Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

What a Fed Rate Cut Could Mean for Mortgage Rates

The Federal Reserve (the Fed) meets this week, and expectations are high that they’ll cut the Federal Funds Rate. But does that mean mortgage rates will drop? Let’s clear up the confusion.

The Fed Doesn’t Directly Set Mortgage Rates

Right now, all eyes are on the Fed. Most economists expect they’ll cut the Federal Funds Rate at their mid-September meeting to try to head off a potential recession.

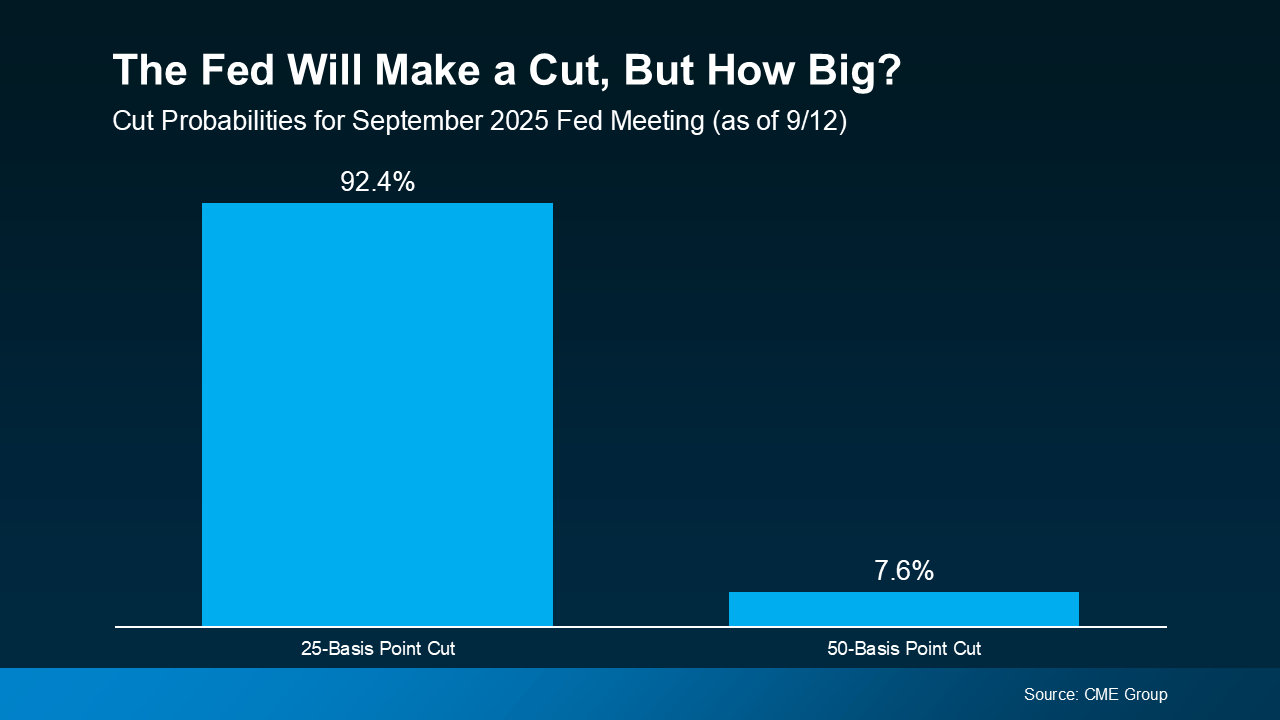

According to the CME FedWatch Tool, markets are already betting on it. There’s virtually a 100% chance of a September cut. And based on what we know now, there’s about a 92% chance it’ll be a small cut (25 basis points) and an 8% chance it will be a bigger cut (50 basis points):

So, what exactly is the Federal Funds Rate? It’s the short-term interest rate banks charge each other. It impacts borrowing costs across the economy, but it’s not the same thing as mortgage rates. Still, the Fed’s actions can shape the direction mortgage rates take next.

So, what exactly is the Federal Funds Rate? It’s the short-term interest rate banks charge each other. It impacts borrowing costs across the economy, but it’s not the same thing as mortgage rates. Still, the Fed’s actions can shape the direction mortgage rates take next.

Why Markets Already Saw This Cut Coming

Here’s the part that may surprise you. Mortgage rates tend to respond to what the financial markets think the Fed will do, before the Fed officially acts. Basically, when markets anticipate a Fed cut, that outlook gets priced into mortgage rates ahead of time.

That’s exactly what happened after weaker-than-expected jobs reports on August 1 and September 5. Each time, mortgage rates ticked down as financial markets grew more confident a cut was coming soon. And even though inflation rose slightly in the latest CPI report, the Fed is still expected to make a cut.

So, if the Fed goes with a 25-basis point cut, as expected, that’s likely already baked in to current mortgage rates, and we may not see a dramatic drop.

But if they go bigger and drop their Federal Funds Rate by 50 basis points instead, mortgage rates could come down more than they already have.

So, Where Do Mortgage Rates Go from Here?

