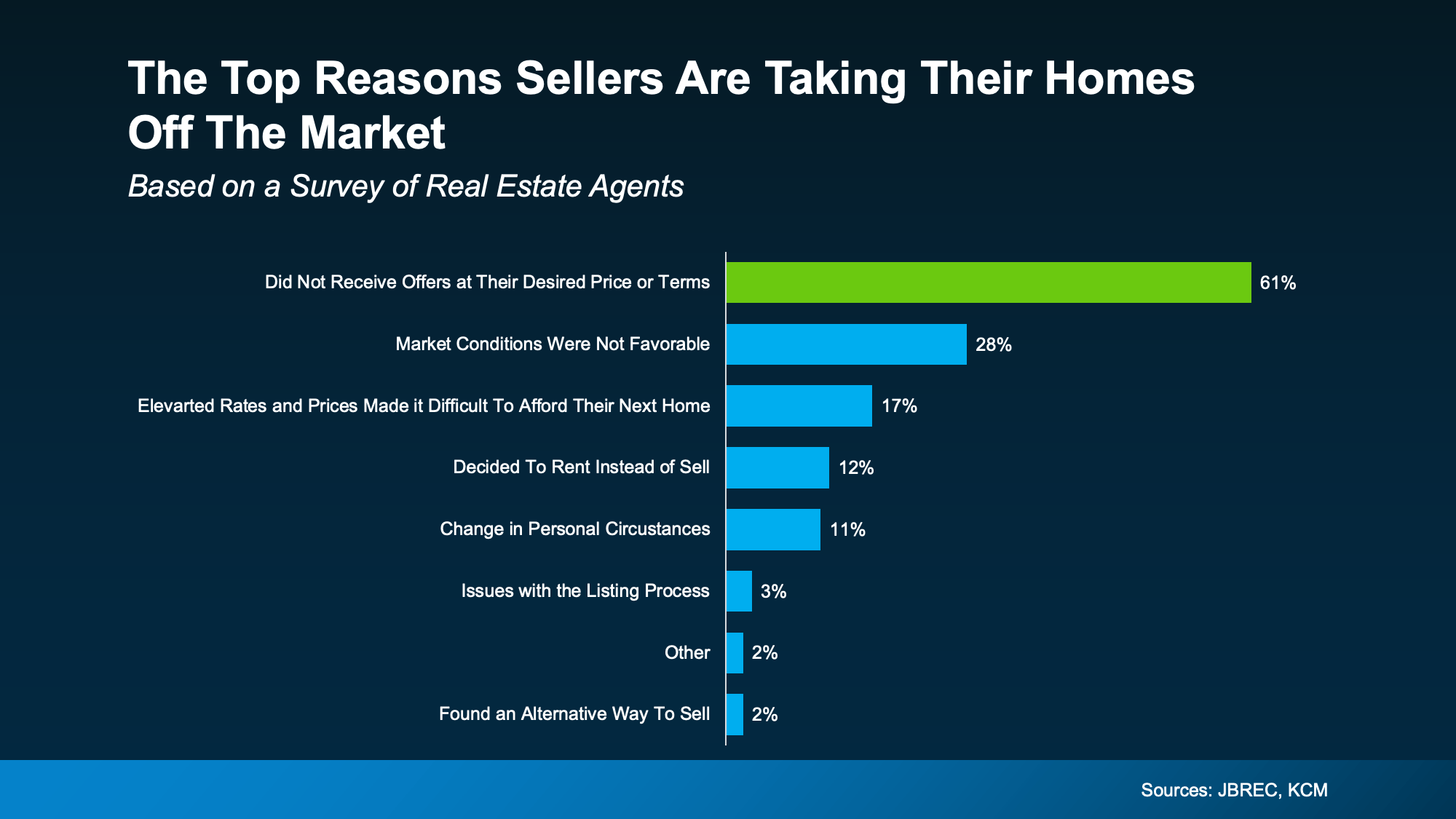

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

If it feels like you’re seeing new construction signs pop up everywhere, you’re not wrong. Builders have been busy. And it’s left some people wondering: Are we overbuilding like we did right before the 2008 housing crash?

No matter what you may hear in the news, there’s no reason for alarm. In reality, data shows builders aren’t racing ahead, they’re actually starting to tap the brakes.

Builders Are Pulling Back, Not Piling On

Permits (applications to start building new homes) are one of the best early indicators for what’s next for home construction. And right now, building permits are trending down, not up. Here’s why that’s so important.

