Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Another Welcomed Drop In Mortgage Interest Rates

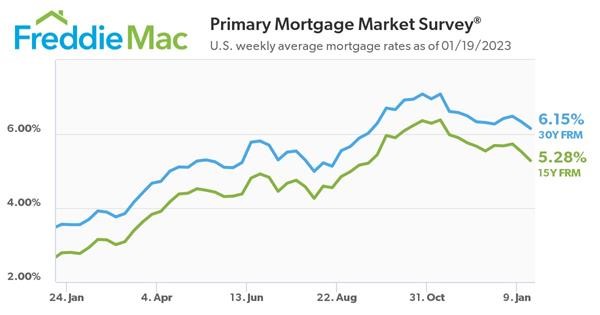

Freddie Mac today released the results of its Primary Mortgage Market Survey® (PMMS®) for the week ending 01/19/2023, showing the 30-year fixed-rate mortgage (FRM) averaged 6.15 percent.

“As inflation continues to moderate, mortgage rates declined again this week,” said Sam Khater, Freddie Mac’s Chief Economist. “Rates are at their lowest level since September of last year, boosting both homebuyer demand and homebuilder sentiment. Declining rates are providing a much-needed boost to the housing market, but the supply of homes remains a persistent concern.”

- 30-year fixed-rate mortgage averaged 6.15 percent as of January 19, 2023, down from last week when it averaged 6.33 percent. A year ago at this time, the 30-year FRM averaged 3.56 percent.

- 15-year fixed-rate mortgage averaged 5.28 percent, down from last week when it averaged 5.52 percent. A year ago at this time, the 15-year FRM averaged 2.79 percent.

The PMMS® is focused on conventional, conforming, fully amortizing home purchase loans for borrowers who put 20 percent down and have excellent credit.

For more information on daily mortgage interest rate movements, check with your mortgage lender. You can also find information on daily mortgage rate movements online on sites such as Mortgage News Daily.

Yes, You Should Get Pre-Approved

I hear this from time to time – I don’t need to get pre-approved. And then I say, “Then you’re really not interested in buying a place, are you?”.

One of the first steps in your homebuying journey is getting pre-approved. To understand why it’s such an important step, you need to understand what pre-approval is and what it does for you. Business Insider explains:

“In a preapproval [sic], the lender tells you which types of loans you may be eligible to take out, how much you may be approved to borrow, and what your rate could be.”

Basically, pre-approval gives you critical information about the homebuying process that’ll help you understand your options and what you may be able to borrow.

How does it work? As part of the pre-approval process, a lender will look at your finances to determine what they’d be willing to loan you. From there, your lender will give you a pre-approval letter to help you understand how much money you can borrow. That can make it easier when you set out to search for homes because you’ll know your overall numbers. And with higher mortgage rates impacting affordability for many buyers today, a solid understanding of your numbers is even more important.

Pre-Approval Helps Show You’re a Serious Buyer

Another added benefit is pre-approval can help a seller feel more confident in your offer because it shows you’re serious about buying their house. A recent article from Forbes notes:

“From the seller’s perspective, a preapproval [sic] letter from a reputable local lender often can make the difference between accepting and rejecting an offer.”

This goes to show, even though you may not face the intense bidding wars you saw if you tried to buy during the pandemic, pre-approval is still an important part of making a strong offer. In fact, Christy Bieber, Personal Finance Writer at The Motley Fool explains it may be the most important part of making an offer:

“Pre-approval maximizes the chances you’ll be able to actually close the deal – and sellers want to see that.

The fact that a pre-approval gives you a better chance of getting your offer accepted is undoubtedly the most important reason to complete this step . . .”

Bottom Line

Getting pre-approved is an important first step towards buying a home. It lets you know what you can borrow and shows sellers you’re serious about purchasing their home. Connect with a local real estate professional and a trusted lender so you have the tools you need to purchase a home in today’s market.

Have Home Values Bottomed Out?

Whether you’re already a homeowner or you’re looking to become one, the recent headlines about home prices may leave you with more questions than answers. News stories are talking about home prices falling, and that’s raising concerns about a repeat of what happened to prices in the crash in 2008.