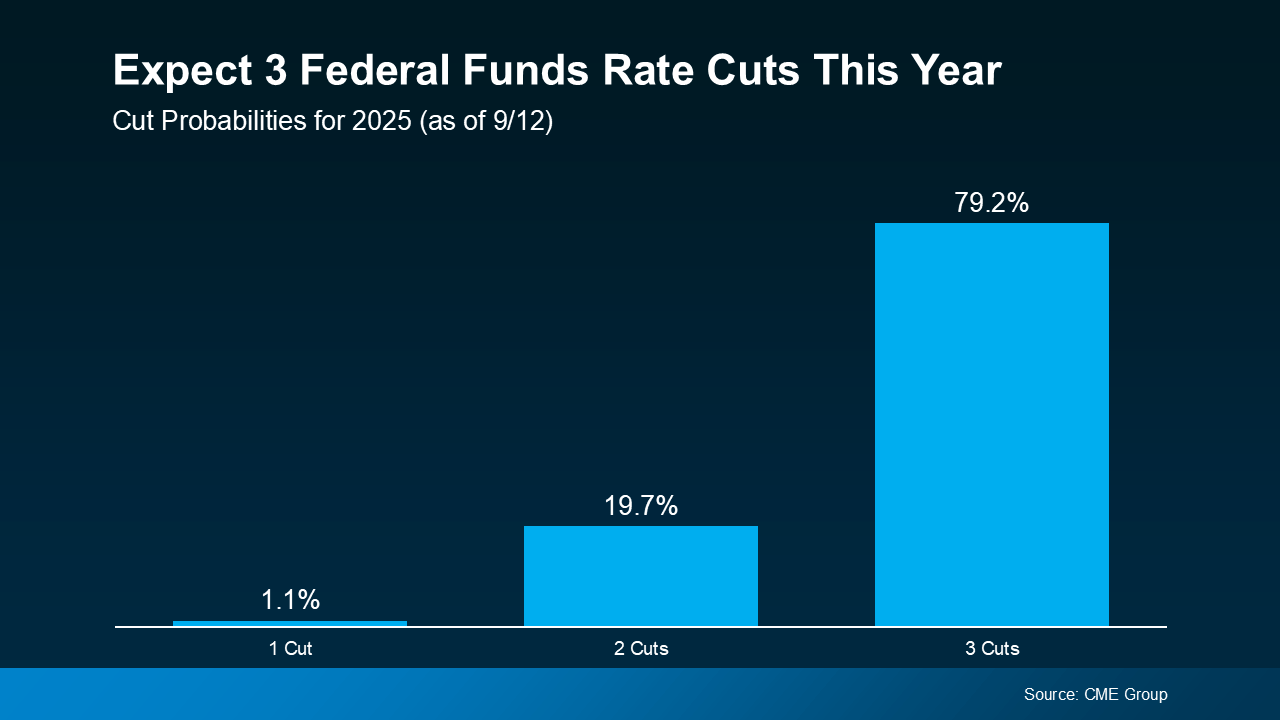

While the upcoming cut may not move the needle much, many experts expect the Fed could cut the Federal Funds Rate more than once before the end of the year. Of course, that’s if the economy continues to cool (see graph below):

As Sam Williamson, Senior Economist at First American, explains:

As Sam Williamson, Senior Economist at First American, explains:

“For mortgage rates, investor confidence in a forthcoming rate-cutting cycle could help push borrowing costs lower in the back half of 2025, offering some relief to housing affordability and potentially helping to boost buyer demand and overall market activity.”

If multiple rate cuts happen, or even if markets just believe they will, mortgage rates could ease further in the months ahead. But here’s the catch – all of this depends on how the economy evolves. Surprise inflation data or unexpected shifts could quickly change the outlook.

Bottom Line

Mortgage rates likely won’t drop sharply overnight, and they won’t mirror the Fed’s moves one-for-one. But if the Fed begins a rate-cutting cycle, and markets continue to expect it, mortgage rates could trend lower later this year and into 2026.

If you’ve been waiting and watching the housing market, now’s the time to talk strategy. Even small changes in rates can make a meaningful difference in affordability, and understanding what’s ahead helps you make the best decision for your situation.

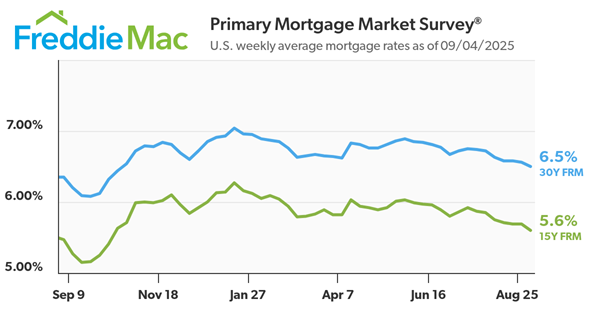

Mortgage Rates Drop

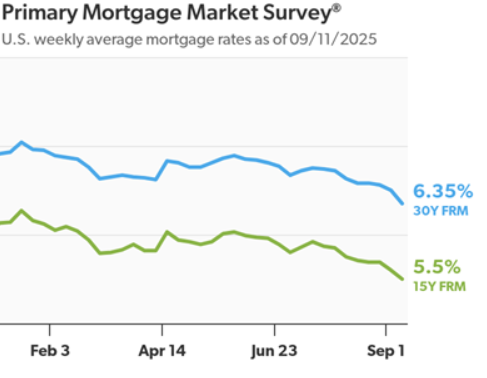

Freddie Mac today released the results of its Primary Mortgage Market Survey® (PMMS®), showing the 30-year fixed-rate mortgage (FRM) averaged 6.35%.

“The 30-year fixed-rate mortgage fell 15 basis points from last week, the largest weekly drop in the past year,” said Sam Khater, Freddie Mac’s Chief Economist. “Mortgage rates are headed in the right direction and homebuyers have noticed, as purchase applications reached the highest year-over-year growth rate in more than four years.”

- The 30-year FRM averaged 6.35% as of September 11, 2025, down from last week when it averaged 6.50%. A year ago at this time, the 30-year FRM averaged 6.20%.

- The 15-year FRM averaged 5.50%, down from la.35%st week when it averaged 5.60%. A year ago at this time, the 15-year FRM averaged 5.27%.

The PMMS® is focused on conventional, conforming, fully amortizing home purchase loans for borrowers who put 20% down and have excellent credit.

Patience Won’t Sell Your House. Pricing Will!

They say it only takes one. That one buyer who walks through the door and says this is it. So, are you waiting for the perfect buyer to fall in love with your house? In today’s market, that’s usually not what’s holding things up. And here’s why.

Let’s be real. Homes are taking a week longer to sell than they did a year ago. According to Realtor.com:

“Homes are also taking longer to sell. The typical home spent 60 days on the market in August, seven days longer than last year and now above pre-pandemic norms for the second consecutive month. This was the 17th straight month of year-over-year increases in time on market.”

Part of that is because there are more homes on the market. So, with more options for buyers to choose from, they aren’t getting snatched up quite as fast. But there’s another big reason: price.

The Average List Price Isn’t Going Up – and That Matters

Today, a lot of homeowners are overshooting their list price. They remember the big climb in home prices a few years ago, and they don’t realize how much has changed.

One of the most important, but often overlooked, changes in today’s housing market is this: average list prices have held steady for the past few years.

That’s a big shift from a typical market, where prices were rising steadily each year. And it’s significantly different than the 2021-2022 surge when sellers could set their price just about anywhere and still attract multiple offers over asking.

But now? That trend has leveled off – and sellers who want to stay competitive need to take note (see graph below):

Here’s what this says about today’s market. Buyers are a lot more price sensitive now. And sellers can’t keep trying to inch the bar higher, or their house will sit without any offers.

Here’s what this says about today’s market. Buyers are a lot more price sensitive now. And sellers can’t keep trying to inch the bar higher, or their house will sit without any offers.

Homeowners who expect to bring in more than their neighbors did last year may be setting themselves up for a longer, more frustrating experience.

