Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

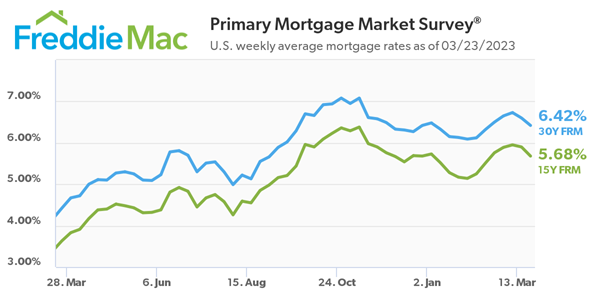

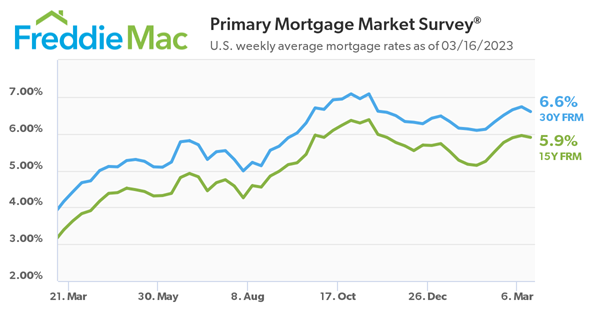

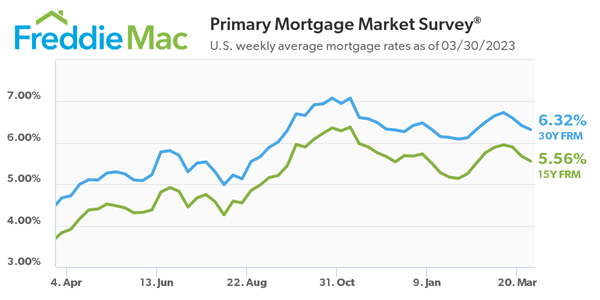

Freddie Mac today released the results of its Primary Mortgage Market Survey (PMMS) for the week ending March 30, 2023, showing the 30-year fixed-rate mortgage (FRM) averaged 6.32 percent.

“Economic uncertainty continues to bring mortgage rates down,” said Sam Khater, Freddie Mac’s Chief Economist. “Over the last several weeks, declining rates have brought borrowers back to the market but, as the spring homebuying season gets underway, low inventory remains a key challenge for prospective buyers.”

- 30-year fixed-rate mortgage averaged 6.32 percent as of March 30, 2023, down from last week when it averaged 6.42 percent. A year ago at this time, the 30-year FRM averaged 4.67 percent.

- 15-year fixed-rate mortgage averaged 5.56 percent, down from last week when it averaged 5.68 percent. A year ago at this time, the 15-year FRM averaged 3.83 percent.

The PMMS is focused on conventional, conforming, fully amortizing home purchase loans for borrowers who put 20 percent down and have excellent credit.