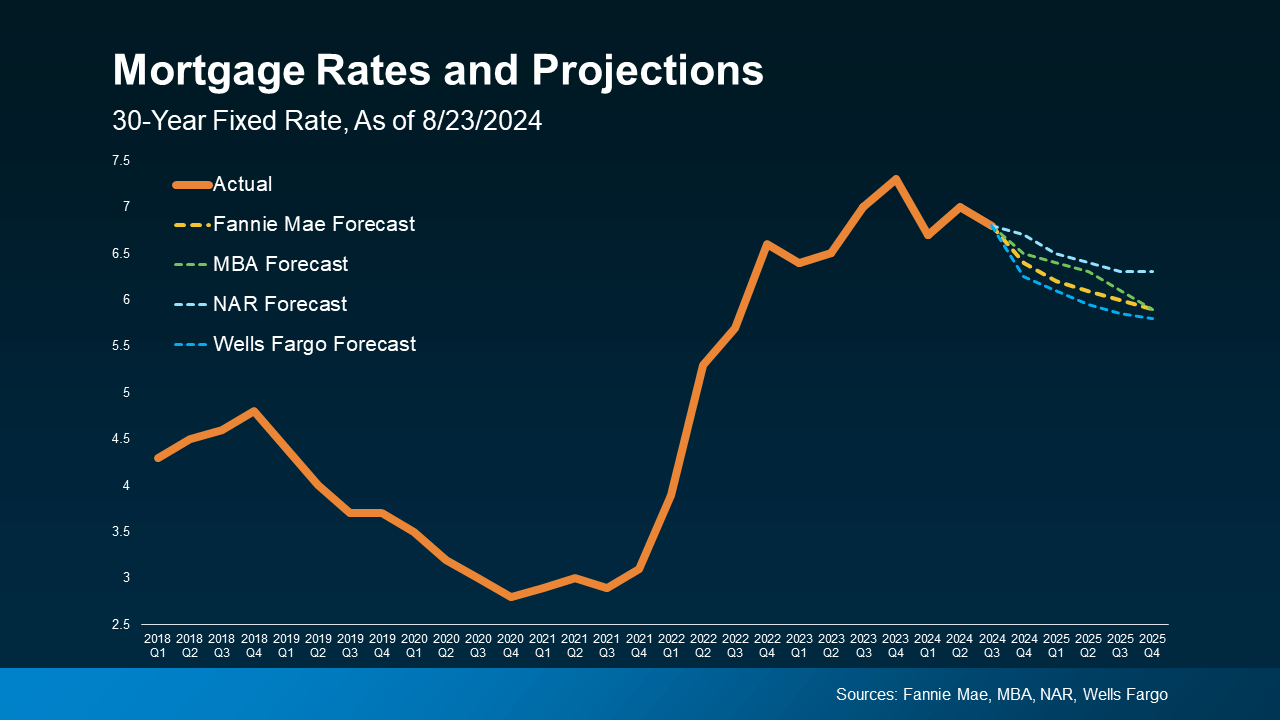

The Projected Impact on Mortgage Rates

Here’s what experts in the industry project for mortgage rates through 2025. One contributing factor to this ongoing gradual decline is the anticipated cuts from the Fed. The graph below shows the latest forecasts from Fannie Mae, MBA, NAR, and Wells Fargo (see graph below):

So, with recent improvements in inflation and signs of a cooling job market, a Federal Funds Rate cut is likely to lead to a moderate decline in mortgage rates (shown in the dotted lines). Here are two big reasons why that’s good news for both buyers and sellers:

1. It Helps Alleviate the Lock-In Effect

For current homeowners, lower mortgage rates could help ease the lock-in effect. That’s where people feel stuck within their current home because today’s rates are higher than what they locked in when they bought their current house.