One of the questions that’s on many minds, based on those headlines, is: how much will home prices decline? But what you may not realize is expert forecasters aren’t calling for a free fall in prices. In fact, if you look at the latest data, there’s a case to be made that the biggest portion of month-over-month price depreciation nationally may already behind us – and even those numbers weren’t significant declines on the national level. Instead of how far will they drop, the question becomes: have home values hit bottom?

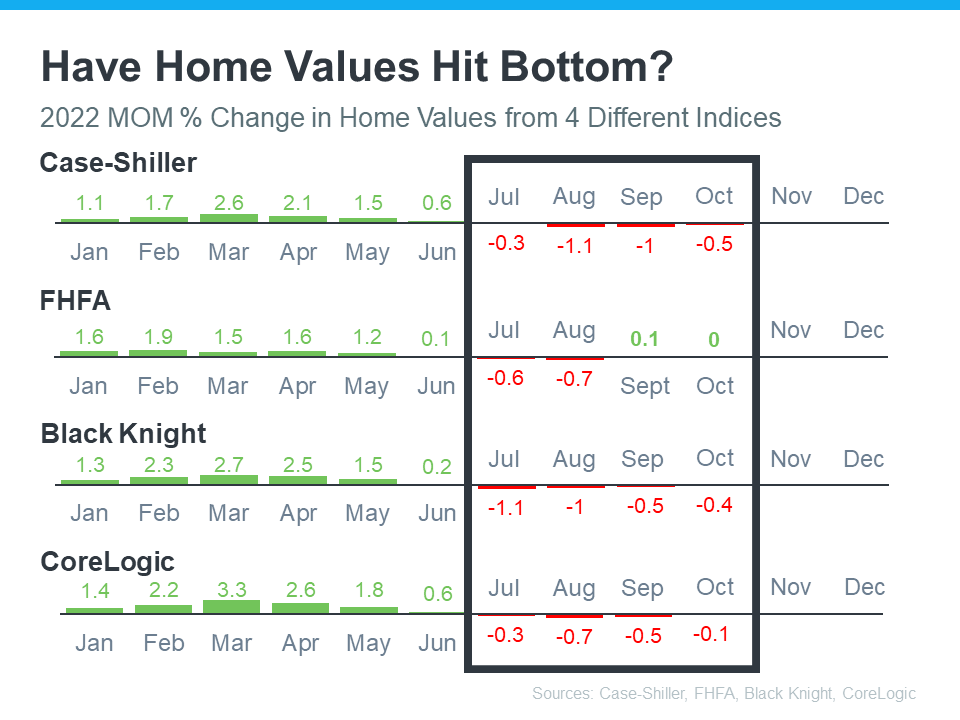

Let’s take a look at the latest data from several reputable industry sources (see chart below):

The chart above provides a look at the most recent reports from Case-Shiller, the Federal Housing Finance Agency (FHFA), Black Knight, and CoreLogic. It shows how, on a national scale, home values have changed month-over-month since January 2022. November and December numbers have yet to come out.

Let’s focus in on what the red numbers tell us. The red numbers are the change in home values over the last four months that have been published. And if we isolate the last four months, what the data shows is, in each case, home price depreciation peaked in August.

While that doesn’t guarantee home price depreciation has hit bottom, it confirms prices aren’t in a free fall, and it may be an early signal that the worst is already behind us. As the numbers for November and December are released, data will be able to further validate this national trend.

Bottom Line

Home prices month-over-month have depreciated for the past four months on record, but there’s a strong case to be made that the worst may be behind us. If you have questions about what’s happening with home prices in our local market, let’s connect.

You Sure You Want To Wait For 3% Mortgage Rates Again?

Last year, the Federal Reserve took action to try to bring down inflation. In response to those efforts, mortgage rates jumped up rapidly from the record lows we saw in 2021, peaking at just over 7% last October. Hopeful buyers experienced a hit to their purchasing power as a result, and some decided to press pause on their plans.

Today, the rate of inflation is starting to drop. And as a result, mortgage rates have dipped below last year’s peak. Sam Khater, Chief Economist at Freddie Mac, shares:

“While mortgage market activity has significantly shrunk over the last year, inflationary pressures are easing and should lead to lower mortgage rates in 2023.”

