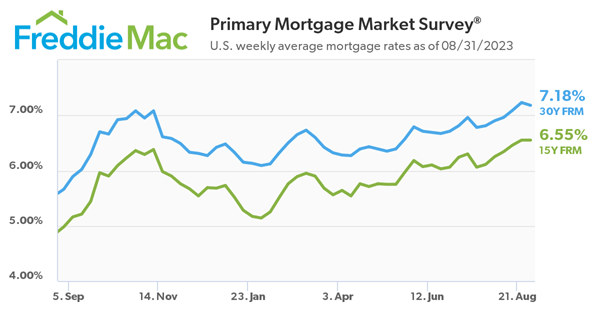

“Mortgage rates leveled off this week but remain elevated. Despite continued high rates, low inventory is keeping house prices steady,” said Sam Khater, Freddie Mac’s Chief Economist. “Recent volatility makes it difficult to forecast where rates will go next, but we should have a better gauge in September as the Federal Reserve determines their next steps regarding interest rate hikes.”

30-year fixed-rate mortgage averaged 7.18 percent as of August 31, 2023, down from last week when it averaged 7.23 percent. A year ago at this time, the 30-year FRM averaged 5.66 percent.

15-year fixed-rate mortgage averaged 6.55 percent, unchanged from last week. A year ago at this time, the 15-year FRM averaged 4.98 percent.

The PMMS® is focused on conventional, conforming, fully amortizing home purchase loans for borrowers who put 20 percent down and have excellent credit

NAR Instate Reaction: by Jessica Lautz – Deputy Chief Economist and Vice President of Research

There was virtually no change to the already elevated mortgage interest rates in the last week. Rates declined slightly from a high of 7.23% to a still high rate of 7.18%. The lack of movement is discouraging to home buyers who are also facing higher home prices.

At a rate of 7.18%, a buyer would have a monthly mortgage of $2,234 for an existing single-family home and $1,938 for an existing condo. In the West, where buyers are rebounding into the market, the typical existing-home price is $610,500, which translates into a monthly mortgage payment of $3,309. The Midwest continues to be the most affordable region to purchase a home, with a median price of $304,600—a typical monthly payment of $1,651.

Until the Fed makes the right decision on the Fed Funds Rate, buyers will continue to see higher home buying costs. These higher rates will continue to exacerbate housing inequality and limit the number of first-time and minority buyers.

Dr. Jessica Lautz is the Deputy Chief Economist and Vice President of Research at the National Association of REALTORS®.

Have you ever wondered how inflation impacts the housing market? Believe it or not, they’re connected. Whenever there are changes to one, both are affected. Here’s a high-level overview of the connection between the two.

The Relationship Between Housing Inflation and Overall Inflation

Shelter inflation is the measure of price growth specific to housing. It comes from a survey of renters and homeowners that’s done by the Bureau of Labor Statistics (BLS). The survey asks renters how much they’re paying in rent, and homeowners how much they’d rent their homes for, if they weren’t living in them.

Much like overall inflation measures the cost of everyday items, shelter inflation measures the cost of housing. And for four consecutive months, based on that survey, shelter inflation has been coming down (see graph below):

Why does this matter? Well, shelter inflation makes up about one-third of overall inflation, as measured by the Consumer Price Index (CPI). So, when shelter inflation moves, it leads to noticeable moves in overall inflation. That means the recent dip in shelter inflation might be a sign that overall inflation could fall in the months ahead.

That moderation would be a welcome sight for the Federal Reserve (the Fed). They’ve been working to get inflation under control since early 2022. While they’ve made some headway (it peaked at 8.9% in the middle of last year), they’re still trying to get to their 2% goal (the latest report is 3.3%).

Inflation and the Federal Funds Rate

What’s the Fed been doing to lower inflation? They’ve been increasing the Federal Funds Rate. That interest rate influences how much it costs banks to borrow money from each other. When inflation climbed, the Fed responded by raising the Federal Funds Rate to keep the economy from overheating.

The graph below shows the relationship between the two. Each time inflation (shown in the blue line) starts to climb, the Fed raises the Federal Funds Rate (shown in the orange line) to try to get it back to their target of 2% (see below):

The circled portion of the graph shows the most recent spike in inflation, the Fed’s actions to raise the Federal Funds Rate to fight that, and the moderation of inflation that happened in response to that hike. As inflation gets closer to the Fed’s current 2% goal, they may not need to raise the Federal Funds Rate much further.