And while homeowners are starting to realize prices can’t keep climbing at such a rapid pace, the hiccup is that list prices aren’t actually coming down yet as a result. They’re hanging around, holding steady. And sellers who make this mistake are often holding onto hope that they’ll be able to eek a few more dollars out of their sale. But that’s the problem right there.

If you want to sell today, you need to be in line with where the market is today. Not last year. Not during the pandemic. Today.

Because buyers will skip over homes that feel overpriced, even if it’s only by a little. It’s not that they aren’t interested. It’s just that in a market with more homes to choose from, buyers can be more selective, and sellers don’t get the same benefit of the doubt. If your house isn’t priced to sell, buyers just move on. They’ve got other options anyway.

4 Signs Your Price May Be Too High

You may already be feeling this yourself. If your home is listed and you’re not seeing results, watch for these common red flags noted by Bankrate:

- You’re not getting many showings

- You haven’t gotten any offers (or you’ve only gotten lowball offers)

- Buyers that do come to see your house leave overly negative feedback

- Your house has been sitting on the market longer than the average for your area

If any of these sound familiar, know that waiting it out won’t fix it. But adjusting your price will.

So, What’s the Solution?

Work with your agent to make sure your house is positioned for today’s market. Depending on your what’s happening in your local area, a few weeks without traction can raise questions for buyers about whether your price is realistic. And don’t worry – it doesn’t have to be a big drop. Even a small adjustment can be enough to bring the right buyers through the door.

And if you’re worried you won’t get the high-ticket sale price you thought you would be able to land, keep in mind that your equity has probably grown quite a bit. Chances are, you’re still ahead of the game simply because you invested in a home over the last 5, 10, or more years. You’re still winning when you sell today.

Bottom Line

Patience isn’t a strategy. Pricing is.

If your home isn’t moving, the market is telling you something – and the right price can change everything. Your house will sell, if you price it strategically.

Talk to your agent about what buyers are willing to pay right now to make sure your home stands out for all the right reasons.

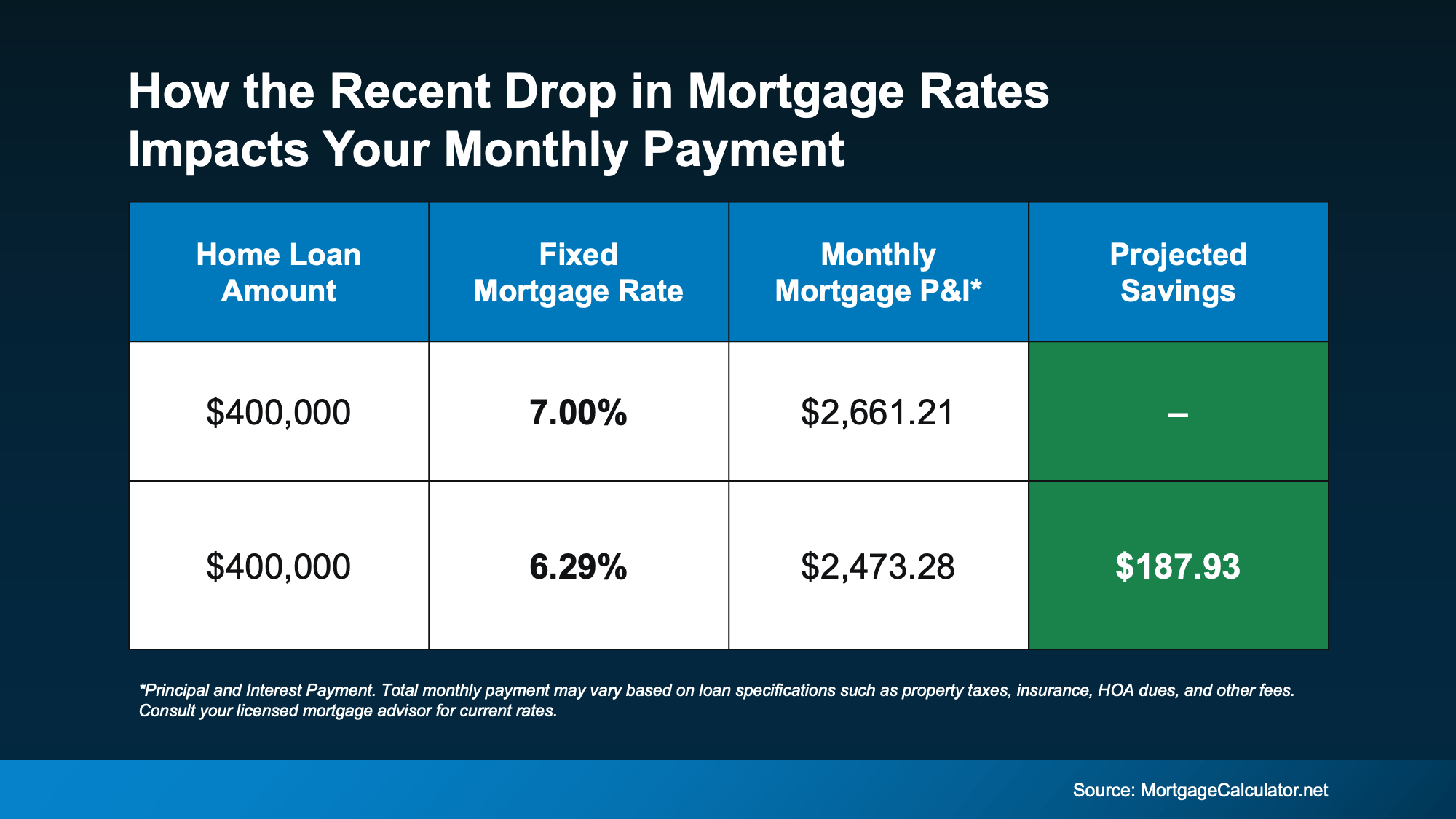

Mortgage Rates Just Saw Their Biggest Drop in a Year

You’ve been waiting for what feels like forever for mortgage rates to finally budge. And last week, they did – in a big way.

On Friday, September 5th, the average 30-year fixed mortgage rate fell to the lowest level since October 2024. It was the biggest one-day decline in over a year.

What Sparked the Drop?

According to Mortgage News Daily, this was a reaction to the August jobs report, which came out weaker-than-expected for a second month in a row. That sent signals across the financial markets, and then mortgage rates came down as a result.

Basically, we’re seeing signs the economy may be slowing down, and as certainty grows in the direction the economy is going, the markets are reacting to what is likely ahead. That historically brings mortgage rates down.

Why Buyers Should Pay Attention Now

But this isn’t just about one day of headlines or one report. It’s about what the drop means for you.

