Selling a house comes with a lot of moving pieces, and the last thing you want is a deal falling apart over unexpected repairs uncovered during the buyer’s inspection. That’s why it pays to anticipate potential issues before buyers ever step through the door. And one way to do that is with a pre-listing inspection.

What Is a Pre-Listing Inspection?

A pre-listing inspection is essentially a professional home inspection you schedule before putting your house on the market. Just like the inspections your buyer will do after making an offer, this process identifies any issues with the condition of your house that could have an impact on the sale – like structural problems, faulty or outdated HVAC systems, or other essential repairs.

While it’s a great option if you’re someone who really doesn’t like surprises, Bankrate explains this may not make sense for all sellers:

“While it can be beneficial for a seller to do, a pre-listing inspection isn’t always necessary. For example, if your home is relatively new and you’ve been the only owner, you’re most likely already aware of any big issues that could impact a sale. But for an older home, a pre-listing inspection can be very insightful and help you get ahead of any potential problems.”

The key is deciding whether the benefits outweigh the costs for your situation. Sometimes a few hundred dollars now can get you information that’ll save you a lot of time and hassle later on.

Why It May Be Worth Considering in Today’s Market

Right now, buyers are more cautious about how much money they’re spending. And they want to be sure the home they’re buying is worth the expense. In a market like this, a pre-listing inspection can be your secret weapon to make sure your house shows well. Here are just a few ways it can help:

Gives You Time To Make Repairs: When you know about issues ahead of time, it gives you the chance to fix them on your schedule, rather than rushing to make repairs when you’re under contract.

Avoid Surprises During Negotiations: When buyers discover issues during their own inspection, it can lead to last-minute negotiations, price reductions, or even a deal falling through. A pre-listing inspection gives you a chance to spot and address any problems ahead of time, so they don’t turn into last-minute headaches or negotiation roadblocks.

Sell Your House Faster: According to Rocket Mortgage, if your house is listed in the best shape possible, there won’t be as many reasons for buyers to ask for concessions. That means you should be able to cut down on negotiation timelines and ultimately sell faster.

How Your Agent Will Help

But before you think about reaching out to any inspectors to get something scheduled, be sure to talk to an agent. Your agent will be able to give you advice on whether a pre-inspection is worthwhile for your house and the local market. Because it may not be as important if sellers still have the majority of the negotiation power where you live.

If your agent does recommend moving forward and getting one done, here’s how they’ll support you throughout the process.

Offer Advice on How To Prioritize Repairs: If the inspection uncovers problems, your agent will sit down with you and offer perspective on what’s going to be a sticking point for buyers so you know what to prioritize.

Knowledge of How To Handle Any Disclosure Requirements: After talking to your agent, you may decide not all of the repairs are worth it right now. Just be ready to disclose what you’re not tackling. Some states require disclosures as a part of a listing – lean on your agent for more information.

Bottom Line

While they’re definitely not required, pre-listing inspections can be especially helpful in today’s market. By understanding your home’s condition ahead of time, you can take control of the process and make informed decisions about what to fix before you list and what to disclose.

If you choose to skip this step, you may be just as surprised as your buyer by what pops up in their inspection. And that could leave you scrambling. Would you rather fix issues now or risk trying to save the deal later?

Let’s connect so you can see if this is a step that makes sense in our market.

More people are taking steps to buy a home. And, if you’ve been waiting for the right time to move, this may be the sign you’ve been looking for.

For the past few years, a lot of would-be homebuyers hit pause on their plans. With rising mortgage rates and affordability challenges, buying just didn’t seem doable. But now, more of them are getting back out there. That’s because they’re getting used to the fact that this may be the new normal for the market – especially as forecasts show mortgage rates may be starting to stabilize. According to the National Association of Realtors (NAR):

“Home buyers seem to be getting over the shock of mortgage rates in the mid- to upper-6% range.”

And that’s good for you and your plans to sell. While there isn’t going to be a big rush of buyers flooding the market all at once, this does mean motivated buyers are re-starting their searches. And here’s the data to prove it.