A Brighter Future for Mortgage Rates?

So, what does all of this mean for you? While the actions coming out of the Fed don’t determine mortgage rates, they do have an impact. As Mortgage Professional America (MPA) explains:

“. . . mortgage rates and inflation are connected, however indirectly. When inflation rises, mortgage rates rise to keep up with the value of the US dollar. When inflation drops, mortgage rates follow suit.”

While no one can predict the future for mortgage rates, it’s encouraging to see the signs of moderating inflation in the economy.

Bottom Line

Whether you’re looking to buy, sell, or just stay informed about the housing market, let’s connect.

Are you putting off selling your house because you’re worried no one’s buying because of where mortgage rates are? If so, know this: the latest data shows plenty of buyers are still out there, and they’re purchasing homes today. Here’s the data to prove it.

The ShowingTime Showing Index is a measure of buyers touring homes. The graph below uses the latest numbers available and compares them to the same month in the last normal years to show just how active today’s buyers still are:

As you can see, when June 2023 numbers are stacked alongside what’s typical for the housing market at this time of year, it’s clear buyers are still active. And, they’re actually a lot more active than the norm.

If you’re wondering how this could possibly be true, it’s because buyers are getting used to higher mortgage rates and accepting them as the new reality. As Danielle Hale, Chief Economist, Realtor.com, explains:

“Interest rate hikes continue to further cut into buyers’ purchasing power, although they appear to have adapted to the higher mortgage rate environment . . .”

It’s simple. Buyers will always need to buy, and those who can afford to move at today’s rates are going to do so.

The Key Takeaway for You

While it’s true things have slowed down from the frenzy of the last couple of years, it doesn’t mean today’s market is at a standstill. The reality is: buyer traffic is still strong today. Even with today’s mortgage rates, plenty of buyers are still making their moves. So why delay your own move when there’s clearly a market for your house?

Bottom Line

Don’t put off your plans because you’re worried no one will buy your home. The opposite is true, and more buyers are more active than the norm. Let’s connect to get your house ready to sell, so it makes the best first impression possible on those eager buyers.

Even though you may feel reluctant to sell your house because you don’t want to take on a mortgage rate that’s higher than the one you have now, there’s more to consider. While the financial side of things does matter, your personal needs may actually matter just as much. As an article from Bankratesays:

“Deciding whether it’s the right time to sell your home is a very personal decision. There are numerous important questions to consider, both financial and lifestyle-based, before putting your home on the market.”

So, ask yourself this: why did I want to move in the first place?

Chances are your primary motivation wasn’t just financial in nature. Why you’re really thinking about selling likely has more to do with something changing in your life or a shift in what you need out of your house.

Reasons Homeowners Still Need To Sell Today

Let’s explore some of the most common reasons sellers are moving today. A recentarticle from Builder Online helps shed light on this. In this research, they identified the following categories:

Marriage – If you just got married, you may find you either need more space than you currently have, or the two of you want to find a new place you picked out together.

Divorce – If you’re getting separated or are divorcing your partner, chances are it’ll be difficult to live under the same roof. Selling the place you have, so you can own get your own spot, may be necessary.

Births – If your household is growing, you may need more square footage, including more bedrooms. If you’re running out of room for everyone, you may not be able to wait to move.

Deaths – If you’ve recently lost a loved one, it can be hard to spend time in that home. You may need to move for financial reasons or because you no longer need all the space.

Retirement – If you’re in the process of retiring, or you just did, you may be looking to downsize to cut costs, relocate to be closer to loved ones, or move to a dream location. In this new phase of life, your current home may not be able to deliver what you need.

You may find you share one of these top motivators. If any of these resonate with you, it may be time to move so you can find a house better suited to your changing needs. A survey from Realtor.com finds other sellers are in the same boat. It says, 1 in 4 sellers are choosing to move for personal reasons, even with current mortgage rates:

“. . . more than half of seller-buyers (56%) who are planning to sell in the next 12 months said they are waiting for rates to come down, while 25% need to sell soon for personal reasons.”

