Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Mortgage Rates Increase Three Weeks In A Row

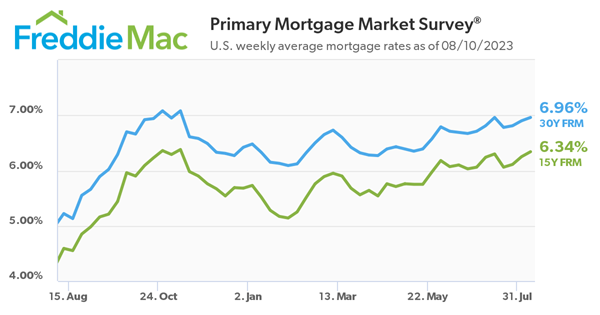

Freddie Mac (OTCQB: FMCC) today released the results of its Primary Mortgage Market Survey® (PMMS®), showing the 30-year fixed-rate mortgage (FRM) averaged 6.96 percent.

“For the third straight week, mortgage rates continued creeping up and are now just shy of seven percent,” said Sam Khater, Freddie Mac’s Chief Economist. “There is no doubt continued high rates will prolong affordability challenges longer than expected, particularly with home prices on the rise again. However, upward pressure on rates is the product of a resilient economy with low unemployment and strong wage growth, which historically has kept purchase demand solid.”

- 30-year fixed-rate mortgage averaged 6.96 percent as of August 10, 2023, up from last week when it averaged 6.90 percent. A year ago at this time, the 30-year FRM averaged 5.22 percent.

- 15-year fixed-rate mortgage averaged 6.34 percent, up from last week when it averaged 6.25 percent. A year ago at this time, the 15-year FRM averaged 4.59 percent.

The PMMS® is focused on conventional, conforming, fully amortizing home purchase loans for borrowers who put 20 percent down and have excellent credit.

Why Wait? Sell Your House Now!

About 11,000 Houses Will Sell Today

Some homeowners have been waiting for months to put their house on the market because they don’t think people are buying homes right now. If that’s you, know that even though the housing market has slowed compared to the frenzy of a couple of years ago, it isn’t at a standstill. Contrary to what you may believe, buyers are still active and plenty of homes are selling right now.

According to the National Association of Realtors (NAR), based on the pace of sales right now, just over 4 million homes will sell this year. With some simple math, let’s break down what that really means for you:

- 4.16 million homes divided by 365 days in a year = 11,397 houses sell each day

- 11,397 divided by 24 hours in a day = 475 houses sell per hour

- 475 divided by 60 minutes in an hour = about 8 houses sell each minute

So, on average, about 11,000 homes sell each day in this country.

A real estate expert can give you more information about how many houses are being sold in your neighborhood, the amazing advantages that sellers are experiencing right now, and the most important things buyers are searching for in your area. Together you’ll use this knowledge to shape how you market your house based on local trends.

Bottom Line

If you’ve been waiting to sell because you don’t think there are buyers out there, know today’s market is active. Every day you wait, around 11,000 other homeowners are selling. In the time it took you to read this, eight homes sold. When you’re ready to sell too, let’s connect.

Do I Need An Agent For New Construction?

Buying a new construction home can be an exciting experience. From being the very first owner, to customizing your home’s features, there are a lot of benefits. But navigating the complexities of buying a home that’s under construction can also be a bit overwhelming. This is where a skilled real estate agent can make all the difference.

An article from The Mortgage Reports sums it up like this:

“Your Realtor or real estate agent will be key to helping you navigate this process. . . . they can guide you through construction and help anticipate and solve for any possible snags along the way.”

Here’s how your agent is an invaluable resource in your search to find and buy your new home.

Agents Know the Local Area and Market

Your agent is well-versed in the emerging communities and upcoming developments that could influence your decision. For example, you’ll want to be aware if there were any plans to construct a highway through the woods behind your prospective backyard. It’s important to consider how the neighborhood and the surrounding area might evolve before making your home purchase. Your agent can help you find a community that perfectly aligns with your preferences, lifestyle, and future needs.

Knowledge of Construction Quality and Builder Reputation

An agent also has the expertise to evaluate the construction quality and reputation of different builders. Their knowledge and experiences with local builders allow them to offer insights into each one’s track record, customer satisfaction, and construction practices. This information can help you avoid any potential risks and help you confidently select a builder known for delivering quality homes.

Assistance with Customization and Upgrades

The most obvious benefit of opting for new home construction is the opportunity to customize your home to suit your preferences. Your agent will guide you through that process and share advice on the upgrades that are most likely to add long-term value to your home. Their expertise ensures you focus your budget on areas that will give you the greatest return on your investment later on.