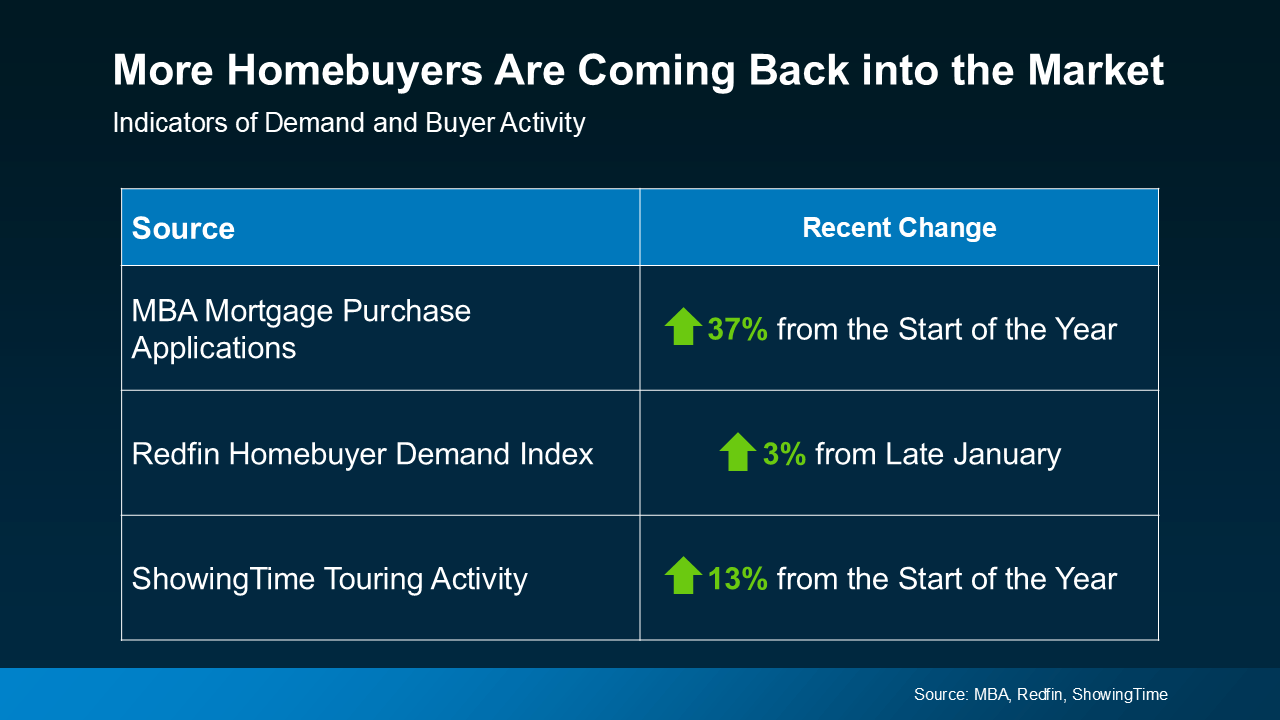

3 Signs Buyers Are Ready To Make Their Move

1. Mortgage Applications Are on the Rise: According to the Mortgage Bankers Association (MBA), mortgage applications are up 37% since the start of the year. That’s a big jump and a clear sign more buyers are more active lately. Don’t miss out on that. Serious buyers who are getting their finances in order are great potential buyers for your house.

2. Buyer Demand Is Picking Up: The Homebuyer Demand Index from Redfin shows demand is up 3% since late January. While that’s not a huge spike, momentum is building.

3. More Home Showings:ShowingTimedata says home showings are up 13% since the beginning of the year. This added foot traffic is exactly what you want to see if you’re about to sell your house. It signals more serious interest in buying. More buyers out there looking means more potential eyes on your house. And more eyes could translate to more offers.

And chances are, this activity is only going to pick up from here. We’re headed into the busiest season of the year for housing. Spring is when more people choose to buy or sell than any other time of year. So, now is a great time to list and get in on the action.

Bottom Line

As buyers re-enter the market, you have the chance to do the same thing. And the increase in buyer activity is definitely something you’ll want to take advantage of. To make sure your house gets in front of these motivated buyers, let’s connect.

If the right buyer walked through your door tomorrow, would you be ready to sell?

