Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

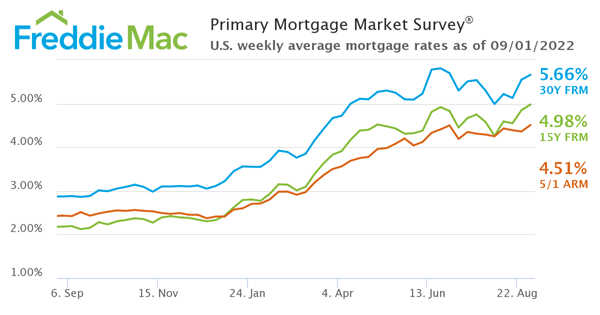

Mortgage Rates Continue Advancing

Freddie Mac (OTCQB: FMCC) today released the results of its Primary Mortgage Market Survey (PMMS), showing that the 30-year fixed-rate mortgage (FRM) averaged 5.66 percent.

“The market’s renewed perception of a more aggressive monetary policy stance has driven mortgage rates up to almost double what they were a year ago,” said Sam Khater, Freddie Mac’s Chief Economist. “The increase in mortgage rates is coming at a particularly vulnerable time for the housing market as sellers are recalibrating their pricing due to lower purchase demand, likely resulting in continued price growth deceleration.”

- 30-year fixed-rate mortgage averaged 5.66 percent with an average 0.8 point as of September 1, 2022, up from last week when it averaged 5.55 percent. A year ago at this time, the 30-year FRM averaged 2.87 percent.

- 15-year fixed-rate mortgage averaged 4.98 percent with an average 0.8 point, up from last week when it averaged 4.85 percent. A year ago at this time, the 15-year FRM averaged 2.18 percent.

- 5-year Treasury-indexed hybrid adjustable-rate mortgage (ARM) averaged 4.51 percent with an average 0.4 point, up from last week when it averaged 4.36 percent. A year ago at this time, the 5-year ARM averaged 2.43 percent.

New Homes May Have the Incentives You’re Looking for Today

According to the U.S. Census Bureau, this year, builders are on pace to complete more than a million new homes in this country. If you’ve had trouble finding a home to buy over the past year, it may be time to work with your trusted agent to consider a new build and the incentives that come with it. Here’s why.

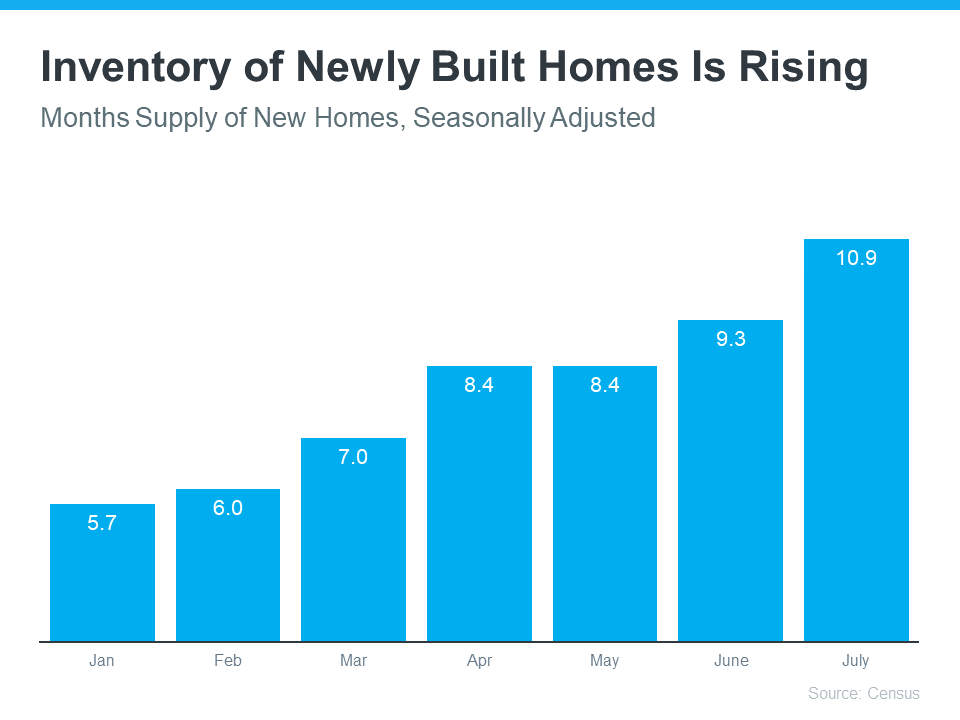

The Supply of Newly Built Homes Is Rising

When looking for a home, you can choose between existing homes (those that are already built and previously owned) and newly constructed ones. While the inventory of existing homes is on the rise today, it’s still in tight supply, meaning it can be challenging to find just the right one.