Understanding Builder Contracts and Negotiations

Builder contracts can be complex and differ from traditional home purchase agreements. Your agent can help you navigate these contracts to make sure you fully understand the terms and conditions. They’re also skilled negotiators who can advocate on your behalf, potentially securing better deals, upgrades, or incentives for you throughout the process.

Bottom Line

The guidance and expertise of a local real estate agent can make all the difference in turning your vision of the perfect home into a reality. Let’s connect so you can feel confident about purchasing your new construction home.

Only Half the Inventory of a Normal Housing Market Today

Wondering if it still makes sense to sell your house right now? The short answer is, yes. Especially if you consider how few homes there are for sale today.

You may have heard inventory is low right now, but you may not fully realize just how low or why that’s a perk when you go to sell your house. This graph from Calculated Risk can help put that into perspective:

As the graph shows, while housing inventory did grow slightly week-over-week (shown in the blue bar), overall supply is still low (shown in the red bars). Compared to the same week last year, supply is down roughly 10% – and it was already considered low at that time. But, if you look further back, you’ll see inventory is down even more significantly.

As the graph shows, while housing inventory did grow slightly week-over-week (shown in the blue bar), overall supply is still low (shown in the red bars). Compared to the same week last year, supply is down roughly 10% – and it was already considered low at that time. But, if you look further back, you’ll see inventory is down even more significantly.

To gauge just how far off from normal today’s inventory is, let’s compare right now to 2019 (the last normal year in the market). When you compare the same week this year with the matching week in 2019, supply is about 50% lower. That means there are half the homes for sale now than there’d usually be.

The key takeaway? We’re still nowhere near what’s considered a balanced market. There’s plenty of demand for your house because there just aren’t enough homes to go around. As Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), explains:

“There are simply not enough homes for sale. The market can easily absorb a doubling of inventory.”

So, if you want to list your house, know that there’s only about half the inventory there’d usually be in a more normal year. That means your house will be in the spotlight if you sell now and you may see multiple offers and a fast home sale.

Bottom Line

With the number of homes for sale roughly half of what there’d usually be in a more normal year, you can rest assured there’s demand for your house. If you want to sell, let’s connect now so your house can shine above the rest while inventory is so low.

4 Ways You Can Use Your Home Equity

If you’re a homeowner, odds are your equity has grown significantly over the last few years. Equity builds over time as home values grow and as you pay down your home loan. And, since home prices skyrocketed during the ‘unicorn’ years, you’ve likely gained more than you think.

According to the latest Equity Insights Report from CoreLogic, the average homeowner has more than $274,000 in equity right now. That much equity can help you achieve certain goals. In a recent article, Bankrate elaborates:

“While the pandemic created serious challenges, the silver lining for anyone who owned a home was the sizable equity gain. Understanding how home equity works, and how to leverage it, is important for any homeowner.”

Here are a few examples of how you can put your home equity to work for you.

1. Buy a Home That Fits Your Needs

If your current space no longer meets your needs, it might be time to think about moving to a bigger home. And if you’ve got too much space, downsizing to a smaller home could be just right. Either way, you can put your equity toward a down payment on a home that fits your changing lifestyle. A real estate agent can help you figure out how much equity you’ve got and how to use it when buying your next home.

2. Reinvest in Your Current Home

Renovations are a great option if you want to change your living space, but you aren’t yet ready to make a move. Home improvement projects give you the freedom to tailor your home to match your needs and personal style. But it’s important to consider the long-term benefits certain upgrades can bring to your home’s value. Lean on a real estate professional for the best advice on which improvement projects to prioritize in order to get the greatest return on your investment when you sell later on.

3. Pursue Personal Ambitions

Home equity can also serve as a catalyst for realizing your life-long dreams. That could mean investing in a new business venture, retirement, or funding an education. While you shouldn’t use your equity for unnecessary spending, using it responsibly for something meaningful and impactful can really make a difference in your life.

4. Understand Your Options to Avoid Foreclosure

Today the number of foreclosure filings remains below the norm, so there’s no need to fear a wave of foreclosed homes flooding the market. But unfortunately, there are still some homeowners who experience the foreclosure process each year. If you’re facing financial difficulties, having a clear understanding of your options and how your equity can help is crucial. Equity can act as a financial cushion that can be used in times of unexpected challenges or unforeseen circumstances that may disrupt your ability to make mortgage payments on time.

