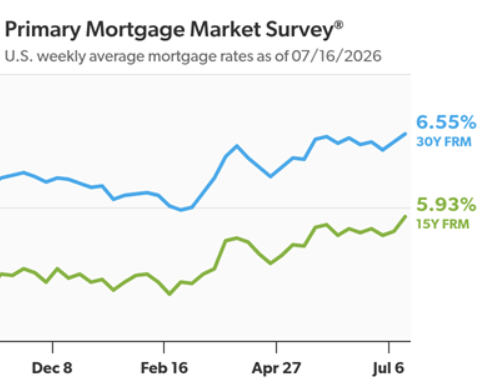

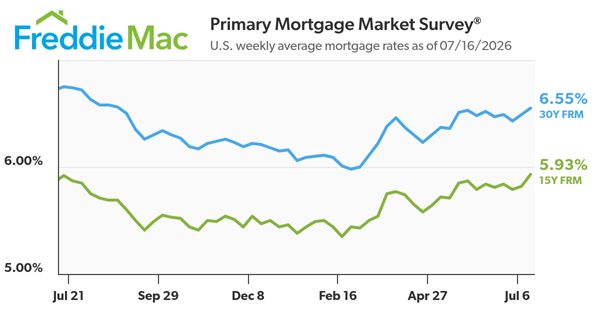

“The 30-year fixed-rate mortgage averaged 6.55% this week,” said Sam Khater, Freddie Mac’s Chief Economist. “Purchase application demand has weakened recently, but housing affordability is more favorable and housing inventory continues to rise, thus the backdrop for prospective homebuyers is modestly improving.”

The 30-year FRM averaged 6.55% as of July 16, 2026, up from last week when it averaged 6.49%. A year ago at this time, the 30-year FRM averaged 6.75%.

The 15-year FRM averaged 5.93%, up from last week when it averaged 5.82%. A year ago at this time, the 15-year FRM averaged 5.92%.

The PMMS® is focused on conventional, conforming, fully amortizing home purchase loans for borrowers who put 20% down and have excellent credit.

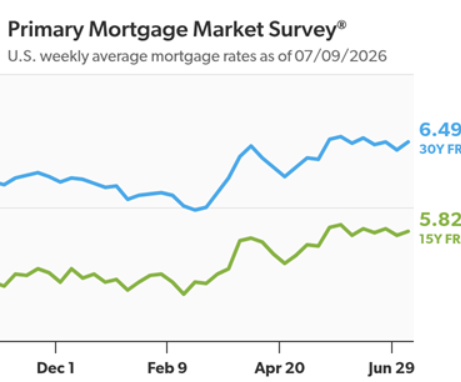

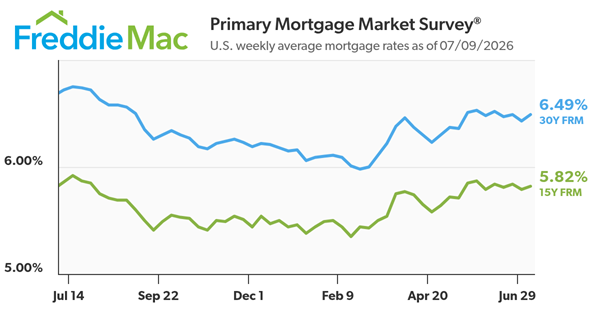

“The 30-year fixed-rate mortgage averaged 6.49% this week,” said Sam Khater, Freddie Mac’s Chief Economist. “Mortgage rates have not changed much recently, but economic growth and housing affordability continue to improve for homebuyers as they shop for homes in today’s market.”

The 30-year FRM averaged 6.49% as of July 9, 2026, up from last week when it averaged 6.43%. A year ago at this time, the 30-year FRM averaged 6.72%.

The 15-year FRM averaged 5.82%, up from last week when it averaged 5.79%. A year ago at this time, the 15-year FRM averaged 5.86%.

The PMMS® is focused on conventional, conforming, fully amortizing home purchase loans for borrowers who put 20% down and have excellent credit.

What To Expect from the Housing Market in the Second Half of 2026

If the first half of this year has left you feeling stuck, you’re not the only one. Mortgage rates stayed higher than people wanted. Affordability remained tight. And uncertainty overseas added another layer of pressure nobody saw coming.

That’s why so many people are asking the same question: Will the second half of the year be any better for the housing market?

While nobody has a crystal ball, there are a few encouraging signs things could start moving in a better direction. Here’s what to watch.