The inventory of newly built homes, however, is also rising. And with more options available than there have been in years, a new home may be just the answer you’re looking for. The graph below shows just how much the supply of newly built homes has grown this year.

And here’s the thing – builders are also keeping a close eye on current market trends. With mortgage rates rising this year and, as a result, buyer demand softening, builders are slowing their pace of new construction. That’s because they learned their lesson in the housing crash of 2008 and want to avoid over-building and having too much inventory in their pipeline.

Basically, while there are more newly built homes on the market today than there have been in years, many builders want to sell their current inventory before adding much more – and that’s where you can really benefit. Today, builders may be more willing to work with buyers. According to a recent survey, 83% of builders have reduced their prices over the last three months.

What That Means for You

The current supply of newly built homes for sale coupled with the fact that data shows the majority of builders are doing price reductions are both great news for you. It means you may have more options and possibly some much-needed relief if you consider newly built homes in your search.

Bottom Line

If you’re ready to buy, it may be time to look for a newly built home. To learn what’s available in our area and what incentives these builders are offering, let’s connect today.

This article provided by Keeping Current Matters. The information contained, and the opinions expressed, in this article are not intended to be construed as investment advice. Keeping Current Matters, Inc. does not guarantee or warrant the accuracy or completeness of the information or opinions contained herein. Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision. Keeping Current Matters, Inc. will not be liable for any loss or damage caused by your reliance on the information or opinions contained herein.

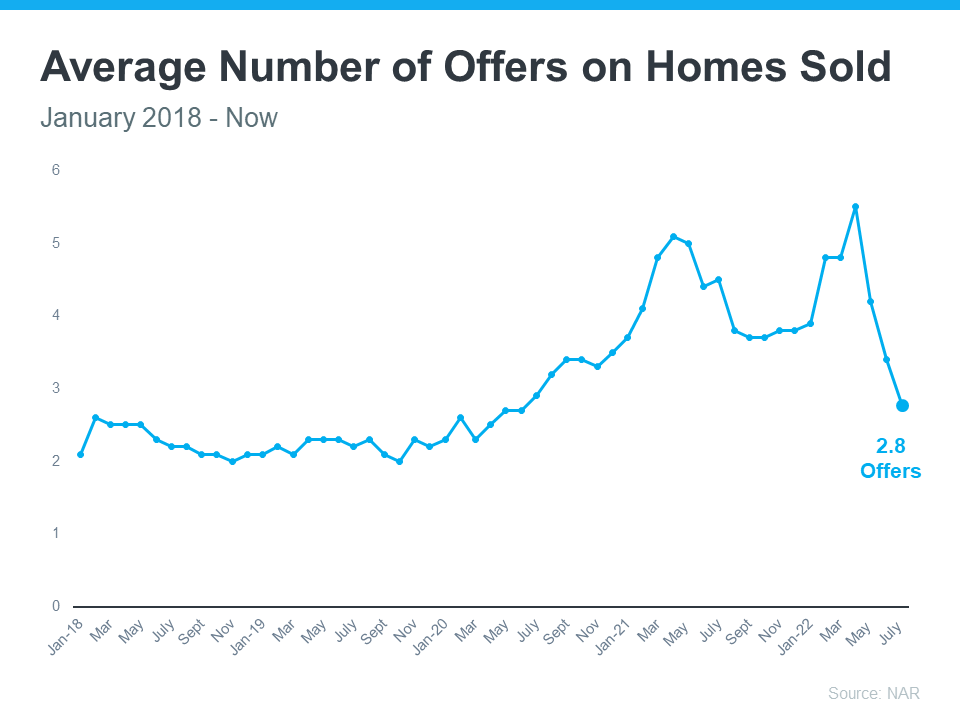

Less Competition as Bidding Wars Ease

One of the top stories in recent real estate headlines was the intensity and frequency of bidding wars. With so many buyers looking to purchase a home and so few of them available for sale, fiercely competitive bidding wars became the norm during the pandemic – and it drove home prices up. If you tried to buy a house over the past two years, you probably experienced this firsthand and may have been outbid on several homes along the way.

