Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

You’re ready to sell your house. But what do you need most from your real estate agent? Well, the National Association of Realtors (NAR) asked that very question to recent sellers and found one of the top things they were looking for is help marketing their house to potential buyers. Maybe that’s what you need the most help with too.

You expect your real estate agent to write a great description of your house for the listing and pair it with some high-quality photos. But that’s not all you’re going to get when you partner with a great agent.

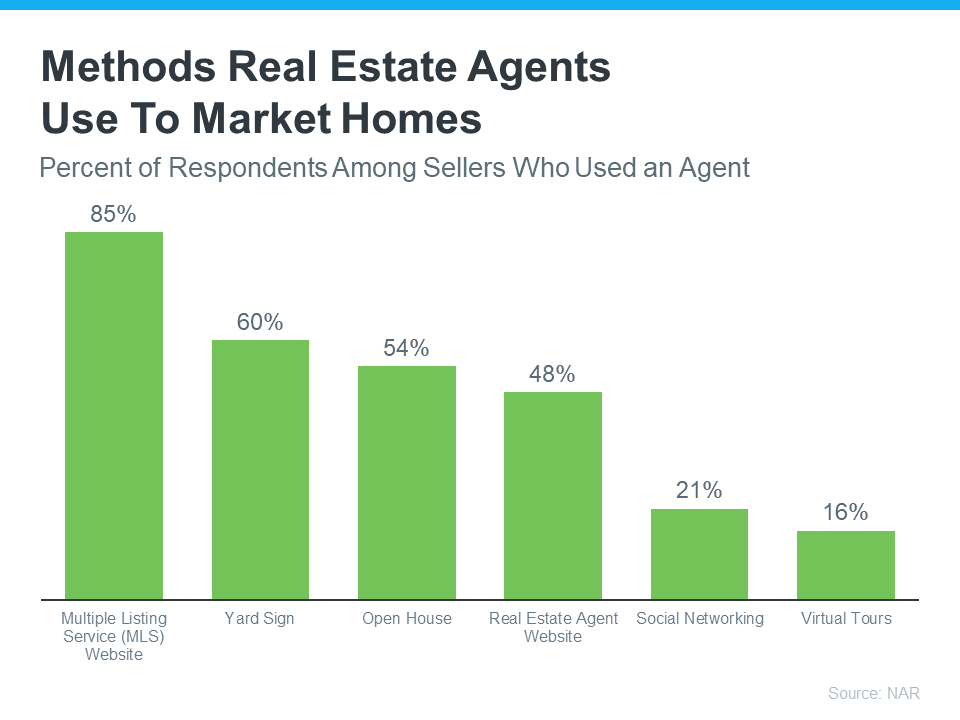

They’ll do a lot more to make sure your house stands out. Here are some of the most common methods real estate agents use to market homes according to that same report from NAR (see graph below):

So, how can you benefit from your agent using these methods?

- Listing on the MLS – By listing your house on the MLS, it will get more visibility from other real estate agents and buyers. This could lead to more traffic, which could ultimately help you see an increase in offers and ultimately a better price.

- Using a Yard Sign – A yard sign catches the eye of people driving or walking by. This method drums up local interest since people who live nearby might have friends or family looking to move into the area. It also prominently displays your agent’s contact information, so interested buyers can get in touch easily.

- Having an Open House – When your agent advertises and hosts your open house, buyers see others are interested in your house, too. This competition can lead to stronger offers. An open house is also easier for you since you only need to leave once for many buyers to visit. Plus, your agent may get useful feedback on what people like or don’t like, which can help you make improvements to attract more buyers later, if needed.

- Showcasing on Your Agent’s Website – Having your house visible on your agent’s website allows for a professional presentation of your property. Additionally, people visiting your agent’s website are more likely to be serious buyers who are ready to make a move.

- Social Networking – Your real estate agent works hard to have a wide-ranging social media presence. Marketing your house this way allows them to reach a large audience. It also makes it easy for people to share your listing with friends and loved ones who might be interested.

- Providing Virtual Tours – Virtual tours are extremely convenient for buyers, especially those who are relocating from out of town. This method allows them to tour anytime, day or night. It shows your agent is using the latest technology to market your house.

There are many tools that can be used to market your house. As NerdWallet sums up:

“A good real estate agent will have a robust plan to promote your listing in an effort to find the right pool of buyers. Adding your home to databases of available homes called multiple listing services (MLS), open houses, 3D virtual tours, professional photography and broker tours for buyers’ agents (particularly for luxury homes) are all factors that may go into a marketing plan.”

As a seller, it’s smart to work with a creative local real estate agent who can maximize them to make sure you get as many eyes on your house as possible.

Bottom Line

When it comes to marketing your house, working with a local real estate agent has tons of benefits. If you’re ready to sell, but don’t know where to start, let’s chat.