Mortgage Rates Could Be Near a Turning Point

One of the biggest reasons mortgage rates haven’t come down yet is inflation. And higher energy prices and uncertainty overseas are at least part of the reason inflation is still elevated. The encouraging news?

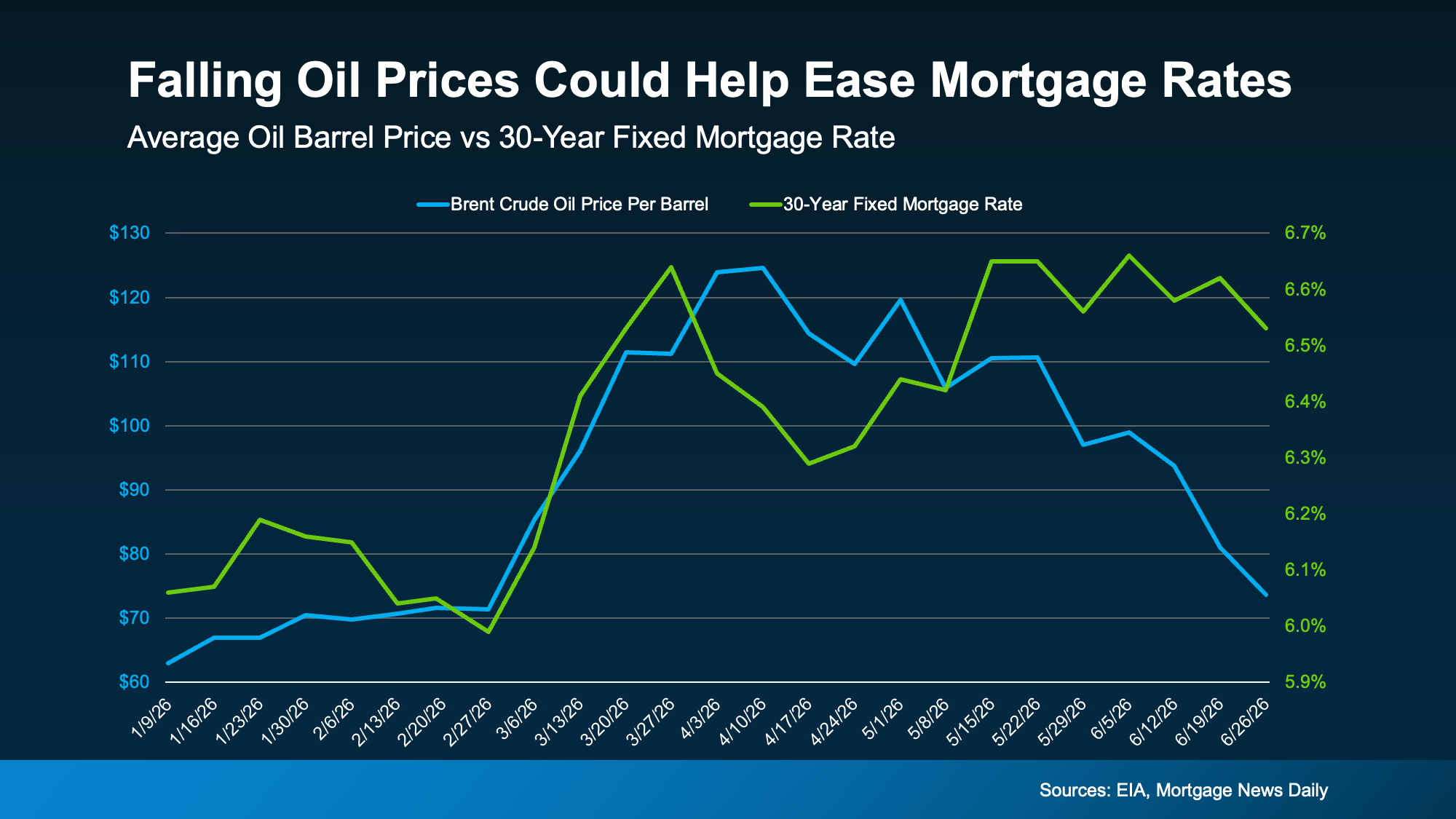

Oil prices have already started coming back down.

That may not sound like it has much to do with buying a home. But historically, mortgage rates and oil prices tend to move in the same direction.

Take a look at the graph below. Generally, they rise and fall together. Both went up in February when the conflict began. While there’s been some volatility lately, experts at the U.S. Energy Information Administration (EIA) say oil prices are forecast to come down. And since oil prices have been on an overall downward trend lately, mortgage rates could come down too:

It’s too soon to say exactly when that will happen (or by how much they’ll fall), but if energy prices go down, inflation cools off, and tensions overseas ease, mortgage rates could come down in the second half of the year.