But here’s the news you’ve been waiting for: data shows clear signs bidding wars are easing this year.

According to the National Association of Realtors (NAR), the average number of offers on recently sold homes has declined considerably over the past few months (see graph below):

The graph shows homes were seeing a high of around five offers earlier this year. But the latest data shows that average was down to just shy of three offers per recently sold home. This shift is happening largely because rising mortgage rates moderated buyer demand and slowed home sales, resulting in a growing supply of homes on the market. Essentially, more choices for buyers.

What This Means for You

If you put your home search on pause because you were outbid last year or because you didn’t want to deal with the peak intensity of bidding wars, you can breathe a welcome sigh of relief. While it’s still a sellers’ market, an uptick in inventory gives you a window of opportunity to jump back in. You may still be competing with some buyers, but it likely won’t be anything like it was just a few short months ago.

Bottom Line

If you put your plans on pause because of intense bidding wars in recent years, it may be time to kick off your home search. Today, bidding wars are easing and that may mean less competition for you as a buyer. If you’re serious about buying a home or making a move, let’s connect to get started today.

This article provided by Keeping Current Matters. The information contained, and the opinions expressed, in this article are not intended to be construed as investment advice. Keeping Current Matters, Inc. does not guarantee or warrant the accuracy or completeness of the information or opinions contained herein. Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision. Keeping Current Matters, Inc. will not be liable for any loss or damage caused by your reliance on the information or opinions contained herein.

Home Price Deceleration?

One of the biggest questions people are asking right now is: what’s happening with home prices? There are headlines about ongoing price appreciation, but at the same time, some sellers are reducing the price of their homes. That can feel confusing and makes it more difficult to get a clear picture.

Part of the challenge is that it can be hard to understand what experts are saying when the words they use sound similar. Let’s break down the differences among those terms to help clarify what’s actually happening today.

- Appreciation is when home prices increase.

- Depreciation is when home prices decrease.

- Deceleration is when home prices continue to appreciate, but at a slower or more moderate pace.