That’s potentially great news if you’re a buyer aiming to jump back into the housing market. Any drop in mortgage rates helps boost your purchasing power by bringing down your expected monthly mortgage payment. This means the lower mortgage rates experts forecast this year could be just what you need to reignite your homebuying goals.

While this opens up a window of opportunity for you, remember: you shouldn’t expect rates to drop back down to record lows like we saw in 2021. Experts agree that’s not the range buyers should bank on. Greg McBride, Chief Financial Analyst at Bankrate, explains:

“I think we could be surprised at how much mortgage rates pull back this year. But we’re not going back to 3 percent anytime soon, because inflation is not going back to 2 percent anytime soon.”

It’s important to have a realistic vision for what you can expect this year, and that’s where the advice of expert real estate advisors is critical. You may be surprised by the impact even a mild drop in mortgage rates has on your budget. If you’re ready to buy a home now, today’s market presents the opportunity to get a more affordable mortgage rate, find your dream home, and face less competition from other buyers.

Bottom Line

The recent pullback in mortgage rates is great news – but if you’re ready to buy now, holding out for 3% is a mistake. Work with a local lender to learn how today’s rates impact your goals, and let’s connect to explore your options in our area.

Past Recessions Tell Us What About Today’s Housing Market

It doesn’t matter if you’re someone who closely follows the economy or not, chances are you’ve heard whispers of an upcoming recession. Economic conditions are determined by a broad range of factors, so rather than explaining them each in depth, let’s lean on the experts and what history tells us to see what could lie ahead. As Greg McBride, Chief Financial Analyst at Bankrate, says:

“Two-in-three economists are forecasting a recession in 2023 . . .”

As talk about a potential recession grows, you may be wondering what a recession could mean for the housing market. Here’s a look at the historical data to show what happened in real estate during previous recessions to help prove why you shouldn’t be afraid of what a recession could mean for the housing market today.

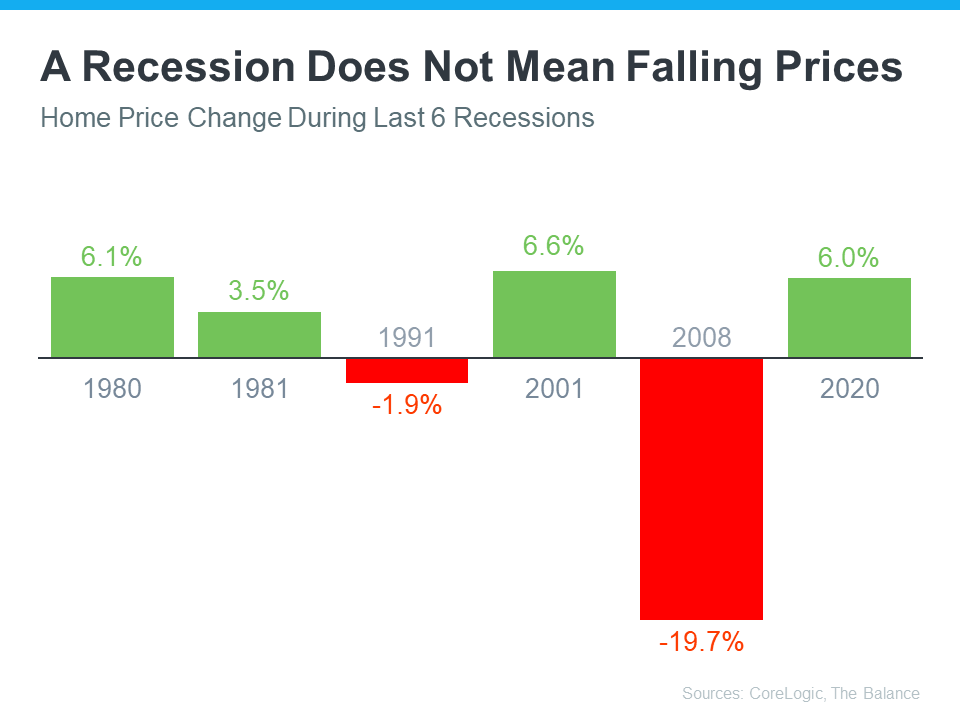

A Recession Doesn’t Mean Falling Home Prices

To show that home prices don’t fall every time there’s a recession, it helps to turn to historical data. As the graph below illustrates, looking at recessions going all the way back to 1980, home prices appreciated in four of the last six of them. So historically, when the economy slows down, it doesn’t mean home values will always fall.