And that’s good news for anyone thinking about moving. The first half of the year tested everyone’s patience. The second half may finally reward it.

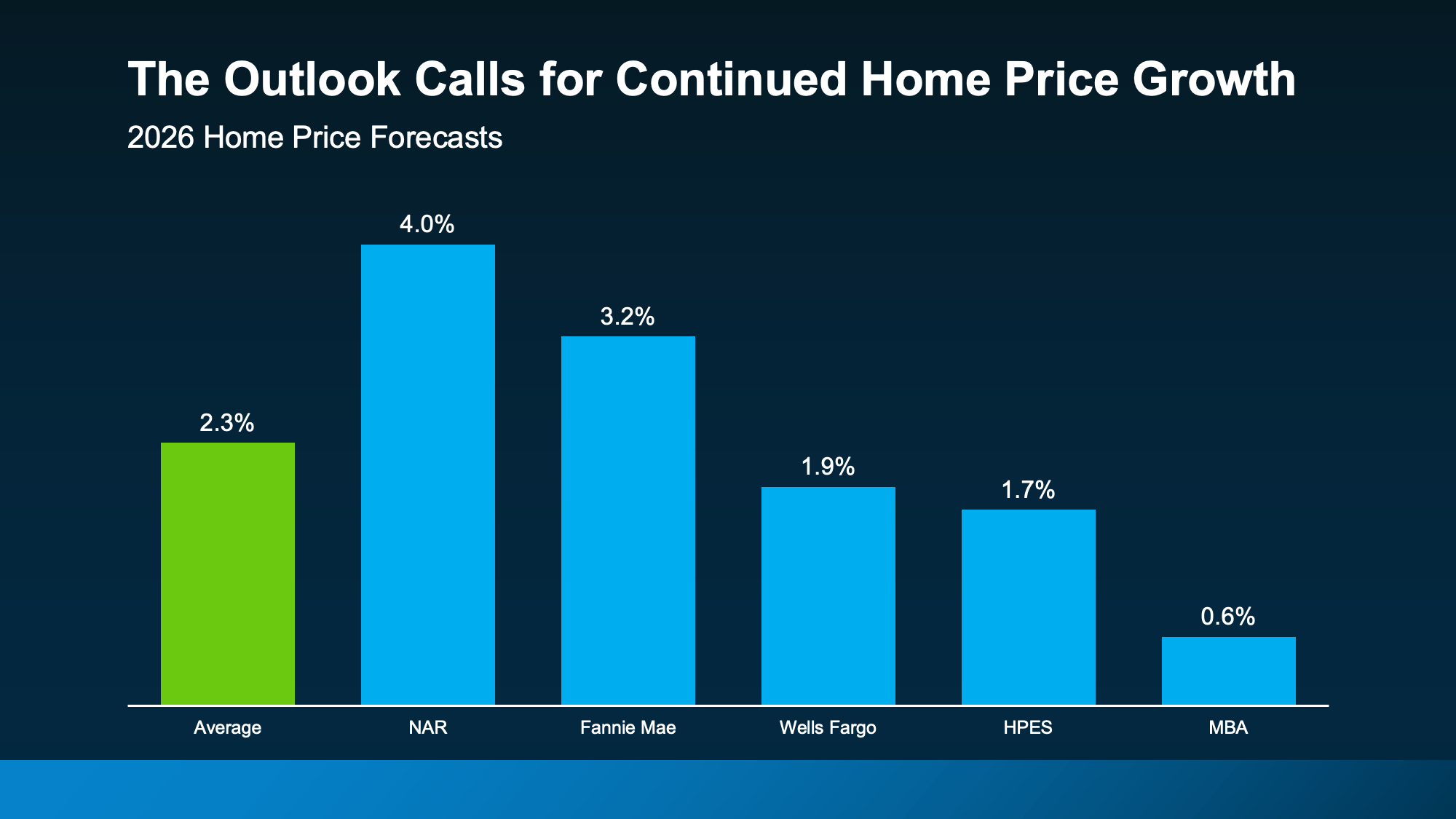

Home Prices Could Pick Back Up

A lot of people want home prices to fall too. But that’s not what most forecasts show.

While price trends are going to vary by area, and some places are seeing mild declines, experts still expect home prices to net positive this year at the national level.