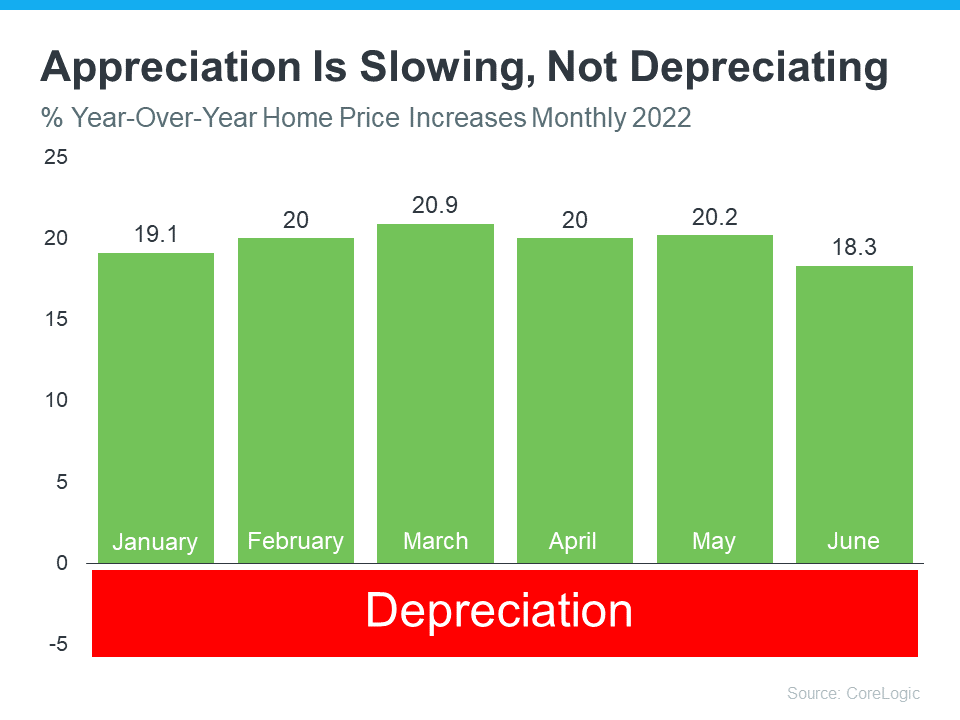

Experts agree that, nationally, what we’re seeing today is deceleration. That means home prices are appreciating, just not at the record-breaking pace they have over the past year. In 2021, data from CoreLogic tells us home prices appreciated by an average of 15% nationwide. And earlier this year, that appreciation was upward of 20%. This year, experts forecast home prices will appreciate at a decelerated pace of around 10 to 11%, on average.

The graph below uses the latest data from CoreLogic to help tell the story of how home prices are decelerating, but not depreciating so far this year.

As the green bars show, home prices appreciated between 19-20% year-over-year from January to March. But over the last few months, the pace of that appreciation has decelerated to 18%. This means price growth is still climbing compared to last year but at a slower rate.

As the Monthly Mortgage Monitor from Black Knight explains:

“Annual home price growth dropped by nearly two percentage points . . . – the greatest single-month slowdown on record since at least the early 1970s. . . While June’s slowdown was record-breaking, home price growth would need to decelerate at this pace for six more months to drive annual appreciation back to 5%, a rate more in line with long-run averages.”

Basically, this means, while moderating, home prices are still far above the norm, and we’d have to see a lot more deceleration to even fall in line with more typical rates of home price growth. That’s still not home price depreciation.

The big takeaway is home prices haven’t fallen or depreciated nationwide, they’re just decelerating or moderating. While some unique and overheated markets may see declines, nationally, home prices are forecast to appreciate. And when we look at the country as a whole, none of the experts project home prices will net depreciate or fall. They’re all projecting ongoing appreciation.

Bottom Line

If you have questions about what’s happening with home prices in our local area, let’s connect.

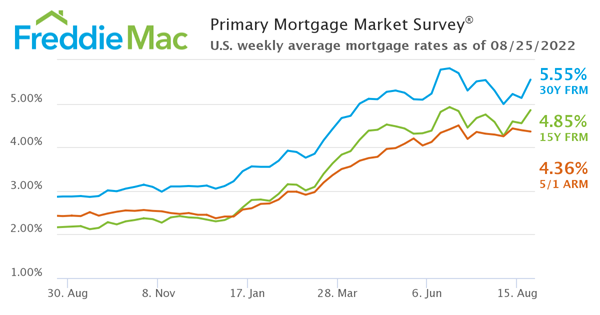

Mortgage Interest Rates Climb Higher

Freddie Mac today released the results of its Primary Mortgage Market Survey® for the week ending August 28, 2022, showing that the 30-year fixed-rate mortgage (FRM) averaged 5.55 percent.

“The combination of higher mortgage rates and the slowdown in economic growth is weighing on the housing market,” said Sam Khater, Freddie Mac’s Chief Economist. “Home sales continue to decline, prices are moderating, and consumer confidence is low. But, amid waning demand, there are still potential homebuyers on the sidelines waiting to jump back into the market.”

- 30-year fixed-rate mortgage averaged 5.55 percent with an average 0.8 point as of August 25, 2022, up from last week when it averaged 5.13 percent. A year ago at this time, the 30-year FRM averaged 2.87 percent.

- 15-year fixed-rate mortgage averaged 4.85 percent with an average 0.8 point, up from last week when it averaged 4.55 percent. A year ago at this time, the 15-year FRM averaged 2.17 percent.

- 5-year Treasury-indexed hybrid adjustable-rate mortgage (ARM) averaged 4.36 percent with an average 0.4 point, down from last week when it averaged 4.39 percent. A year ago at this time, the 5-year ARM averaged 2.42 percent.

For more information on daily mortgage interest rate movements, check with your mortgage lender. You can also find information online at sites such as Mortgage News Daily.