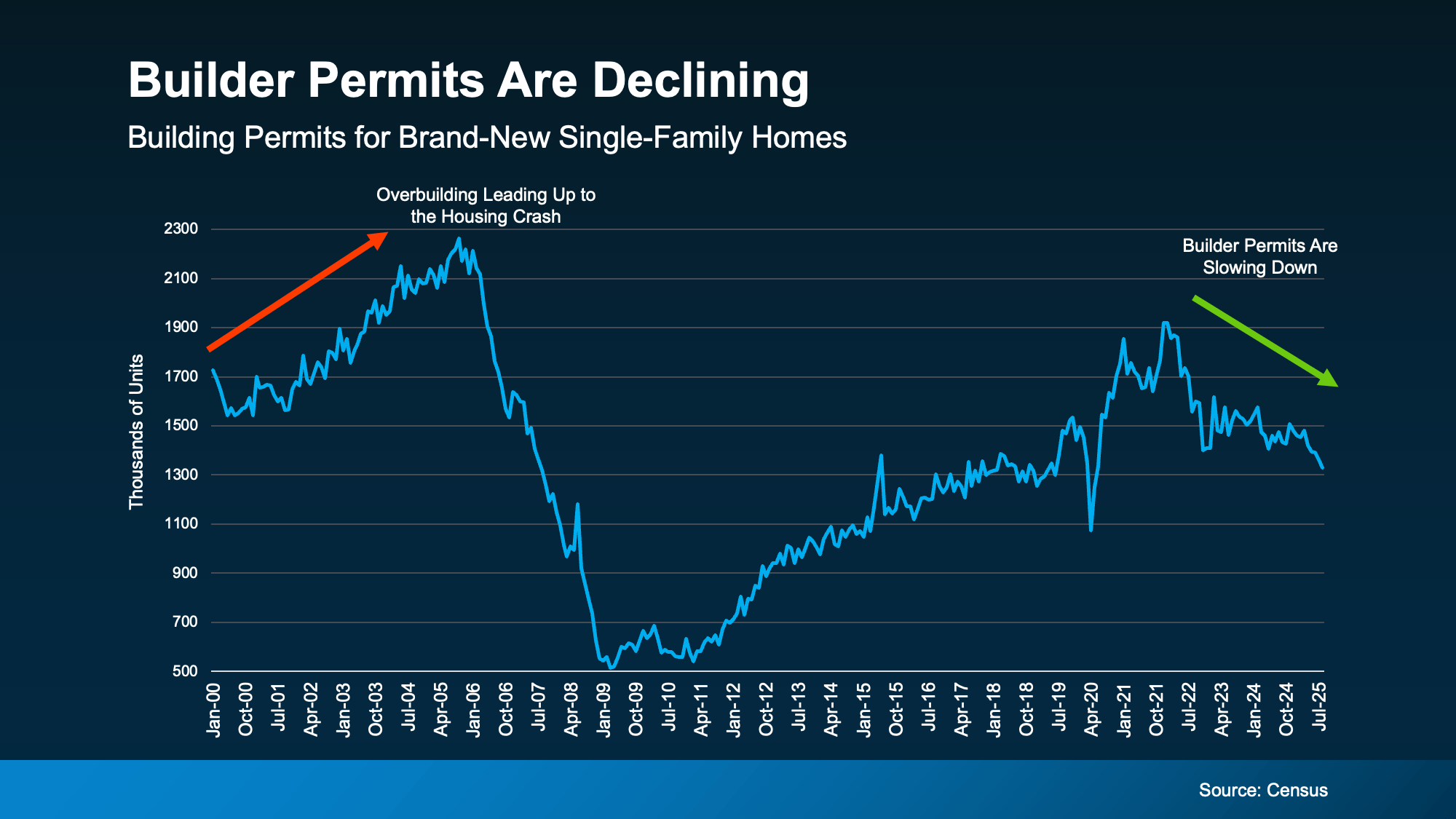

In the years before the housing crash of 2008, builders really ramped up their production of single-family homes (the red arrow in the graph below). And unfortunately, they built far more homes than the market actually needed. That oversupply led to falling home prices. That’s what so many people remember, and what they worry will happen again.

But while construction has been picking back up since roughly 2012, we’re not headed for a repeat of the same mistakes. The latest data available shows builders are actually starting construction on fewer homes right now (the green arrow in the graph below):

New data from the National Association of Home Builders (NAHB) confirms that trend. It shows that single-family building permits have fallen for eight straight months.

New data from the National Association of Home Builders (NAHB) confirms that trend. It shows that single-family building permits have fallen for eight straight months.

The Slowdown Isn’t Random, It’s Intentional

Basically, builders are watching and reacting to today’s economic conditions and buyer demand in real time. And they’re pumping the brakes on their pipelines to avoid getting caught with too much unsold inventory. As Ali Wolf, Chief Economist at Zonda, says:

“. . . builders are still working through their backlog of inventory but are more cautious with new starts.”

That’s a big contrast to what happened before the housing crash, when overconfidence led to record-breaking levels of new home construction – even as demand was dropping. Today’s builders aren’t overconfident. They’re listening to the market and adjusting before things get out of balance.