In fact, they’re projecting prices will rise by an average of 2.3% in 2026 (see graph below):

What does that mean for you? Right now, Federal Housing Finance Agency (FHFA)data shows prices are up about 1.7% nationally year-over-year. The average forecast for all of 2026? 2.3%.

Based on those projections, home price growth would have to pick up a bit during the second half of the year. Nothing dramatic, just enough to finish the year around that projected 2.3% gain.

Here’s why that’s possible.

The number of homes for sale has grown, but that growth may be starting to slow down. And if rates improve, more buyers could jump back into the market. More buyers competing could put modest upward pressure on prices, especially if inventory’s not growing as fast.

That’s why buyers shouldn’t assume waiting will guarantee a lower price later. And for sellers, that’s great news if you’ve been worried about your home’s value.

More Homes Are Expected To Sell

If you’ve been wondering why the housing market has felt quieter lately, you’re not imagining it. Home sales have been slower than many experts expected. But that doesn’t mean people have stopped wanting to move.

A lot of people still want or need to make a change. They’ve just been waiting for more certainty, better affordability, or a clearer read on where the market is headed. And early signs show that may be on the horizon.

If rates ease and confidence improves, more people may finally move. As Odeta Kushi, Deputy Chief Economist at First American, explains:

“Overall, we expect pent-up demand to continue emerging gradually. But the pace of recovery will vary significantly across markets and will depend on the path of rates, labor market conditions and inventory growth.”