This recent change saves you money when you buy a home. The chart below shows you an example of what a monthly mortgage payment (principal and interest) would be at 7% (where mortgage rates were in May) versus where rates roughly are now:

Compared to just 4 months ago, your future monthly payment would be almost $200 less per month. That’s close to $2,400 a year in savings.

Compared to just 4 months ago, your future monthly payment would be almost $200 less per month. That’s close to $2,400 a year in savings.

How Long Will It Last?

That really depends on where the economy and inflation go from here. Rates could drop lower, or they could inch up slightly.

So, make sure you’re connected with a good agent and trusted lender. They’ll keep a close eye on inflation indicators, job market updates, and reactions to upcoming Fed policy to gauge where mortgage rates may go from here.

But for now, focus on this. While no one can say for sure where rates are headed, the fact that rates broke out of their months-long rut is a good thing. If you’ve been feeling stuck, this could make the start of a new chapter. As Diana Olick, Senior Real Estate and Climate Correspondent at CNBC, says:

“Rates are finally breaking out of the high 6% range, where they’ve been stuck for months.”

And that’s gives you more reason to hope than you’ve had in quite some time.

Bottom Line

This is the shift you’ve been waiting for.

Mortgage rates just saw their biggest decline in over a year. And if rates stay near this level, it could make a home you couldn’t afford just a few months ago feel possible again.

What would today’s rates save you on your future monthly payment? Let’s connect so you can find out.

Homes for Sale at Highest Number Since 2020!

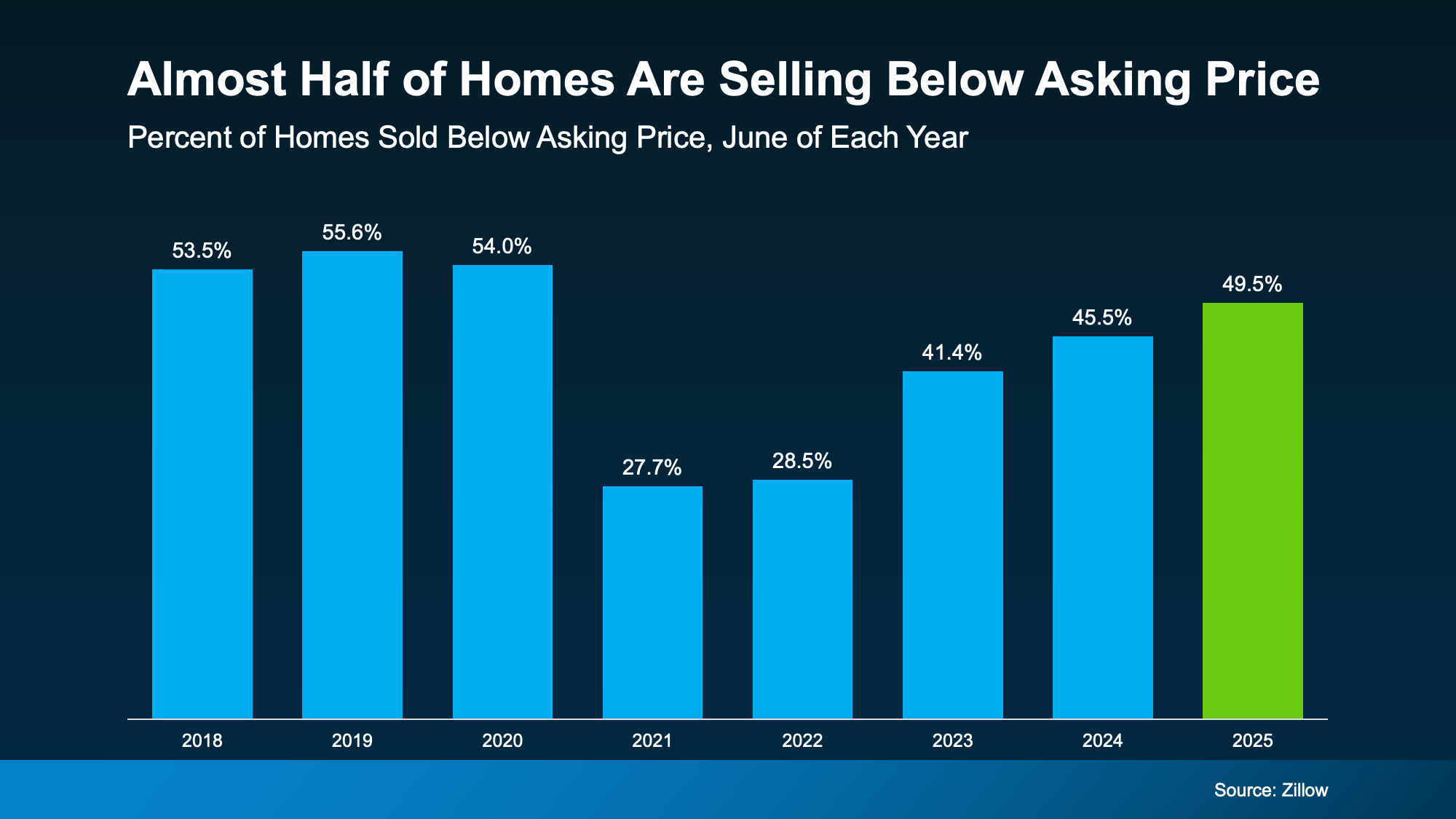

Why 50% of Homes Are Selling for Under Asking and How To Avoid It

If your selling strategy still assumes you’ll get multiple offers over asking, it’s officially time for a reset. That frenzied seller’s market is behind us. And here are the numbers to prove it.

From Frenzy to “Normal”

Right now, about 50% of homes on the market are selling for less than their asking price, according to the latest data from Cotality.

But that isn’t necessarily bad news, even if it feels like it. Here’s why. The wild run-up over the last few years was never going to be sustainable. The housing market needed a reset, and data shows that’s exactly what’s happening right now.

The graph below uses data from Zillow to show how this trend has shifted over time. Here’s what it tells us:

- 2018–2019: 50–55% of homes sold under asking. That was the norm.

- 2021–2022: Only 25% sold under asking, thanks to record-low rates and intense buyer demand.

- 2025: 50% of homes are selling below asking. That’s much closer to what’s typical in the housing market.

Why This Matters If You’re Selling Your House

Why This Matters If You’re Selling Your House

Why This Matters If You’re Selling Your House

Why This Matters If You’re Selling Your HouseIn this return to normal, your pricing strategy is more important than ever.

A few years ago, you could overprice your house and still get swarmed with offers. But now, buyers have more options, tighter budgets, and less urgency.