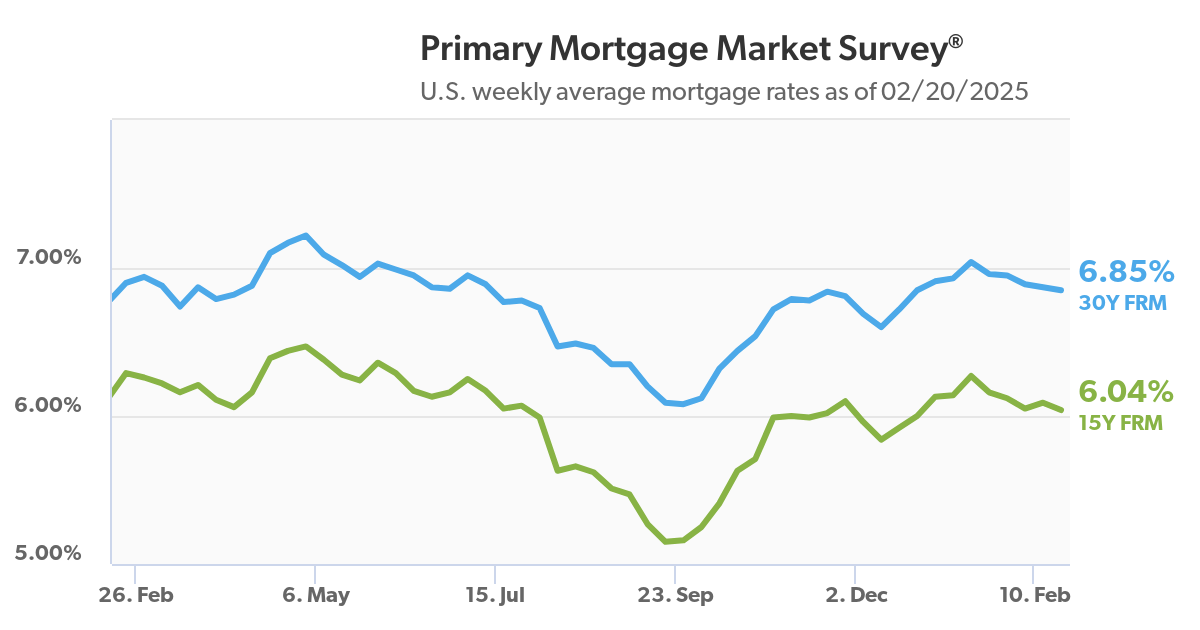

“Mortgage rates decreased slightly this week,” said Sam Khater, Freddie Mac’s Chief Economist. “The 30-year fixed-rate mortgage has stayed just under 7% for five consecutive weeks and in that time has fluctuated less than 20 basis points. This stability continues to bode well for potential buyers and sellers as we approach the spring homebuying season.”

The 30-year FRM averaged 6.85% as of February 20, 2025, down from last week when it averaged 6.87%. A year ago at this time, the 30-year FRM averaged 6.90%.

The 15-year FRM averaged 6.04%, down from last week when it averaged 6.09%. A year ago at this time, the 15-year FRM averaged 6.29%.