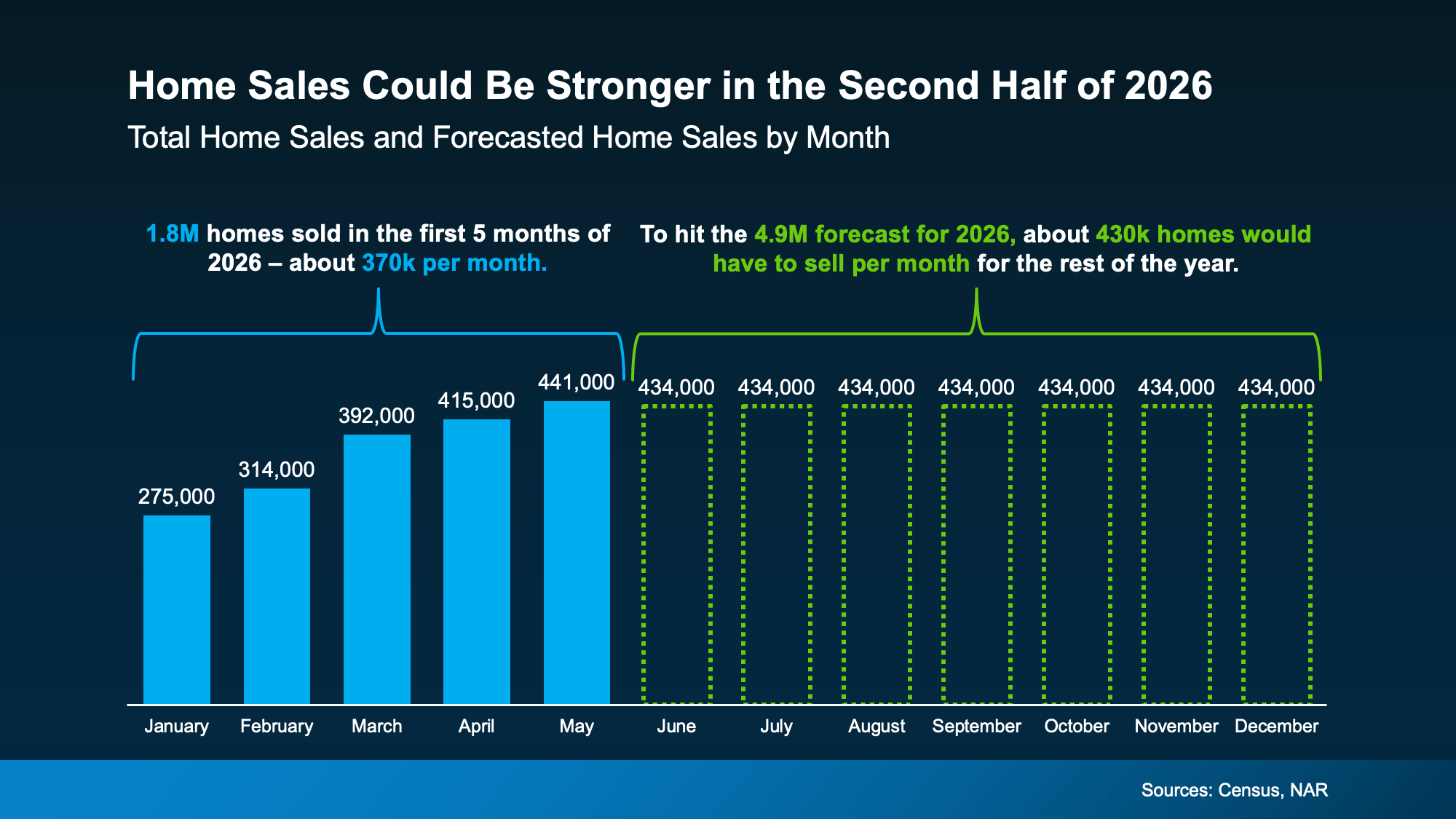

Based on the latest forecasts, to hit the number of sales expected this year, here’s what would have to happen. The second half of the year would need to outperform the first in sales (see graph below):

In fact, each month for the rest of 2026 would have to come close to matching the best month we’ve had so far this year (May). That’s a sign the experts are calling for more momentum headed into the second half.

More people will finally make their move happen – and you’ve got the chance to be one of them.

Bottom Line

The second half of the year probably won’t be perfect. But it could be better.

Mortgage rates may ease. Home sales could pick up. And prices are expected to continue rising at a healthier, more sustainable pace. If you’ve been waiting for signs of progress, this is it.

If you want to understand what these forecasts mean for your plans and what’s happening in our local market, let’s connect.

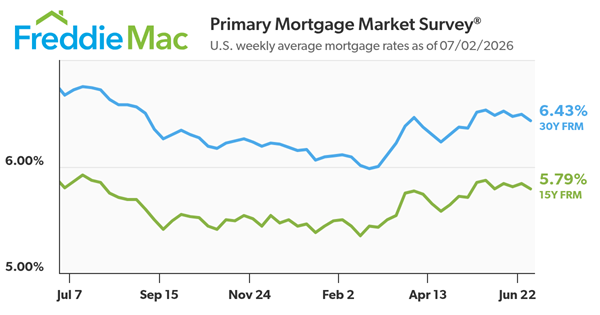

“The 30-year fixed-rate mortgage eased slightly this week averaging 6.43%” said Sam Khater, Freddie Mac’s Chief Economist. “With rates at a seven-week low and purchase demand continuing to edge higher, it’s an encouraging sign as prospective homebuyers respond to modest improvements in affordability.”

The 30-year FRM averaged 6.43% as of July 2, 2026, down from last week when it averaged 6.49%. A year ago at this time, the 30-year FRM averaged 6.67%.

The 15-year FRM averaged 5.79%, down from last week when it averaged 5.84%. A year ago at this time, the 15-year FRM averaged 5.80%.

The PMMS® is focused on conventional, conforming, fully amortizing home purchase loans for borrowers who put 20% down and have excellent credit.

When your house doesn’t sell, it’s not just disappointing. It messes with your timing. Your plans. Your confidence. You start second-guessing everything, including the decision to move in the first place. And that raises 2 big questions:

Do you try again?

Is that even worth it?

Here’s the secret to getting a better outcome the second time around.