Today, your asking price can be make or break for your sale, especially right out of the gate. Your first two weeks on the market are the most important window because that’s when the most serious buyers are paying attention to your listing. Miss your price during that crucial period, and your sale will grind to a halt. Buyers will look right past it. And once your listing sits long enough to go stale, it’ll be hard to sell for your asking price.

The Ideal Formula

Basically, sellers who cling to outdated expectations end up dealing with price cuts, lower offers, and a longer time just sitting on the market. But homeowners who understand what’s happening are still winning, even today.

Because that stat about 50% of homes selling for under asking also means the other half are selling at or above – as long as they’re priced right from the start.

So, how do you set yourself up for success? Do these 3 things:

- Prep your house. Tackle essential repairs and touch-ups before you list. If your house looks great, you’ll have a better chance to sell at (or over) your asking price.

- Price strategically from day one. Don’t rely on what nearby homes are listed for. Lean on your agent for what they’ve actually sold for. And price your house based on that.

- Stay flexible. Be ready to negotiate. And know that it doesn’t always have to be on price. It may be on repairs, closing costs, or some other detail. But know this: today’s serious buyers expect some give-and-take.

If you want your house to be one that sells for at (or even more than) your asking price, it’s time to plan for the market you’re in today – not the one we saw a few years ago. And that’s exactly why you need a stand-out local agent.

Bottom Line

You don’t want to fall behind in this market.

So, let’s talk about what buyers in our area are paying right now. With local expertise and a strategy that gets your house noticed in those crucial first two weeks, anything is possible.

Want to know what your house would sell for?

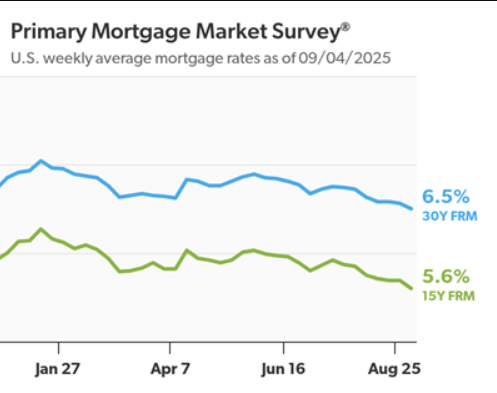

30-Year Mortgage Rate Trends Down

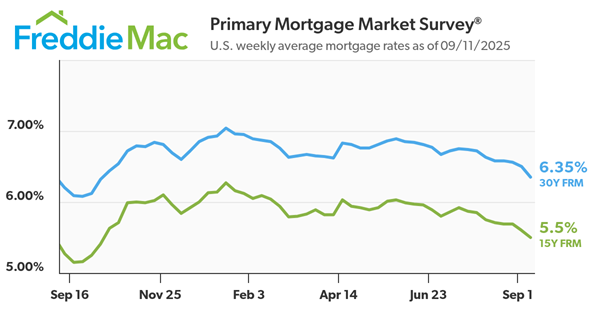

Freddie Mac today released the results of its Primary Mortgage Market Survey® (PMMS®), showing the 30-year fixed-rate mortgage (FRM) averaged 6.50%.

“Mortgage rates continue to trend down, increasing optimism for new buyers and current owners alike,” said Sam Khater, Freddie Mac’s Chief Economist. “As rates continue to drop, the number of homeowners who have the opportunity to refinance is expanding. In fact, the share of market mortgage applications that were for a refinance reached nearly 47%, the highest since October.”

- The 30-year FRM averaged 6.50% as of September 4, 2025, down from last week when it averaged 6.56%. A year ago at this time, the 30-year FRM averaged 6.35%.

- The 15-year FRM averaged 5.60%, down from last week when it averaged 5.69%. A year ago at this time, the 15-year FRM averaged 5.47%.

The PMMS® is focused on conventional, conforming, fully amortizing home purchase loans for borrowers who put 20% down and have excellent credit.

Builder Incentives Reach 5-Year High

Even with more homes on the market right now, some buyers are still having a tough time finding the right one at the right price. Maybe the layout feels off. Maybe it still needs some updating. Or maybe it’s just more of the same.

That’s why more buyers are turning to new construction – and finding some of the best deals available today.

Why? Today, many builders have more homes that are finished and sitting on the market than normal. And that means they’re motivated to sell. They’re running a business, and they don’t want to sit on their inventory. They want to sell it before they build more homes. And that can definitely work in your favor.

As Lance Lambert, Co-Founder of ResiClub, puts it:

“In housing markets where unsold completed inventory has built up, many homebuilders have pulled back on their spec builds—and many are doing bigger incentives or outright price cuts to move unsold inventory.”