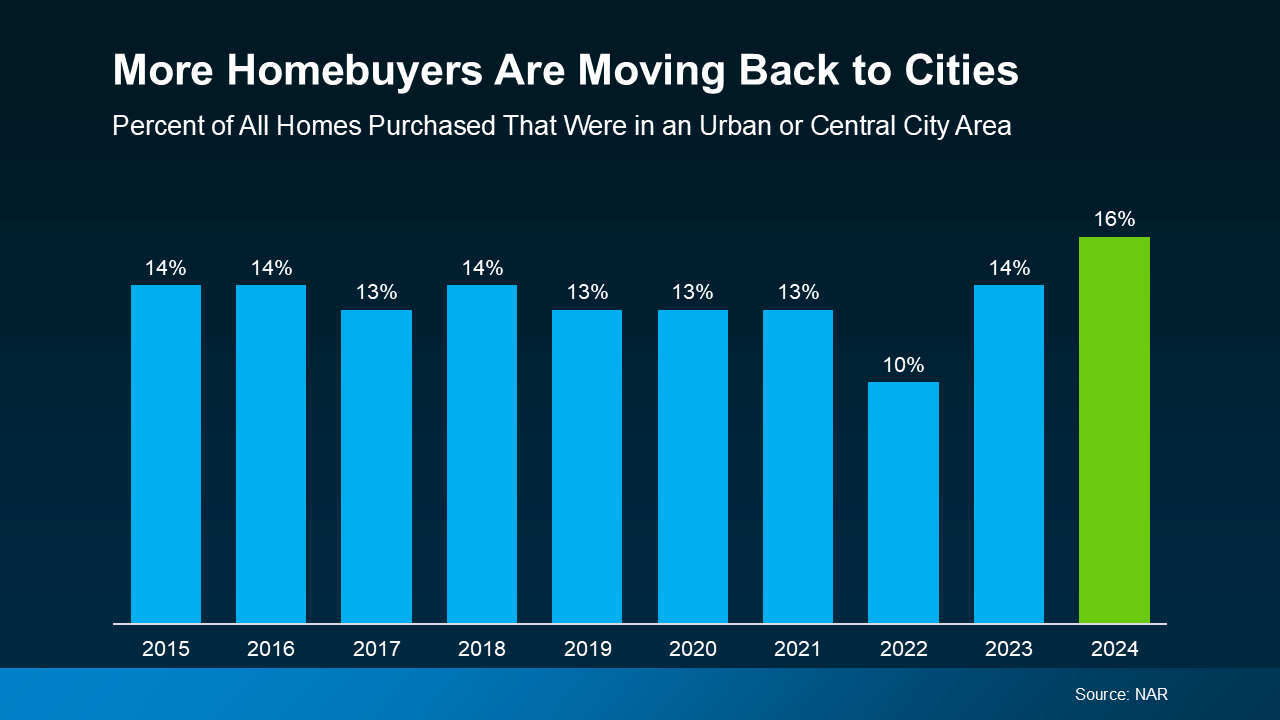

After years of suburban and rural migration during the pandemic, cities have been making a comeback in the past couple of years. According to the National Association of Realtors (NAR), the percentage of people moving to cities has risen to 16%. While that may not sound like a big number to you, it is the highest level in a decade – and that’s a big deal (see graph below):

And data from BrightMLS seems to confirm this trend. In a recent survey, 1 in 5 (20.6%) people looking to buy say they want to live in the city.

So, what’s behind this ongoing shift back to urban living? Let’s break down the top three reasons why people are trading quiet suburbs for bustling cityscapes. You may find out you want to sell your house with a big yard and move to an urban oasis, too.

1. Vibrant Culture

Cities have always been hubs of culture, entertainment, and community. They’re packed with energy and there are always endless things to do. During the pandemic, a lot of that excitement was put on pause. But the last couple of years? Cities are buzzing again.

There’s nothing quite like being able to walk to your favorite coffee shop, pop into a local gallery, see a live concert or show, or grab a last-minute dinner at a great spot down the street. It’s a lifestyle that’s easy to love — and one a lot of people want today.

2. Being Close to Work

Remote work is still a thing, but most companies are moving to hybrid schedules or even bringing employees back to the office. That makes living closer to work way more convenient. Whether it’s cutting down a long commute or having more chances to network in person, being close to the office is a big plus — especially for industries that thrive on face-to-face connections.

3. Easy Access To Everything You Need or Want

One of the best things about living in a city? The convenience. Public transportation, top-notch healthcare, and so much more are all within easy reach. For a lot of people, having everything nearby just makes life easier — and it’s a big reason they’re drawn to urban living.

What To Do If You Want To Move To the City

Let’s say you moved to a suburban area during the pandemic and you’re missing the excitement of living right off city streets. You’re probably thinking: how can I afford to move back into the heart of things with how mortgage rates and home prices are? Here’s how other people are doing it.

According to data from the Federal Housing Finance Agency (FHFA), home values have gone up by 57.4% in the last 5 years alone. And that means your house is probably going to sell for more than you bought it for.

If you already own a home in the suburbs, you may be able to sell that house and use the equity you get back to fuel your move. Sure, you may have to compromise and be happy with a smaller, urban space – but if it’s the lifestyle you’re craving – that trade-off is going to be worth it. To find out what’s possible and what it costs to live in an urban area, lean on a local real estate professional.

Bottom Line

The urban renaissance is real. Whether it’s the vibrant culture, being close to work, or having easy access to everything you need, cities are once again calling — and people are answering.

What’s your favorite thing about life in the city? Let me know.

I’d love to find you a home you love where all the hustle and bustle makes life a bit more exciting.

It feels like everything is getting more expensive these days. That’s because inflation has remained higher than normal for longer than expected – and that’s impacting the costs of goods, services, and more. And with rising costs all around you, you’re probably questioning: is now really the right time to buy a home?