Most people remember the housing crisis in 2008 (the larger of the two red bars in the graph above) and think another recession would be a repeat of what happened to housing then. But today’s housing market isn’t about to crash because the fundamentals of the market are different than they were in 2008. According to experts, home prices will vary by market and may go up or down depending on the local area. But the average of their 2023 forecasts shows prices will net neutral nationwide, not fall drastically like they did in 2008.

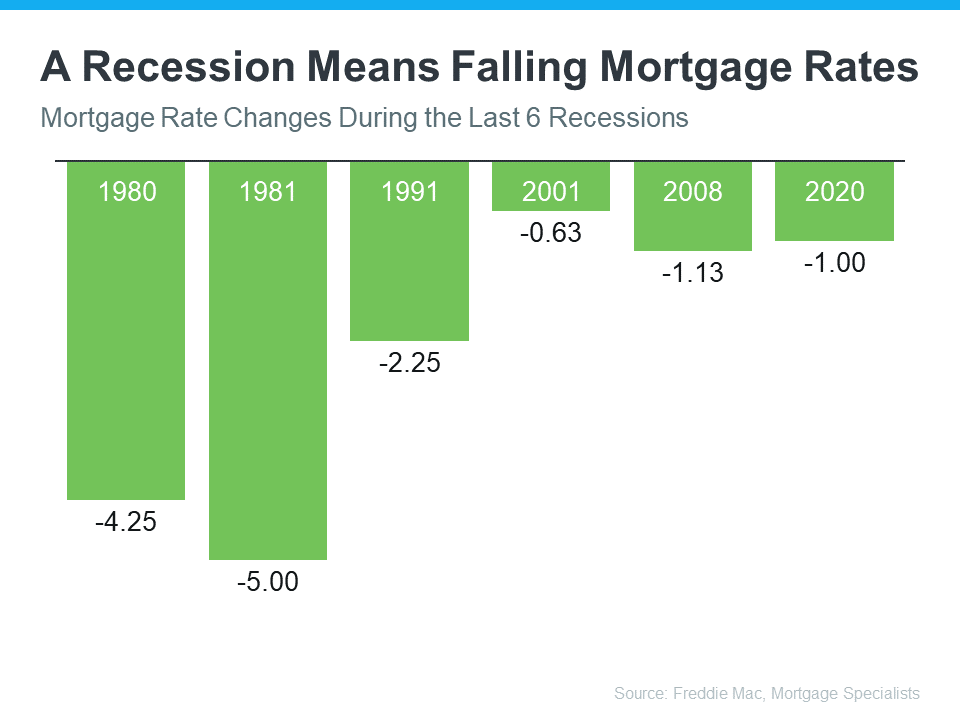

A Recession Means Falling Mortgage Rates

Research also helps paint the picture of how a recession could impact the cost of financing a home. As the graph below shows, historically, each time the economy slowed down, mortgage rates decreased.

Fortune explains mortgage rates typically fall during an economic slowdown:

“Over the past five recessions, mortgage rates have fallen an average of 1.8 percentage points from the peak seen during the recession to the trough. And in many cases, they continued to fall after the fact as it takes some time to turn things around even when the recession is technically over.”

In 2023, market experts say mortgage rates will likely stabilize below the peak we saw last year. That’s because mortgage rates tend to respond to inflation. And early signs show inflation is starting to cool. If inflation continues to ease, rates may fall a bit more, but the days of 3% are likely behind us.

The big takeaway is you don’t need to fear the word recession when it comes to housing. In fact, experts say a recession would be mild and housing would play a key role in a quick economic rebound. As the 2022 CEO Outlook from KPMG, says:

“Global CEOs see a ‘mild and short’ recession, yet optimistic about global economy over 3-year horizon . . .

More than 8 out of 10 anticipate a recession over the next 12 months, with more than half expecting it to be mild and short.”