If the fear of losing your low-rate mortgage and facing higher costs has kept you out of the market, a slight reduction in rates could make selling a bit more attractive again. However, this isn’t expected to bring a flood of sellers to the market, as many homeowners may still be cautious about giving up their existing mortgage rate.

2. It Should Boost Buyer Activity

For potential homebuyers, any drop in mortgage rates will provide a more inviting housing market. Lower mortgage rates can reduce the overall cost of homeownership, making it more feasible for you if you’ve been waiting to make a move.

What Should You Do?

While a Federal Funds Rate cut is not expected to lead to drastically lower mortgage rates, it will likely contribute to the gradual decrease that’s already happening.

And while the anticipated rate cut represents a positive shift for the future of the housing market, it’s important to consider your options right now. Jacob Channel, Senior Economist at LendingTree, sums it up well:

“Timing the market is basically impossible. If you’re always waiting for perfect market conditions, you’re going to be waiting forever. Buy now only if it’s a good idea for you.”

Bottom Line

The expected Federal Funds Rate cut, driven by improving inflation and slower job growth, is likely to have a positive, though gradual, impact on mortgage rates. That could help unlock opportunities for you. When you’re ready, let’s connect. That way you’ll be prepared to take action when the time is right for you.

Should You Sell Now? The Lifestyle Factors That Could Tip the Scale

Are you on the fence about whether to sell your house now or hold off? It’s a common dilemma, but here’s a key point to consider: your lifestyle might be the biggest factor in your decision. While financial aspects are important, sometimes the personal motivations for moving are reason enough to make the leap sooner rather than later.