Here’s the good news. Owning a home is actually one of the best ways to protect yourself from the rising costs that come with inflation.

A Fixed Mortgage Protects You from Rising Housing Costs

One of the key benefits of homeownership is that when you buy a home with a fixed-rate mortgage, your biggest monthly expense — your mortgage payment — stabilizes. Sure, your payment could rise slightly as your homeowner’s insurance and property taxes shift. But no matter what happens with inflation, your principal and interest payments won’t change.

That’s not the case if you rent. Rent tends to rise over time, and it usually goes up even faster than the rate of inflation. Just look at the data from theBureau of Economic Analysis (BEA) and the Census Bureau (see graph below):

So, while renters face higher costs year after year, homeowners with a fixed mortgage rate lock in their monthly payments, making it easier to budget no matter what happens with inflation.

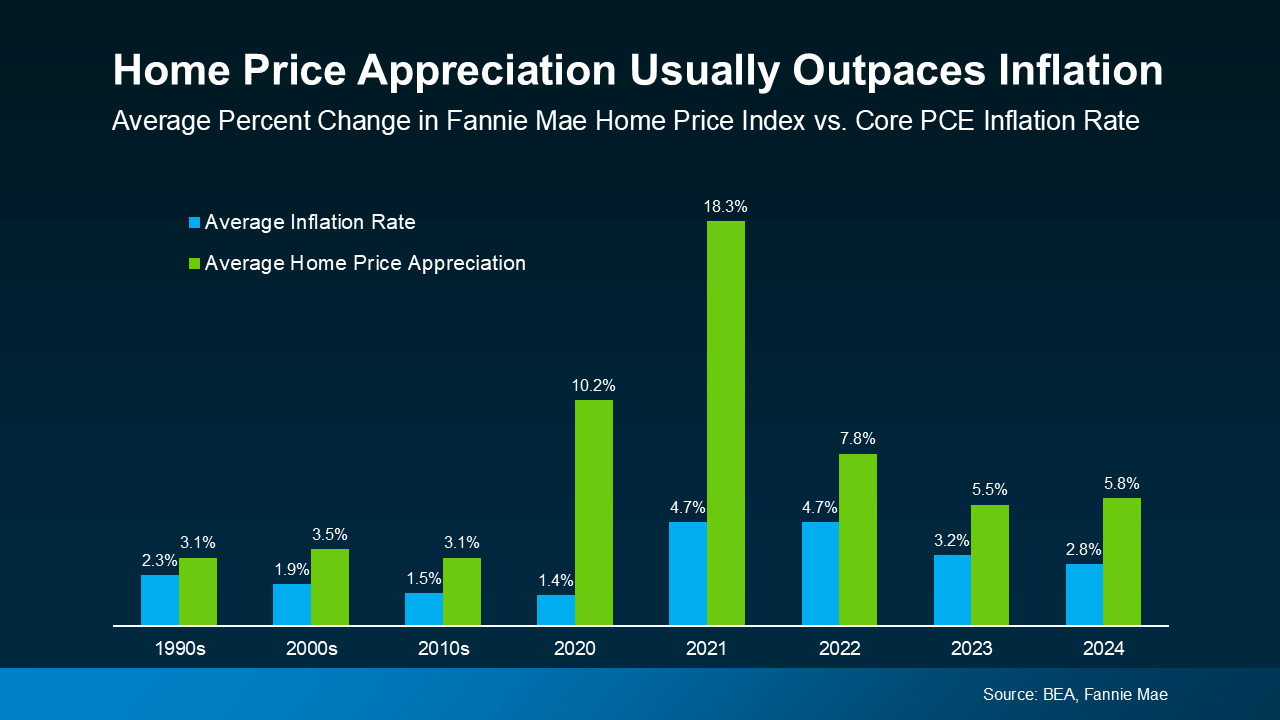

Home Prices Typically Rise Faster Than Inflation

Another big reason homeownership is a great hedge against inflation is that home values tend to appreciate over time — often at a higher rate than inflation, according to data from the BEA and Fannie Mae(see graph below):

That makes real estate one of the strongest long-term investments during times of rising prices. While inflation can chip away at the value of cash savings, real estate typically holds or grows in value, allowing you to build wealth.