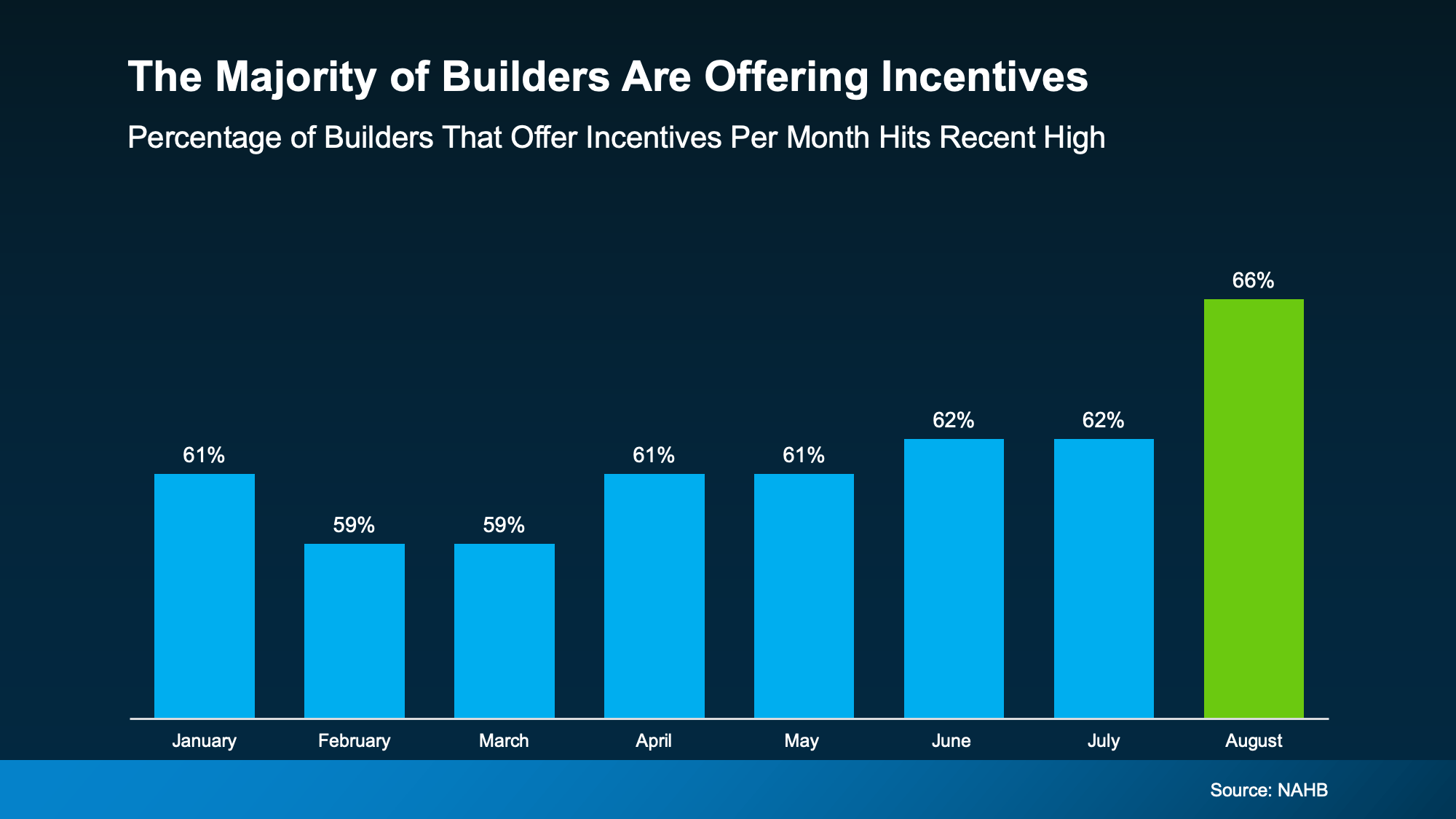

Incentives Are the Highest They’ve Been in 5 Years

Data from the National Association of Home Builders (NAHB) shows 66% of builders offered sales incentives in August. That’s the peak so far this year, and the highest percentage we’ve seen in 5 years.

That means 2 out of every 3 builders are offering something extra to get deals done. And when builders throw in incentives, it’s the buyers like you who win.

That means 2 out of every 3 builders are offering something extra to get deals done. And when builders throw in incentives, it’s the buyers like you who win.

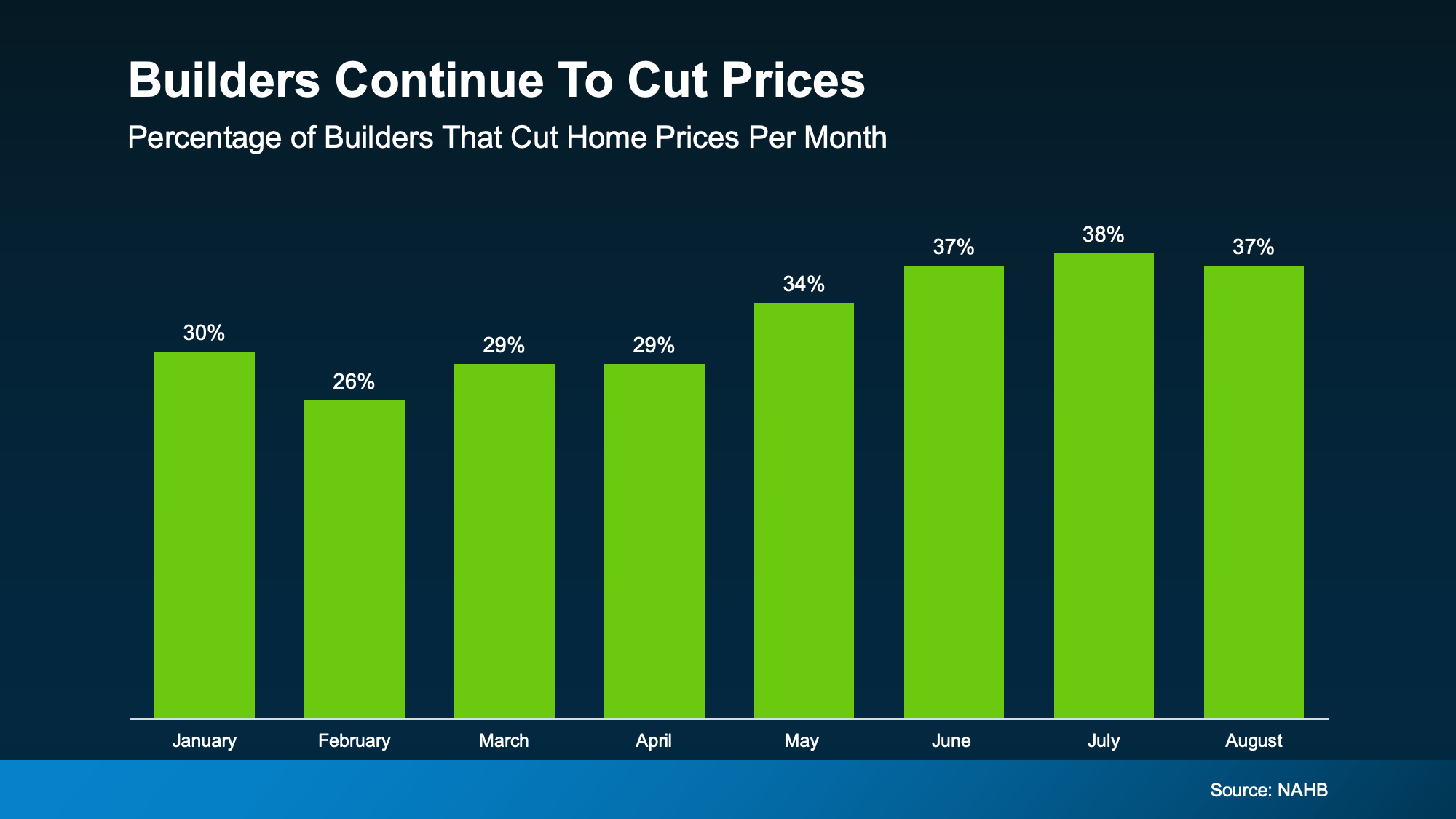

Price Cuts Are Back on the Table

One of the most common incentives they’re offering right now is adjusting the price. According to NAHB, almost 40% of builders are doing price cuts (see graph below):

On average they’re taking off about 5% off the purchase price of the house. For a buyer, 5% could be the difference between reluctantly settling and finally getting a home that works for you.