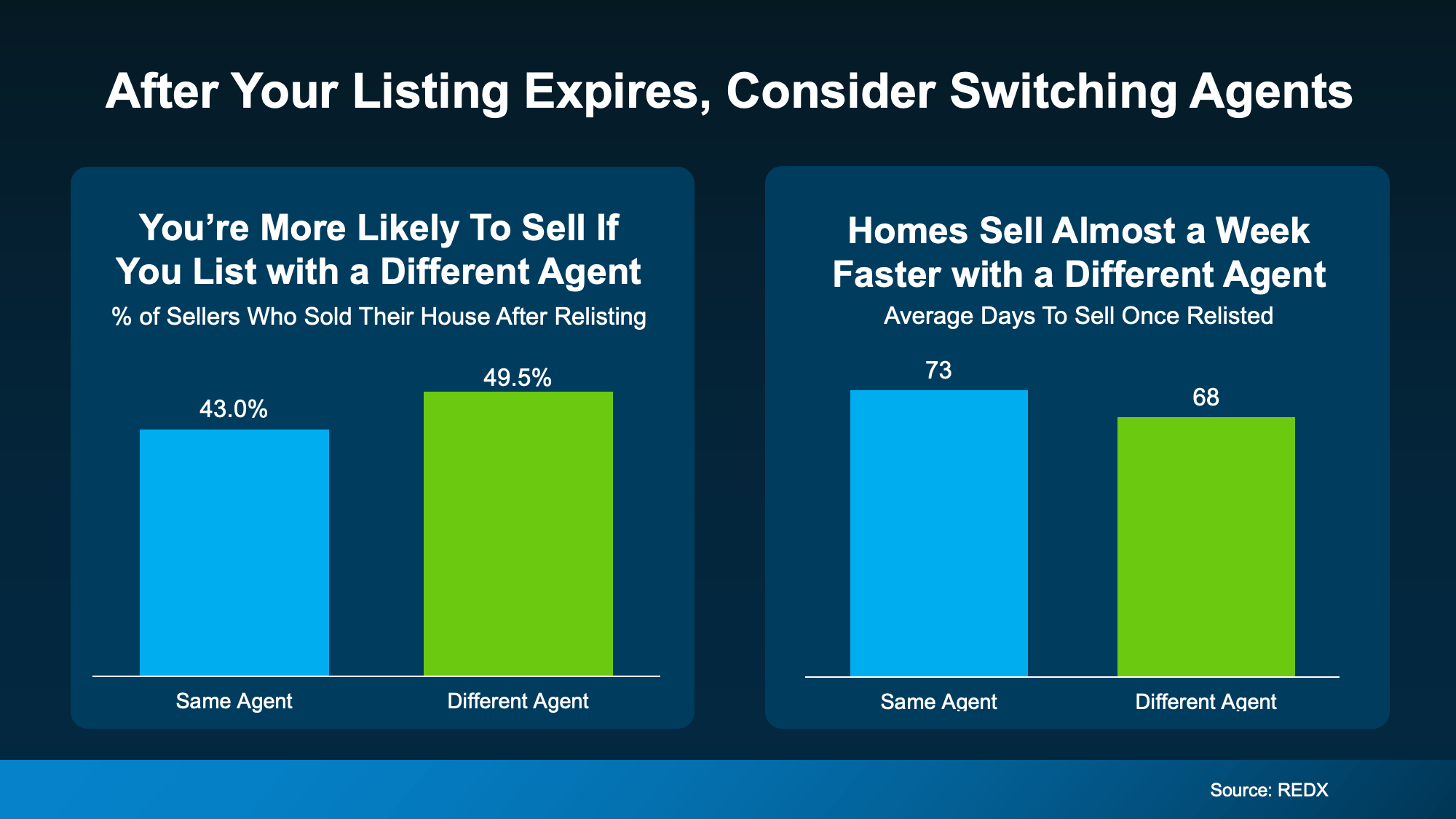

Different Agent. Different Results.

Most sellers who re-list and ultimately sell don’t wait for market to magically change. They change their approach. And there’s data to back that up.

Research from REDX shows homeowners who put their house back on the market with a different agent are more likely to sell than homeowners who re-used the same agent. Not to mention, they see their homes sell faster (see graph below):

That’s the power of a fresh set of eyes. Because in a moment like this, the worst thing you can do is rerun the same set of plays and expect a different outcome. A different agent can bring a new perspective on where things went off track – and a lot of the time, one of these things happened.

1. The Asking Price Didn’t Match Buyer Reality

There’s a saying that’s especially important in today’s market, and it’s: “if your price isn’t compelling, it’s not selling.” Maybe that’s what happened with your house.

With mortgage rates where they are and inflation driving up the cost of everyday purchases, buyers have less room to stretch. If they feel like your house is priced even a little high, it’s going to get skipped over. And if no one looks at it, it’s not going to sell.

The Fix: Price to draw buyers in, not push them away. Have an agent pull fresh data from recent sales so your asking price matches what buyers are actually paying right now.

2. The First Impression Didn’t Win the Click

Most buyers decide whether they want to tour a home in seconds. If the photos look dark, or dated, they scroll right past. And while you may think: “If they just saw it in person, they’d get it,” you may not get that chance.

And honestly, even in person, small things can quietly kill momentum – worn down paint, outdated fixtures, clutter, or a yard that feels high-maintenance. Individually, they’re small. Stacked together, they create doubt.

The Fix: Walk the house like you’re a buyer, not the owner. Start with what’s easy and obvious – paint, lighting, curb appeal, decluttering. Then update the photos so they match the best version of your house.

3. The Marketing Was Too “Set It and Forget It”

Today, the number of homes for sale has grown in many areas. Buyers have more options, which means your house needs a plan to stand out. A generic description and a basic upload to the MLS can blend in fast.