On the other hand, renting offers no protection against inflation. In fact, it does the opposite — when inflation drives up costs, landlords often pass those increases onto tenants through higher rents.

That means as a renter, you’re continually paying more without gaining any financial benefit. But as a homeowner, rising prices work in your favor by increasing the value of your home and growing your equity over time.

And with experts forecasting continued home price growth, that means you’re making an investment that usually grows in value and should outperform inflation in the years ahead.

In short, a fixed-rate mortgage protects your budget, and home price appreciation grows your net worth. That’s why homeownership is a strong hedge against inflation.

Bottom Line

Inflation can make everyday expenses unpredictable, but owning a home gives you stability. Unlike rent, your monthly mortgage payment stays pretty much the same over time. Plus, the value of your home is likely to increase after you buy.

How would having a fixed housing payment change the way you budget for the future?

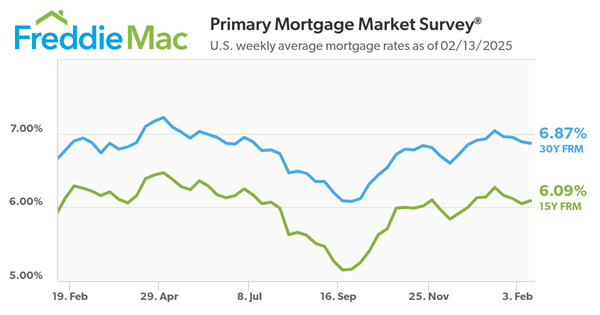

“The 30-year fixed-rate mortgage continued to inch down this week, reaching its lowest level thus far in 2025,” said Sam Khater, Freddie Mac’s Chief Economist. “Recent mortgage rate stability is benefitting potential buyers, as purchase demand is stronger than this time last year. This is an indication that a thaw in buyer activity could be on the horizon.”

The 30-year FRM averaged 6.87% as of February 13, 2025, down from last week when it averaged 6.89%. A year ago at this time, the 30-year FRM averaged 6.77%.

The 15-year FRM averaged 6.09%, up from last week when it averaged 6.05%. A year ago at this time, the 15-year FRM averaged 6.12%.

The PMMS® is focused on conventional, conforming, fully amortizing home purchase loans for borrowers who put 20% down and have excellent credit.

Here’s reaction from Dr. Jessica Lautz, Deputy Chief Economist and Vice President of Research at the National Association of REALTORS®.

Facts: The average 30-year fixed mortgage rate from Freddie Mac fell to 6.87% from 6.89% last week. At 6.87%, with a 20% down payment, the monthly mortgage payment is $2,101 for a home priced at $400,000. With 10% down, the typical payment would be $2,364.

Positive: Mortgage interest rates have decreased for four consecutive weeks. This timing is encouraging as home buyers begin to enter the early Spring housing market, and mortgage applications have also risen. If housing inventory continues to grow, home buyers will find themselves in a more favorable position compared to previous years.

Negative: Although rates are lower on a weekly basis, the overall housing affordability equation considers the price of the home alongside expenses such as utilities, taxes, and insurance.

-o-

For more information on daily mortgage rate movements, check with your loan office. Or you can find information online at sites such as Mortgage News Daily

Spring is the busiest season in the housing market. It’s the time of year when buyers are most active – that means it’s when homes sell faster and for top dollar. If you’ve already got a move on your mind, why not list this spring and take advantage of the added buyer demand?

Since spring is just around the corner, now’s the time to start getting your house market-ready. You’ve got just over a month to do the prep work. And while that may sound like a decent amount of time, it’s going to go by quickly. And you won’t want to rush through this important task – especially this year.

The Right Repairs Will Matter More This Spring

Right now, two things are true. There are more homes on the market than there have been in years. And buyers are being extra selective. That combination means you need to invest some time and effort in making strategic repairs. And many homeowners already have a jump on this work.

In the 2025 Outlook for Home Remodeling, Carlos Martin, Director of the Remodeling Futures Program at the Joint Center for Housing Studies of Harvard University, explains:

“. . . homeowners are slowly but surely expanding the pace and scope of projects compared to the last couple years.”

And the most common projects they’re tackling are replacing water heaters, HVAC units, and flooring. Energy efficiency is a key consideration too, based on home improvement data from the Census.