In an article, Freddie Mac explains it this way:

“If exiting your home is the best option for you, selling with equity may be a good option. When selling with equity, you are using the proceeds from selling your home at a higher price than the amount you owe on your mortgage to pay off your remaining mortgage debt.”

Bottom Line

Your equity can be a game changer in reinvesting in your needs, pursuing your goals, and even helping you avoid foreclosure during difficult times. If you’re unsure how much equity you have in your home, let’s connect so you can start planning your next move.

Mortgage Rates Move Toward 7%

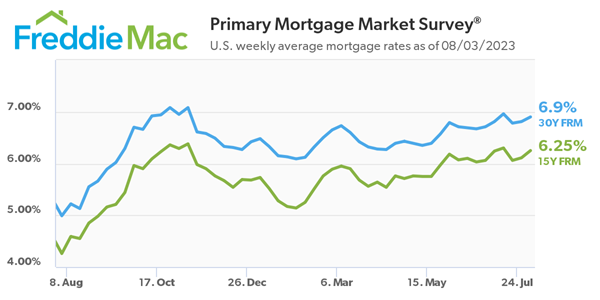

Freddie Mac today (08/03/2023) released the results of its Primary Mortgage Market Survey® (PMMS®), showing the 30-year fixed-rate mortgage (FRM) averaged 6.90 percent.

“The combination of upbeat economic data and the U.S. government credit rating downgrade caused mortgage rates to rise this week,” said Sam Khater, Freddie Mac’s Chief Economist. “Despite higher rates and lower purchase demand, home prices have increased due to very low unsold inventory.”

- 30-year fixed-rate mortgage averaged 6.90 percent as of August 3, 2023, up from last week when it averaged 6.81 percent. A year ago at this time, the 30-year FRM averaged 4.99 percent.

- 15-year fixed-rate mortgage averaged 6.25 percent, up from last week when it averaged 6.11 percent. A year ago at this time, the 15-year FRM averaged 4.26 percent.

The PMMS® is focused on conventional, conforming, fully amortizing home purchase loans for borrowers who put 20 percent down and have excellent credit.

How Inflation Impacts Mortgage Rates

When you read about the housing market in the news, you might see something about a recent decision made by the Federal Reserve (the Fed). But how does this decision affect you and your plans to buy a home? Here’s what you need to know.

The Fed is trying hard to reduce inflation. And even though there’s been 12 straight months where inflation has cooled (see graph below), the most recent data shows it’s still higher than the Fed’s target of 2%:

While you may have been hoping the Fed would stop their hikes since they’re making progress on their goal of bringing down inflation, they don’t want to stop too soon, and risk inflation climbing back up as a result. Because of this, the Fed decided to increase the Federal Funds Rate again last week. As Jerome Powell, Chairman of the Fed, says:

“We remain committed to bringing inflation back to our 2 percent goal and to keeping longer-term inflation expectations well anchored.”

Greg McBride, Senior VP, and Chief Financial Analyst at Bankrate, explains how high inflation and a strong economy play into the Fed’s recent decision:

“Inflation remains stubbornly high. The economy has been remarkably resilient, the labor market is still robust, but that may be contributing to the stubbornly high inflation. So, Fed has to pump the brakes a bit more.”

Even though a Federal Fund Rate hike by the Fed doesn’t directly dictate what happens with mortgage rates, it does have an impact. As a recent article from Fortune says:

“The federal funds rate is an interest rate that banks charge other banks when they lend one another money . . . When inflation is running high, the Fed will increase rates to increase the cost of borrowing and slow down the economy. When it’s too low, they’ll lower rates to stimulate the economy and get things moving again.”

How All of This Affects You

In the simplest sense, when inflation is high, mortgage rates are also high. But, if the Fed succeeds in bringing down inflation, it could ultimately lead to lower mortgage rates, making it more affordable for you to buy a home.

This graph helps illustrate that point by showing that when inflation decreases, mortgage rates typically go down, too (see graph below):

As the data above shows, inflation (shown in the blue trend line) is slowly coming down and, based on historical trends, mortgage rates (shown in the green trend line) are likely to follow. McBride says this about the future of mortgage rates:

“With the backdrop of easing inflation pressures, we should see more consistent declines in mortgage rates as the year progresses, particularly if the economy and labor market slow noticeably.”

Bottom Line

What happens to mortgage rates depends on inflation. If inflation cools down, mortgage rates should go down too. Let’s talk so you can get expert advice on housing market changes and what they mean for you.