On average they’re taking off about 5% off the purchase price of the house. For a buyer, 5% could be the difference between reluctantly settling and finally getting a home that works for you.

Take a $500,000 house as an example. If builders reduce the price by 5%, you’re saving $25,000.

And even if the builder you’re interested in won’t budge on price, they’ve got plenty of other levers to pull. As Realtor.com explains:

“. . . there are deals to be found in the market for new homes, with builders increasingly willing to negotiate on price or offer incentives such as rate buydowns and closing cost assistance.”

Why This Matters for You

As a buyer, you probably have a clear vision for your ideal home. Because you’re not just buying any house. You’re buying your house. The one with the space, features, and lifestyle you’ve been hoping for. New builds can check those boxes since they usually have:

- Bigger kitchens and open layouts

- Energy efficiency (hello lower utility bills)

- Smart-home upgrades

- Fewer repair headaches on day one

And today’s incentives make buying a new home more attainable than it’s been in years.

One Word of Advice: Don’t Go At It Alone

If you want to take advantage of this opportunity, just be sure to use your own agent. Builder reps aren’t there to save you money. They protect the builder’s bottom line. That’s why you need to bring your agent with you. Your agent will:

- Cut through the sales pitch and run the cold hard numbers

- Spot which incentives are actually worth it (and which ones are fluff)

- Handle negotiations so you walk away with the best deal possible

- Keep your best interest as their top priority

Bottom Line

If you’re not finding a home you love, the new home market is buzzing with opportunity. With record-high incentives, price cuts in play, and builders itching to move inventory, this is the best time in years to buy new construction.

Curious how far today’s incentives could stretch your budget? Let’s connect so you can see what builders are offering in our area.

Can Mortgage Delinquencies Tell Us About the Future of Foreclosures?

You may be seeing headlines about how foreclosures are rising. And if that makes you nervous that we’re headed for another crash, here’s what you should know.

According to ATTOM, during the housing crash, over nine million people went through some sort of distressed sale (2007-2011). Last year, there were just over 300,000.

So, even with the increase lately, we’re talking about numbers that are dramatically lower. But what does the future hold? Is a wave coming? The short answer is, no.

Here’s why. Experts in the industry look at mortgage delinquencies (loans that are more than 30 days past due) as an early sign for potential foreclosures down the line. And the latest data for delinquencies is reassuring about the market overall.

Right now, delinquencies as a whole are consistent with where we ended last year, which means we’re not seeing the kind of increase that would signal widespread trouble.

But there are some key indicators to continue to watch. Marina Walsh, Vice President of Industry Analysis at the Mortgage Bankers Association, explains:

“While overall mortgage delinquencies are relatively flat compared to last year, the composition has changed.”

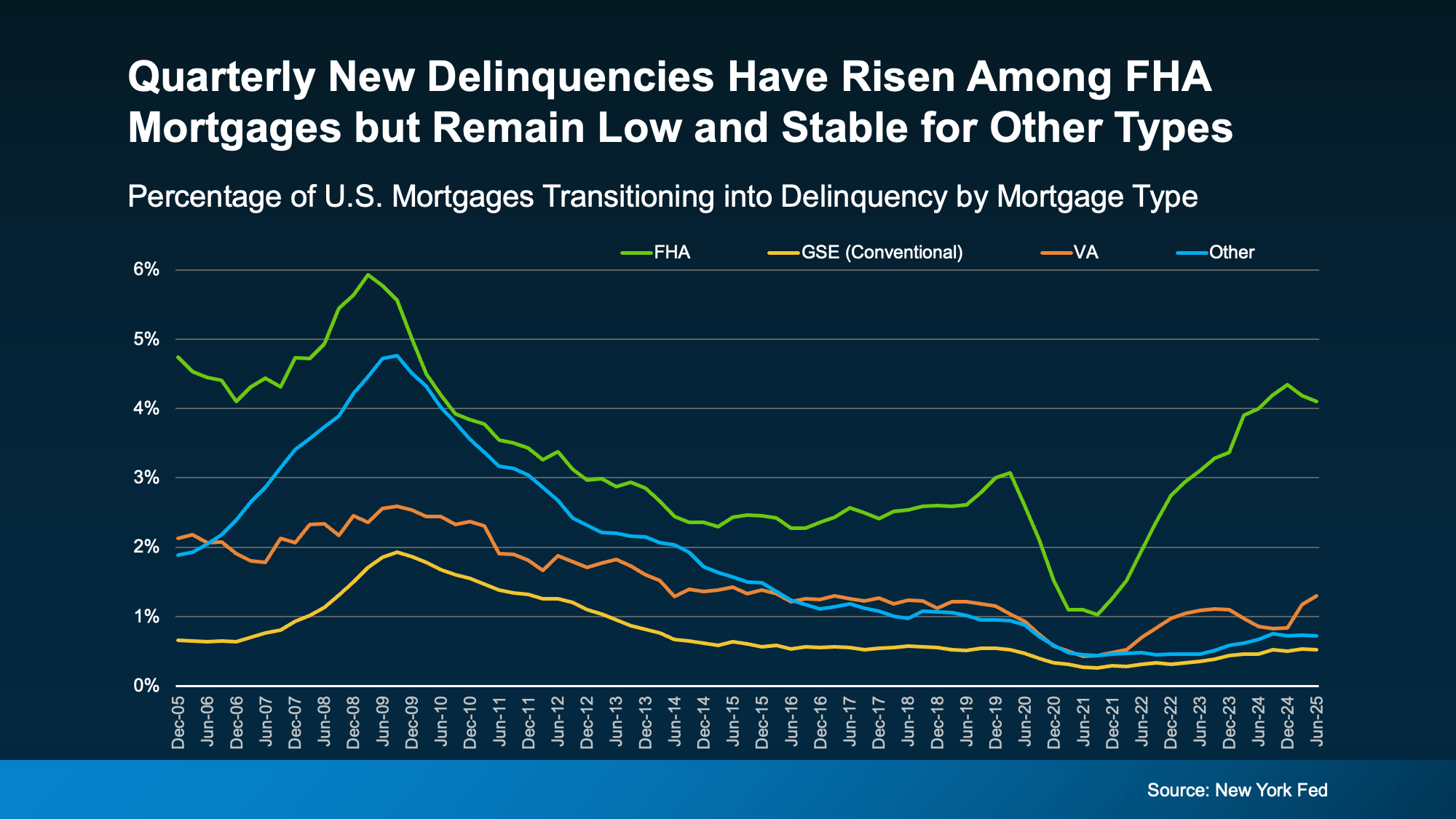

Right now, borrowers with FHA mortgages currently make up the biggest share of new delinquencies (see graph below):

And here’s why that may be happening. Borrowers with FHA mortgages may be more sensitive to shifts in the economy. And with recession fears, stubborn inflation, employment challenges, and more, it makes sense this segment of the market may be feeling it a bit more. But that doesn’t mean it’s a signal a crash is coming.