You May Want To Start Your Home Search Today

If you’re thinking about buying a home, you likely have a lot of factors on your mind. You’re weighing your own needs against higher mortgage rates, today’s home prices, and more to try to decide if you want to jump into the market. While some buyers may wait things out, there’s a reason serious buyers are making moves right now, and that’s the growing number of homes for sale.

So far this year, housing inventory has been increasing and that’s making the prospect of finding your dream home less difficult. While there are always reasons you could delay making a big decision, there are also always reasons to consider moving forward. And having a growing number of options for your home search may be exactly what you needed to feel more confident in making a move.

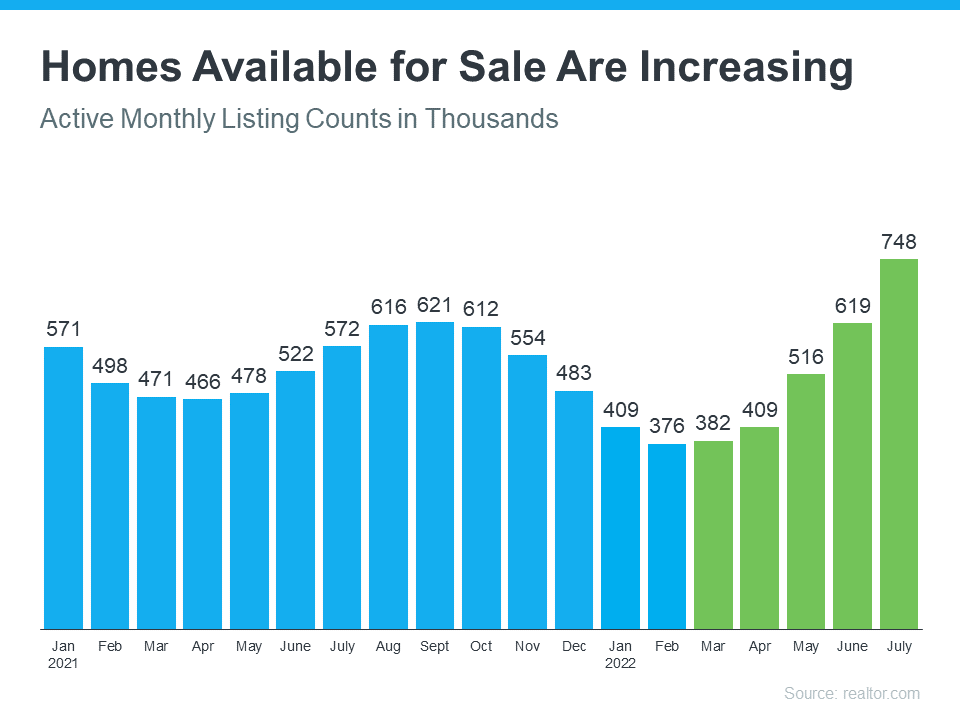

What’s Causing Housing Inventory To Grow?

As new data comes out, we’re getting an updated picture of why housing supply is increasing so much this year. As Bill McBride, Author of Calculated Risk, explains:

“We are seeing a significant change in inventory, but no pickup in new listings. Most of the increase in inventory so far has been due to softer demand – likely because of higher mortgage rates.”

Basically, the inventory growth is primarily from homes staying on the market a bit longer (known as active listings). And that’s happening because higher mortgage rates and home prices have helped moderate the peak frenzy of buyer demand.

The graph below uses data from realtor.com to show how much active listings have risen over the past five months as a result (shown in green):

Why This Growth Is Good News for You

Regardless of the source, the increase in available housing supply is good for buyers. More housing supply actively for sale means you have more options as your search for your next home. A recent article from realtor.com explains just how significant the inventory growth has been and why it’s good news for your plans to buy:

“Nationally, the inventory of homes actively for sale on a typical day in July increased by 30.7% over the past year, the largest increase in inventory in the data history and higher than last month’s growth rate of 18.7% which was itself record-breaking. This amounted to 176,000 more homes actively for sale on a typical day in July compared to the previous year and more choice for buyers who are still looking for a new home.”

The growth this year is certainly good news for you, especially if you’ve had trouble finding a home that meets your needs. If you start your search today, those additional options should make it less difficult to find a home than it would have been over the past two years.