Bottom Line

While history doesn’t always repeat itself, we can learn from the past. According to historical data, in most recessions, home values have appreciated and mortgage rates have declined.

If you’re thinking about buying or selling a home this year, let’s connect so you have expert advice on what’s happening in the housing market and what that means for your homeownership goals.

You Got This!

![Key Terms To Know When Buying a Home [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2023/01/11164544/Key-Terms-To-Know-When-Buying-A-Home-MEM-1046x2684.png)

Some Highlights

- Buying a home is a major transaction that can seem even more complex when you don’t understand the terms used throughout the process.

- If you’re looking to become a homeowner this year, it’s important to know these housing terms and how they relate to the current market so you feel confident throughout the homebuying process.

- Let’s connect so you have expert answers for any questions as they come up.

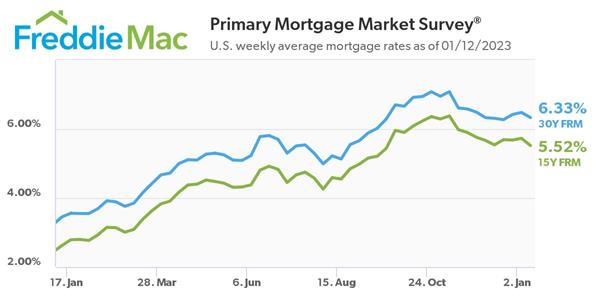

Mortgage Rate Drop

Freddie Mac (OTCQB: FMCC) released the results of its Primary Mortgage Market Survey (PMMS) for the week ending 01/12/2023, showing the 30-year fixed-rate mortgage (FRM) averaged 6.33 percent.

“While mortgage rates have resumed their decline, the market remains hypersensitive to rate movements, with purchase demand experiencing large swings relative to small changes in rates,” said Sam Khater, Freddie Mac’s Chief Economist. “Over the last few weeks latent demand has been on display with buyers jumping in and out of the market as rates move.”

- 30-year fixed-rate mortgage averaged 6.33 percent as of January 12, 2023, down from last week when it averaged 6.48 percent. A year ago at this time, the 30-year FRM averaged 3.45 percent.

- 15-year fixed-rate mortgage averaged 5.52 percent, down from last week when it averaged 5.73 percent. A year ago at this time, the 15-year FRM averaged 2.62 percent.

The PMMS is focused on conventional, conforming, fully amortizing home purchase loans for borrowers who put 20 percent down and have excellent credit

Time To List Your Second Home?

During the pandemic, second homes became popular because of the rise in work-from-home flexibility. That’s because owning a second home, especially in the luxury market, allowed those homeowners to spend more time in their favorite places or with different home features. Keep in mind, a luxury home isn’t only defined by price. In a recent article, Investopedia shares additional factors that push a home into this category: location, such as a home on the water or in a desirable city, and features, the things that make the home itself feel luxurious.

A recent report from the Institute for Luxury Home Marketing (ILHM) explains just how much remote work impacted the demand for second and luxury homes:

“The unprecedented ten-fold increase towards remote work since the pandemic is an historic development that will continue to fuel second home demand for many years to come.”

But what if you bought a second home that you no longer use? If you’re now shifting back into the office or are seeing your priorities and needs change, you may find you’re not utilizing your second home as much. If so, it may be time to sell it.

And if you own what’s considered a luxury home, buyer demand for it may be even greater. In another report, the Institute for Luxury Home Marketing explains:

“. . . the last few years have left their legacy for the luxury market. While it might only represent a small percentage of the overall real estate market, luxury homeownership’s influence is growing. Not only has the purchase of homes valued over $1 million (a figure considered by the National Association of Realtors to be a benchmark for luxury) tripled from 2.6% to 6.5% since 2018, but demand for multiple luxury properties has soared over the last two years.

This phenomenal increase has been driven by a growing affluent demographic who consider owning a luxury property a necessity in their asset portfolio. All indications are that this trend is here to stay, albeit that demand is set to return to a more sustainable level.”

If you own a luxury second home that isn’t being used as much anymore, now’s the time to sell. There are still buyers in the market who are looking for a home like yours today.

Bottom Line

Let’s connect to explore the benefits of selling your second home this year.