And here’s why that may be happening. Borrowers with FHA mortgages may be more sensitive to shifts in the economy. And with recession fears, stubborn inflation, employment challenges, and more, it makes sense this segment of the market may be feeling it a bit more. But that doesn’t mean it’s a signal a crash is coming.

If you look back at the graph, it shows, while there are more FHA loans experiencing hardship than the norm, delinquency rates for other loan types remain low and stable. Back during the crash, delinquency rates were significantly elevated for all 4 categories.

That means the broader mortgage market is on much stronger footing than it was back in 2008. As ResiClub says:

“The recent uptick in mortgage delinquency seems to be concentrated among FHA borrowers, however, mortgage performance remains very solid when viewed in light of the twenty-year history of our data.”

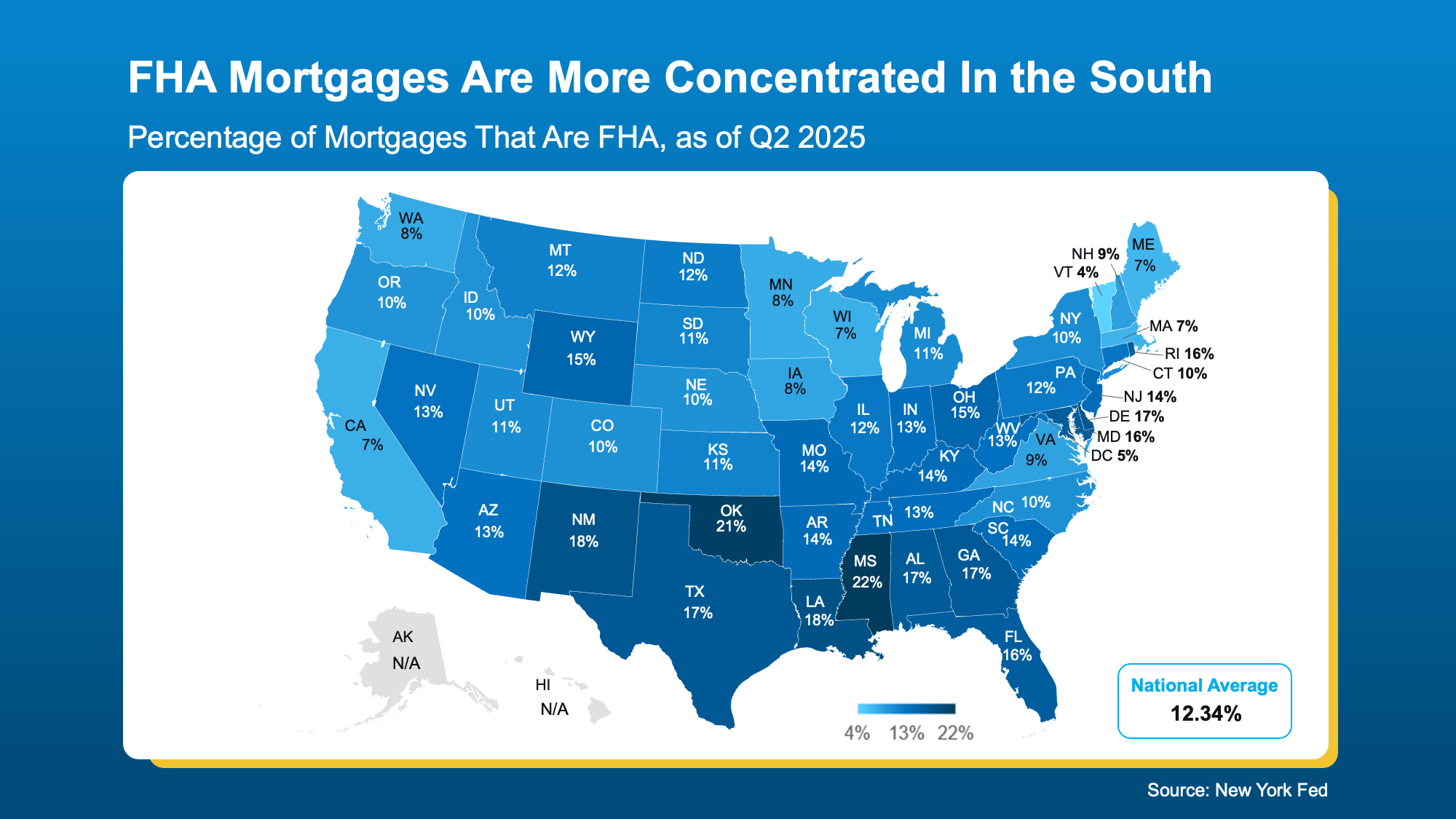

The Region with the Most FHA Loans

Here’s another reason this isn’t a signal of trouble ahead. FHA loans only make up about 12% of all home loans nationwide. But like anything else in housing, local data matters. There are some regions of the country where there are more of this type of loan than others, particularly the South.

The map below does not show how many FHA loans are delinquent. It just shows the overall concentration of FHA loans by state, so you can see which regions have the greatest volume (see map below):

As the Federal Reserve Bank of New York explains:

As the Federal Reserve Bank of New York explains:

“Looking at geographic concentrations of loans, recent data indicate that a higher proportion of mortgage balances are delinquent in many of the southern states . . . we see that higher delinquency rates coincide with a higher share of FHA loans across states.”

Just remember, even the delinquencies rates we’re seeing now aren’t as high as they were in 2008. Again, this is not a signal of a crisis. But it is something experts will monitor in the months ahead.

If You’re Experiencing Financial Hardship

No one wants to see anyone face the challenges of foreclosure. But just know that, if you’re a homeowner struggling with payments, you’re not alone – and you do have options.

The first step is reaching out to your mortgage provider. In many cases, you may be able to set up a repayment plan or explore loan modifications to help you stay on track. And for many homeowners today, you may also have enough equity to sell your house and avoid foreclosure. Odds are, at least some of these delinquencies will go that route since homeowners today have near record amounts of equity in their homes. It may be worth seeing if that could be an option for you too.

Bottom Line

Foreclosures are rising slightly, but they’re nowhere near the levels of 2008. And delinquency trends don’t point to a crash ahead.

This is something industry professionals are going to watch in the days ahead. If you want to stay up to date, let’s connect so you always have the latest information.