What To Prioritize as You Plan Ahead

But just because that’s what other homeowners are doing, it doesn’t mean that’s what you have to tackle. Think about what you’d want to see if you were a buyer. Focus on quick wins that are easy to knock out with the time you have – but, don’t ignore key repairs, especially ones you think could turn off buyers.

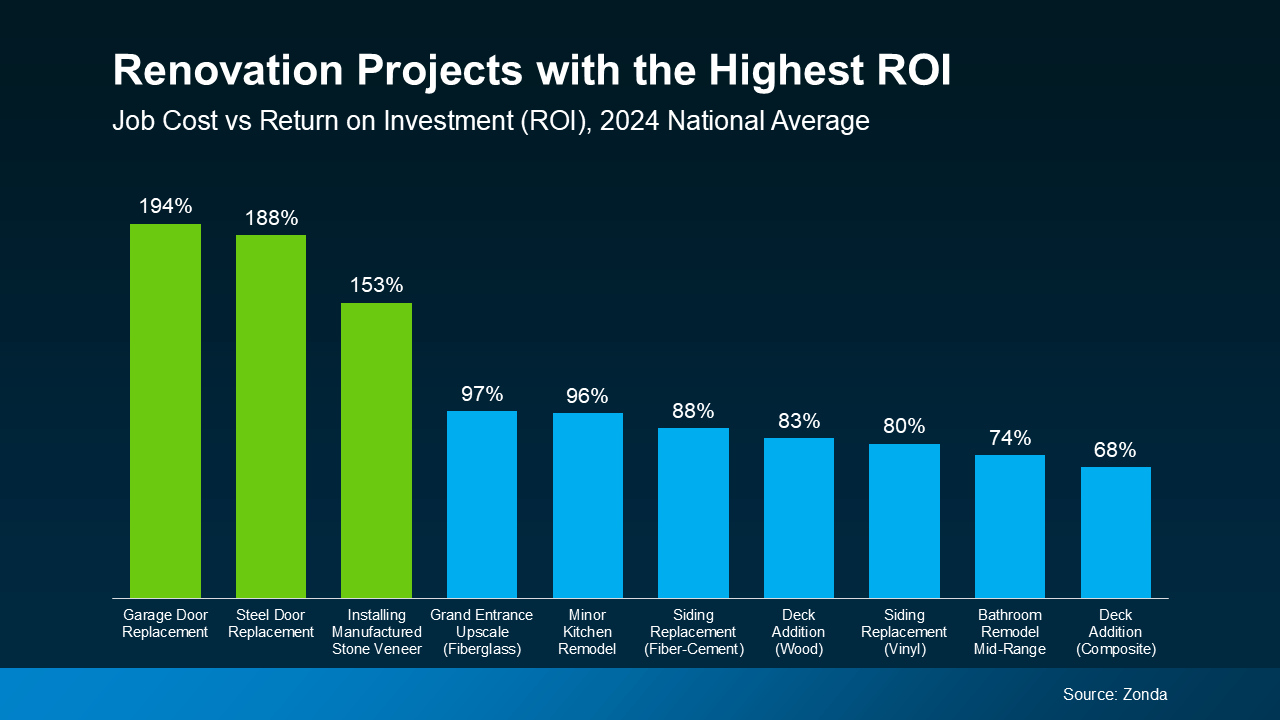

While big-ticket items like replacing an old roof or outdated flooring may seem daunting, they can pay off – especially if you focus on projects with the best return on investment (ROI).

An agent’s expertise is key in narrowing down your list to what’s actually worth it. They know what buyers in your area want and they also have data like this report from Zonda to guide you on which updates have the best ROI(see green in the graph below):

That’s why it’s so important to talk to a local real estate agent before you dive into any repairs. Bankrate puts it best:

“As a seller, it’s smart to be prepared and control whatever factors you’re able to. Things like hiring a great real estate agent and maximizing your home’s online appeal can translate into a smoother sale — and more money in the bank.”

It’s not too early to partner with an agent. By starting now, you’ve still got time to space out the work and find any contractors you need to get the job done. If you wait until spring to roll up your sleeves, you risk running out of time – and that means your house may be overshadowed by others who are more buyer-ready.

Bottom Line

If you’re planning to sell this spring, it’s time to start tackling your to-do list. But, before you get started, let’s connect. That way you can make sure you’re spending your time and budget on projects that’ll pay off in the long run.