Bottom Line

If you’re ready to jump into the market and take advantage of the increasing supply of homes for sale, let’s connect today. The opportunity is knocking, will you answer?

Why Today’s Housing Inventory Shows the Market Isn’t Headed for a Crash

Whether or not you owned a home in 2008, you likely remember the housing crash that took place back then. And news about an economic slowdown happening today may bring all those concerns back to the surface. While those feelings are understandable, data can help reassure you the situation today is nothing like it was in 2008.

One of the key reasons why the market won’t crash this time is the current undersupply of inventory. Housing supply comes from three key places:

- Current homeowners putting their homes up for sale

- Newly built homes coming onto the market

- Distressed properties (short sales or foreclosures)

For the market to crash, you’d have to make a case for an oversupply of inventory headed to the market, and the numbers just don’t support that. So, here’s a deeper look at where inventory is coming from today to help prove why the housing market isn’t headed for a crash.

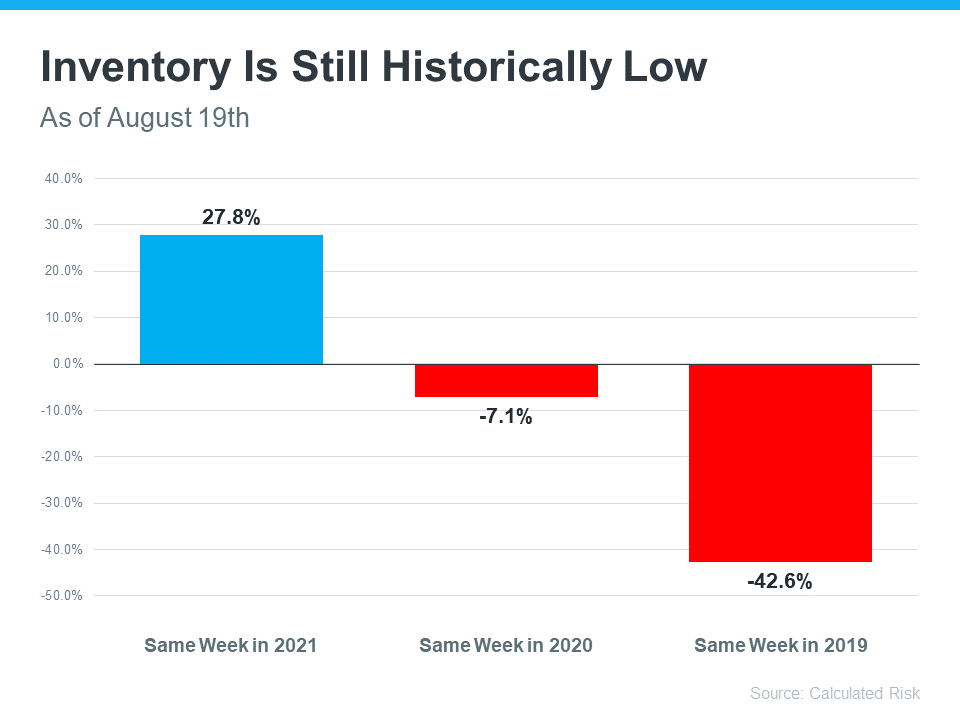

Current Homeowners Putting Their Homes Up for Sale

Even though housing supply is increasing this year, there’s still a limited number of existing homes available. The graph below helps illustrate this point. Based on the latest weekly data, inventory is up 27.8% compared to the same week last year (shown in blue). But compared to the same week in 2019 (shown in the larger red bar), it’s still down by 42.6%.

So, what does this mean? Inventory is still historically low. There simply aren’t enough homes on the market to cause prices to crash. There would need to be a flood of people getting ready to sell their houses in order to tip the scales toward a buyers’ market. And that level of activity simply isn’t there.

Newly Built Homes Coming onto the Market

There’s also a lot of talk about what’s happening with newly built homes today, and that may make you wonder if we’re overbuilding. But home builders are actually slowing down their production right now. Ali Wolf, Chief Economist at Zonda, notes:

“It has become a very competitive market for builders where they are trying to offload any standing inventory.”