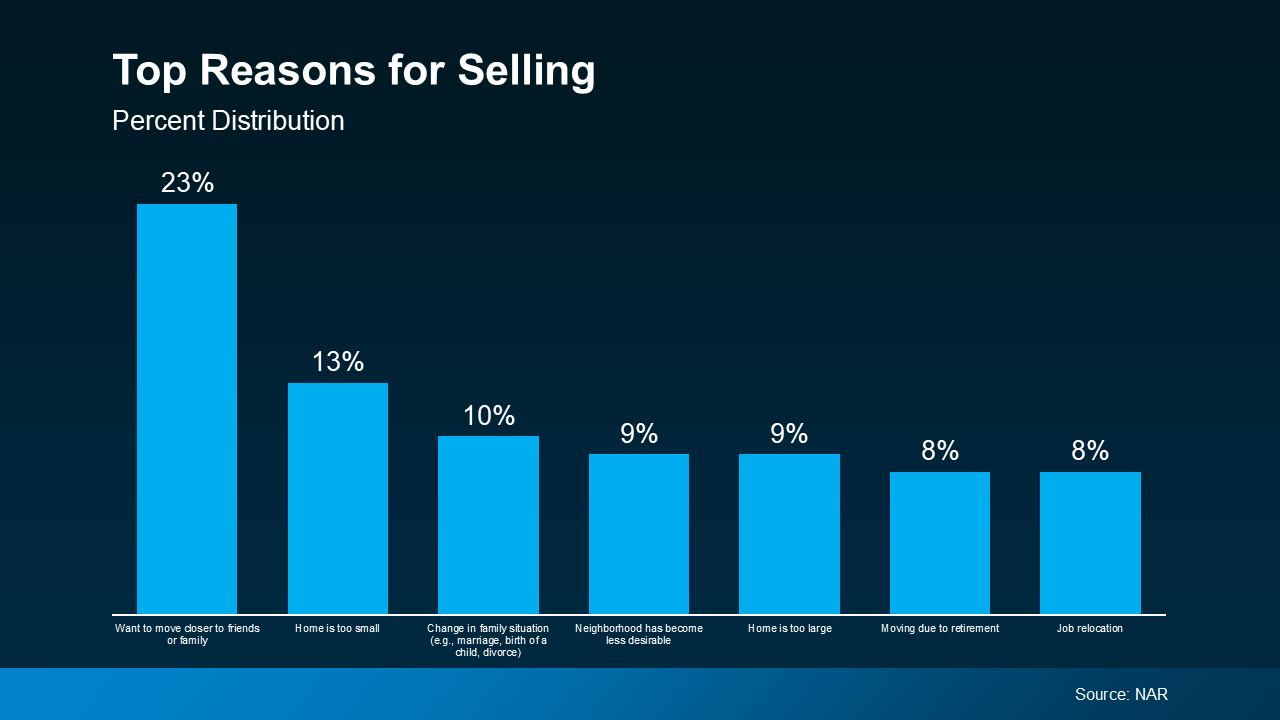

An annual report from the National Association of Realtors (NAR) offers insight into why homeowners like you chose to sell. All of the top reasons are related to life changes. As the graph below highlights:

As the visual shows, the biggest motivators were the desire to be closer to friends or family, outgrowing their current house, or experiencing a significant life change like getting married or having a baby. The need to downsize or relocate for work also made the list.

If you, like the homeowners in this report, find yourself needing features, space, or amenities your current home just can’t provide, it may be time to consider talking to a real estate agent about selling your house. Your needs matter. That agent will walk you through your options and what you can expect from today’s market, so you can make a confident decision based on what matters most to you and your loved ones.

Your agent will also be able to help you understand how much equity you have and how it can make moving to meet your changing needs that much easier. As Danielle Hale, Chief Economist at Realtor.com, explains:

“A consideration today’s homeowners should review is what their home equity picture looks like. With the typical home listing price up 40% from just five years ago, many home sellers are sitting on a healthy equity cushion. This means they are likely to walk away from a home sale with proceeds that they can use to offset the amount of borrowing needed for their next home purchase.”

Bottom Line

Your lifestyle needs may be enough to motivate you to make a change. If you want help weighing the pros and cons of selling your house, let’s have a conversation.

If you’re thinking about downsizing, you may be hearing about 55+ communities and wondering if they’d be a good fit for you. Here’s some information that could help you make your decision.

What Is a 55+ Community?

It’s important to note that these communities aren’t just for people who need extra support – they can be pretty vibrant, too. Many people who are downsizing opt for this type of home because they’re looking to be surrounded by people in a similar season of life. U.S. Newsexplains:

“The terms ‘55-plus community,’ ‘active adult community,’ ‘lifestyle communities’ and ‘planned communities’ refer to a setting that caters to the needs and preferences of adults over the age of 55. These communities are designed for seniors who are able to care for themselves but may be looking to downsize to a community with others their same age and with similar interests.”

Why It’s Worth Considering This Type of Home

If that sounds like something that may interest you, here’s one thing to consider. You may find you’ve got a growing list of options if you look at this type of community. According to 55places.com, the number of listings tailored for homebuyers in this age group has increased by over 50% compared to last year.

And a bigger pool of options could make your move much less stressful because it’s easier to find something that’s specifically designed to meet your needs.

Other Benefits of 55+ Communities

On top of that, there are other benefits to seeking out this type of home. An article from 55places.com, highlights just a few:

Lower-Maintenance Living: Tired of mowing the lawn or pulling weeds? Many of these communities take care of this for you. So, you can spend more time doing fun things, and less time on maintenance.

On-Site Amenities: Some feature lifestyle amenities like a clubhouse, fitness center, and more, so it’s easy to stay active. Plus, others offer media rooms, libraries, spas, arts and craft studios, and more.

Like-Minded Neighbors: Additionally, these types of homes usually offer clubs, outings, meet-ups, and more to foster a close-knit community.

Accessible Floor Plans: Not to mention, many have first-floor living options, ample storage spaces, and modern floor plans so you can have a home tailored to this phase in your life.

Bottom Line

If this sounds appealing to you, let’s talk about what’s available in our area, and the unique amenities for each community. You may find a 55+ home is exactly what you’ve been searching for.

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link