Send me a list of what’s on your to-do list, and we can prioritize them together.

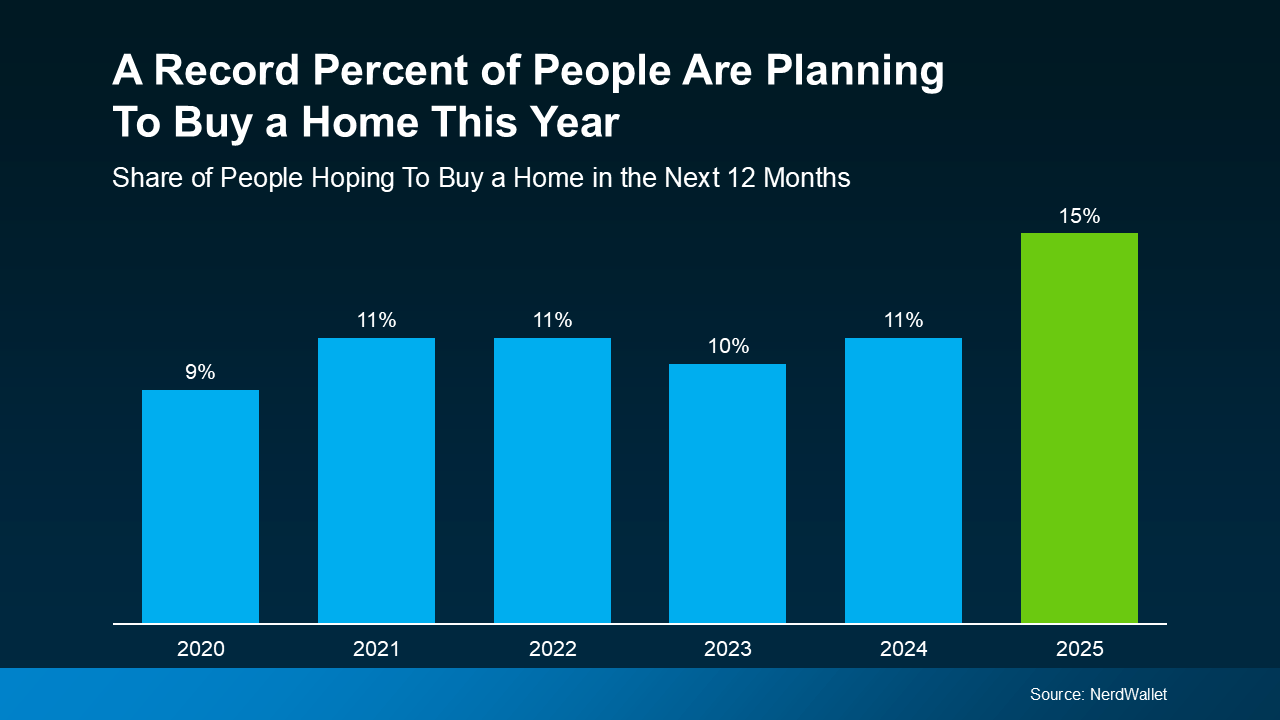

This could be the year to sell your house – and here’s why. According to a recent NerdWallet survey, 15% of people are planning to buy a home this year. That’s actually a record high for this survey (see graph below):

Here’s why this is such a big deal. The percentage has been hovering between 9-11% since 2020. This recent increase shows buyer demand hasn’t disappeared – if anything, it indicates there’s pent-up demand ready to come back to the market.

That doesn’t mean the floodgates are opening and that there’s going to be a huge wave of buyers like we saw a few years ago. But this does signal there’ll be more activity this year than last.

At least some of the buyers who put their plans on hold over the past few years will jump back in. Whether they’re feeling more confident about moving, they’ve finally saved up enough to buy, or they simply can’t wait any longer – this is the year they’re aiming to take the plunge.

And, according to that same NerdWallet survey, more than half (54%) of those potential buyers have already started looking at homes online.

That’s a good indicator that a number of these buyers will be looking during the peak homebuying season this spring. So, if you find the right agent to make sure your house is prepped, priced, and marketed well, you can get your house in front of them.

Bottom Line

More people are going to move this year, and with the right strategy, you can make sure your house is one of the first they look at.

What do you think these buyers will love most about your house?

Let’s talk it over and make sure it’s front and center in your listing.

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

And

And