To avoid repeating the overbuilding that happened leading up to the housing crisis, builders are reacting to higher mortgage rates and softening buyer demand by slowing down their work. It’s a sign they’re being intentional about not overbuilding homes like they did during the bubble.

And according to the latest data from the U.S. Census, at today’s current pace, we’re headed to build a seasonally adjusted annual rate of about 1.4 million homes this year. While this will add more inventory to the market, it’s not on pace to create an oversupply because builders today are more cautious than the last time when they built more homes than the market could absorb.

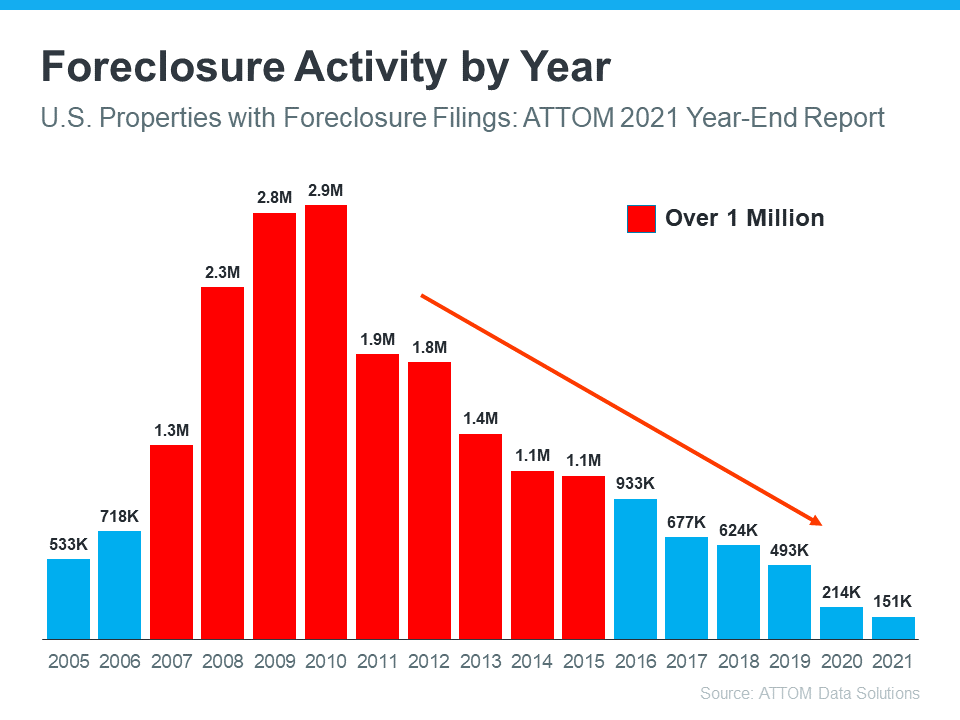

Distressed Properties (Short Sales or Foreclosures)

The last place inventory can come from is distressed properties, including short sales and foreclosures. Back in the housing crisis, there was a flood of foreclosures due to lending standards that allowed many people to secure a home loan they couldn’t truly afford. Today, lending standards are much tighter, resulting in more qualified buyers and far fewer foreclosures. The graph below uses data from ATTOM Data Solutions on properties with foreclosure filings to help paint the picture of how things have changed since the crash:

This graph shows how in the time around the housing crash there were over one million foreclosure filings per year. As lending standards tightened since then, the activity started to decline. And in 2020 and 2021, the forbearance program was a further aid to help prevent a repeat of the wave of foreclosures we saw back around 2008.

That program was a game changer, giving homeowners options for things like loan deferrals and modifications they didn’t have before. And data on the success of that program shows four out of every five homeowners coming out of forbearance are either paid in full or have worked out a repayment plan to avoid foreclosure. These are a few of the biggest reasons there won’t be a wave of foreclosures coming to the market.

Bottom Line

Although housing supply is growing this year, the market certainly isn’t anywhere near the inventory levels that would cause prices to drop significantly. That’s why inventory tells us the housing market won’t crash.

Selling? What You Need To Know in Today’s Housing Market

If you’re thinking about selling your house, you may have heard about the housing market slowing down in recent months. While it’s still a sellers’ market, the peak frenzy the market saw over the past two years has cooled some. If you’re asking yourself if you’ve missed your chance to sell your house and make a move, the good news is you haven’t – motivated buyers are still out there. But you do need to price your house right for today’s market. Here’s why.

As Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), says:

“Homes priced right are selling very quickly, but homes priced too high are deterring prospective buyers.”

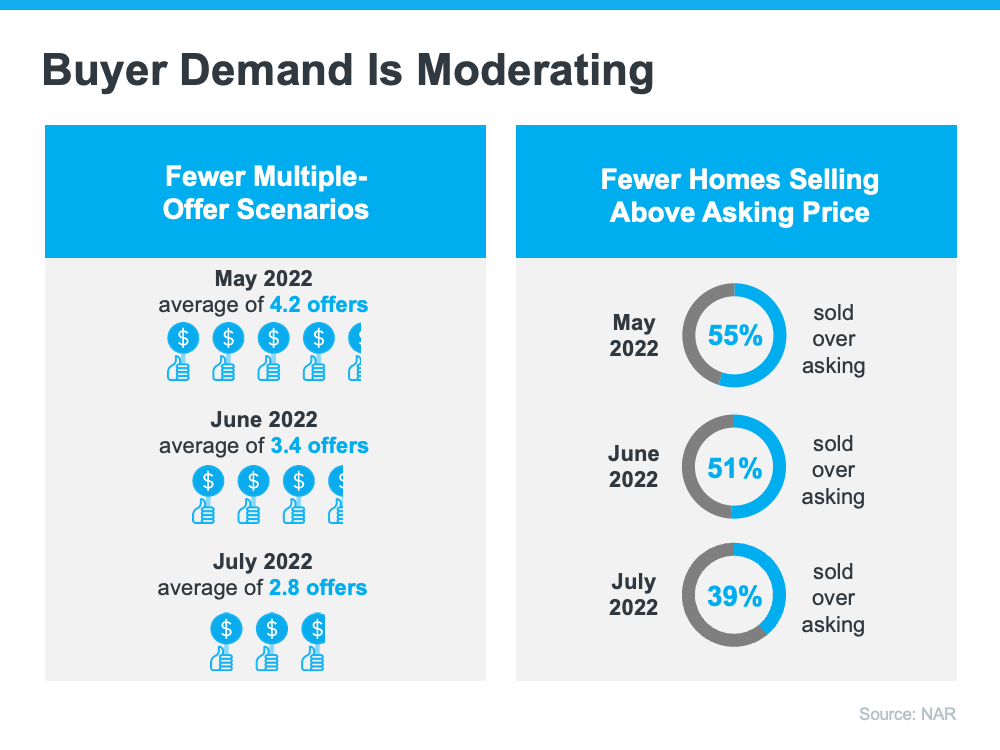

It’s true buyer demand has slowed over the past few months as higher mortgage rates made it more expensive to buy a home. The result is fewer bidding wars and less competition among buyers (see visual below):

But don’t forget – that’s compared to the severely overheated market we saw over the past two years. According to the latest Confidence Index from NAR:

“. . . 39% of homes sold above list price, down from 51% a month ago and 50% a year ago.”

While this is a slower pace than even one month ago, serious buyers are still actively in the market, and they’re buying homes that are priced right. In fact, the Confidence Index also notes the average home is selling in just 14 days.

If you’re aiming to sell your house, be sure you’re working with your agent to price it for today’s housing market. As buyer demand softens, it’s important to understand this isn’t the same market as last year. It’s not even the same market as just a few months ago. But it is still a sellers’ market.

If you’re ready to sell your house, seek the advice of a real estate professional. In some cases, you’ll need to adjust your expectations accordingly to meet the market where it is today. Selma Hepp, Interim Lead, Deputy Chief Economist at CoreLogic, explains what’s happening and what it means when you sell:

“Signs of a broader slowdown in the housing market are evident, . . . This is in line with our previous expectations and given the notable cooling of buyer demand due to higher mortgage rates. . . . Nevertheless, buyers still remain interested, which is keeping the market competitive — particularly for attractive homes that are properly priced.”

Bottom Line

While the housing market has cooled from its overheated frenzy, it’s still a sellers’ market. Let’s connect so you understand what’s happening with buyer demand and home prices in our local area as you get ready to enter the market.