The Fix: Find an agent who can build stronger exposure through digital marketing and social platforms, plus content that makes buyers stop – strong photos, a smart description, a video walk-through, and a plan for open houses and follow-up.

4. There Was No Clear Plan for Feedback

Sometimes the house gets showings, but no offers. If that was your experience, it actually tells you something important. Buyers liked it enough online to come see it. So, something else was holding them back.

Those buyers were sending a message. It just wasn’t translated into action.

The Fix: Make sure your agent has a clear plan for seeking out and acting on feedback quickly. That dialogue often points to the one change that would get a house sold.

5. The Deal Couldn’t Get Over the Finish Line

Even when a house is priced well and marketed right, deals fall apart when there’s no plan for the human side of the transaction.

Buyers today are more likely to ask for repairs, credits, or help with closing costs than a few years ago. In this type of market, being unwilling to negotiate can cost you more than a reasonable concession ever would.

The Fix: Decide ahead of time what matters most to you and where you can be flexible. Keep the dialogue open and lean on your agent for advice.

Bottom Line

If your house didn’t sell the first time, you’re not stuck. You just need a different strategy, and maybe a different partner.

When you’re ready for a fresh set of eyes on what happened and what to change first, let’s connect.

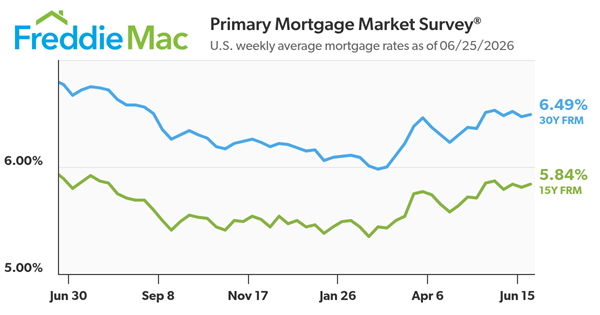

“The average 30-year fixed mortgage rate was little changed this week at 6.49%” said Sam Khater, Freddie Mac’s Chief Economist. “Rates have remained relatively stable over the last six weeks. Meanwhile, purchase activity eased modestly and refinance activity has continued to pick up recently, reflecting borrowers’ responsiveness to current rate levels.”

The 30-year FRM averaged 6.49% as of June 25, 2026, up from last week when it averaged 6.47%. A year ago at this time, the 30-year FRM averaged 6.77%.

The 15-year FRM averaged 5.84%, up from last week when it averaged 5.81%. A year ago at this time, the 15-year FRM averaged 5.89%.

The PMMS® is focused on conventional, conforming, fully amortizing home purchase loans for borrowers who put 20% down and have excellent credit.