The Regional Picture Tells the Same Story

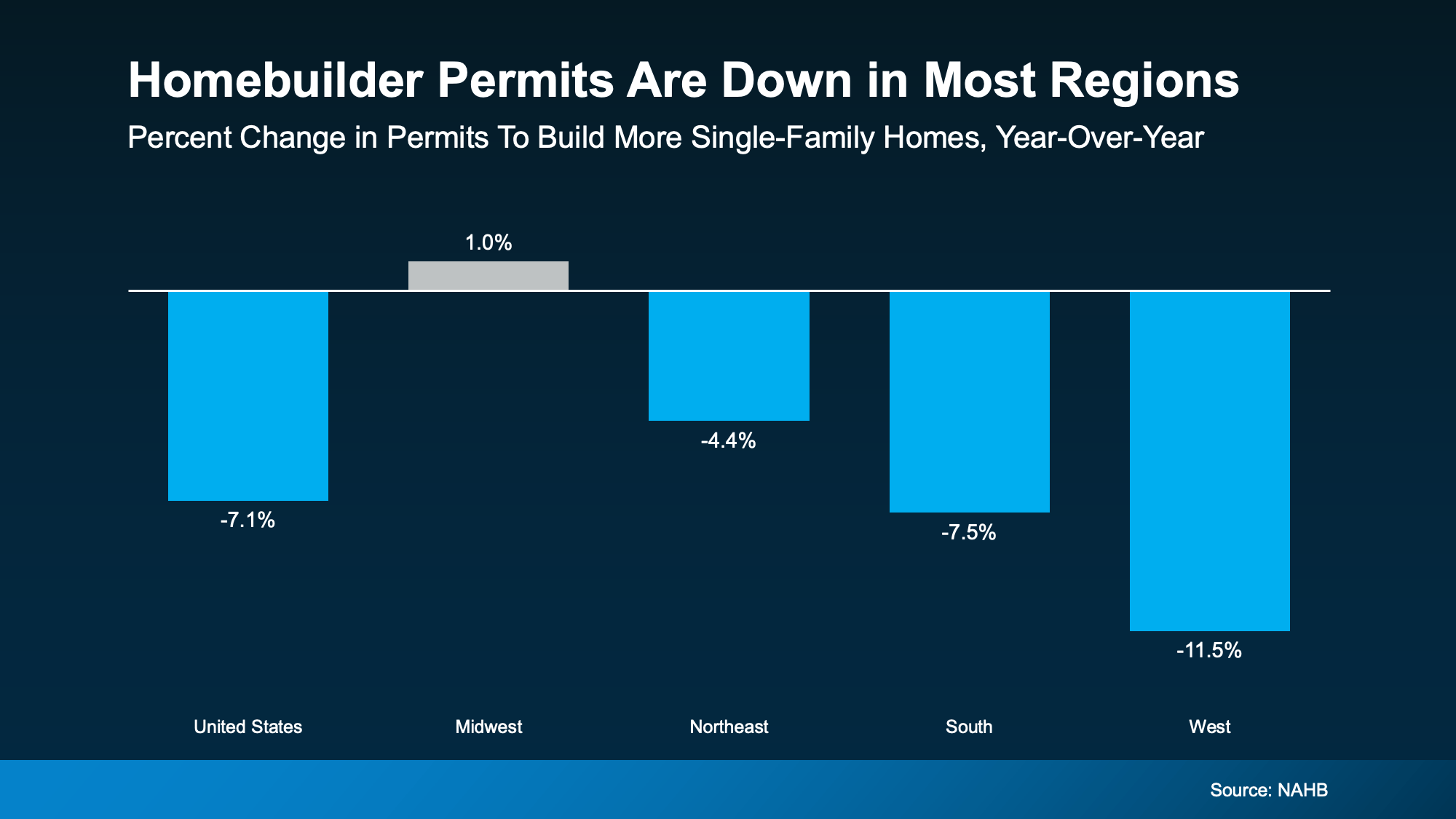

And while inventory is going to vary a lot based on where you live, if you zoom out and look at regional data, the pattern holds almost everywhere (see graph below):

NAHB reports single-family permits are down in nearly every part of the country, with just one region showing a slight uptick. And even there, the growth is so small, it’s practically flat.

NAHB reports single-family permits are down in nearly every part of the country, with just one region showing a slight uptick. And even there, the growth is so small, it’s practically flat.

Why This Isn’t 2008 All Over Again

In the lead up to the crash, builders kept building long after demand had disappeared. This time, they’re slowing down early, and that’s a good thing.

The market actually needs more homes after years of underbuilding. But builders are making sure they don’t have to overcorrect. They’re being intentional about how many homes they’re building right now.

So yes, you’re seeing more new homes for sale today, but that doesn’t mean we’re oversupplied nationally. It means buyers finally have more options, and builders are pacing themselves to keep things in check. They’re not going to flood the market. And that’s a really good thing for housing overall.

Bottom Line

Seeing more new homes for sale doesn’t mean builders are overdoing it. Since building permits have been declining for eight straight months, it’s clear this isn’t an out-of-control boom. It’s a measured recovery.

If you want to know more about what builders are doing in our area, let’s connect.

BrightMLS

BrightMLS