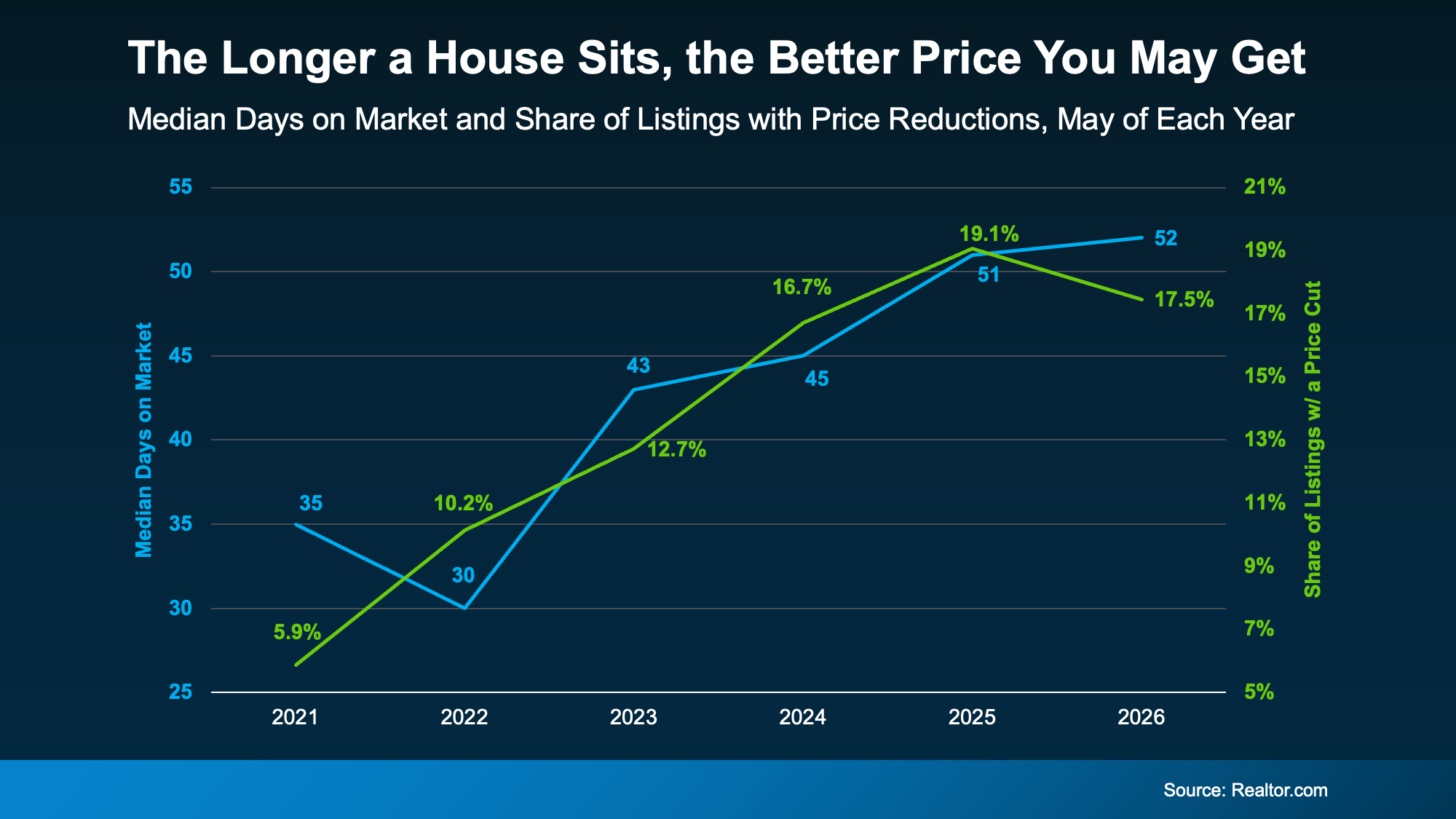

Open up a home search and you’ll see them. Listings that have been on the market for two months. Three. Some longer.

Most buyers scroll right past them, assuming something’s wrong with the house. But that instinct could be costing you, since the longer a home sits, the more motivated the seller usually gets.

Where Some Buyers Are Finding Better Deals

If affordability has been your #1 hurdle to buying, here’s a surprisingly simple strategy that could help you finally get your foot in the door. Start with the homes that have been sitting the longest. That’s often where the best deals are.

Here’s why. Data from Realtor.com shows there’s a connection between longer time on the market and lower sales prices. Basically, the longer a house sits, the more likely it is that the seller will reduce the price (see graph below):

The blue line tracks how long homes stay on the market, while the green line tracks the share of homes getting a price reduction. As one climbs, so does the other.

And if you focus on these homes that are just sitting and waiting, the opportunity for you is bigger than you may think right now.

Redfin data shows there’s $347 billion worth of stale listings on the market right now – more than ever before for this time of year. So, ask your agent to filter listings for you from oldest to newest. The home that fits your budget might already be there. Just further down the list than you thought.

Lingering Doesn’t Always Mean Something’s Wrong

Let’s say you do that and something catches your eye. Still, you might be questioning why the home has been sitting in the first place. Just remember, sometimes it has nothing to do with the home itself.

According to Redfin, common causes are:

The asking price was set too high to start

The home didn’t show well online

There are a lot of homes for sale in the area, so it just got buried

So, nothing that’s necessarily a dealbreaker, or even anything that’s wrong with the home itself. If there’s a real issue, a thorough inspection will surface it. And that’s information you can use to negotiate. Not a reason to assume it’s a house worth skipping over.

How To Turn a Lingering Listing into a Win

So how do you capitalize on a lingering listing? According to USA Today, you have two main levers to pull.

The first is price. Work with your agent to study what comparable homes recently sold for, then build an offer around that. Coming in below asking price is fair game when a home has been sitting.

The second is concessions. If a seller won’t budge much on price, they may still help in other ways, like covering some closing costs, repair credits, or even a mortgage rate buydown that lowers your monthly payment.

A local agent has the context to tell which homes are the real opportunities and which are skippable.

Bottom Line

A house sitting on the market isn’t always a glaring red flag. In today’s market, it may be your best opportunity yet.

For help deciding which lingering listings are actually worth a second look, let’s connect.

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link