If you need to sell now because something in your own life has changed, don’t let rates hold you back from what you want. You have options to help make that move possible. You can use the equity you already have in your current home toward your next purchase. And with how much equity homeowners have right now, you may be able to finance less than you’d expect, or pay all cash to avoid borrowing at all.

Bottom Line

When you’re ready to prioritize your changing needs, let’s connect. You need an expert on your side to help you list your house and find a home that delivers on everything you’re looking for.

Generation Z (Gen Z) is eager to put down their own roots and achieve financial independence. As a result, they’re turning to homeownership. According to the latest Home Buyers and Sellers Generational Trends Report from the National Association of Realtors (NAR), 30% of Gen Z buyers transitioned straight from living under their parents’ roofs to owning their own homes.

If you’re a member of this generation, and you’re interested in pursuing your own dream of homeownership, here’s some information you may find helpful on why and where your peers are buying.

The Reasons Gen Z Want To Become Homeowners

A recent survey by Rocket Mortgageidentifies some of the top motivators driving Gen Z buyers to purchase a home:

“Of those surveyed, 34% said that starting or growing their family was their main motivation to buy a home. . . .Along with growing a family comes establishing a home base.”

Another key reason the survey says Gen Z wants to buy is because homeownership can give them more stability (20.8%). That’s because buying a home allows you to stabilize what’s typically your biggest monthly expense: your housing cost.

When you have a fixed-rate mortgage on your home, you can lock in your monthly payment for the duration of your loan, often 15 to 30 years. If you keep renting, you don’t have that same benefit, and you won’t be protected from rising housing costs.

So, if you’re ready to start a new chapter in your life or if you’re craving more stability, know that your peers feel the same way, and those motivators are why they’re turning to homeownership.

Gen Z’s Next Stop: Where Are They Making Their Moves?

If those reasons have you feeling ready to buy, here’s some information on where your peers are finding their homes that could help you with your search. According to a recent Lending Treesurvey, Gen Z buyers are focusing on more affordable areas to help boost their buying power and offset the challenges that come with today’s mortgage rates.

Many Gen Z buyers still want the convenience and excitement of city life, but also value the affordability, open air, and space more suburban areas offer. Jacob Channel, Senior Economist at LendingTree, explains:

“. . . they want to live in a city, but they also want to be close to nature.”

Locating a home that offers both of those things requires expertise. Working with a trusted real estate professional can help you find a home in your budget and desired area. Your agent will know the most affordable neighborhoods to search in. They can also highlight the amenities and features that location offers and how those are aligned with your goals. They’ll also be able to walk you through how things like remote work can help you cast a broader net for your search.

Bottom Line

If you’re a member of Gen Z and are just getting started on your homebuying journey, or if you want to learn more about the process, let’s connect. That way, you have a guide to help you find a home that fits both your lifestyle and your budget.

Freddie Mac (OTCQB: FMCC) today released the results of its Primary Mortgage Market Survey® (PMMS®), showing the 30-year fixed-rate mortgage (FRM) averaged 7.23 percent.

“This week, the 30-year fixed-rate mortgage reached its highest level since 2001 and indications of ongoing economic strength will likely continue to keep upward pressure on rates in the short-term,” said Sam Khater, Freddie Mac’s Chief Economist. “As rates remain high and supply of unsold homes woefully low, incoming data shows that existing homes sales continue to fall. However, there are slightly more new homes available, and sales of these new homes continue to rise, helping provide modest relief to the unyielding housing inventory predicament.”

30-year fixed-rate mortgage averaged 7.23 percent as of August 24, 2023, up from last week when it averaged 7.09 percent. A year ago at this time, the 30-year FRM averaged 5.55 percent.

15-year fixed-rate mortgage averaged 6.55 percent, up from last week when it averaged 6.46 percent. A year ago at this time, the 15-year FRM averaged 4.85 percent.

The PMMS® is focused on conventional, conforming, fully amortizing home purchase loans for borrowers who put 20 percent down and have excellent credit.

Dr. Jessica Lautz is the Deputy Chief Economist and Vice President of Research at the National Association of REALTORS®.

Mortgage rates jumped this week to 7.23% from 7.09% last week, the highest monthly mortgage payment since June 1, 2001, when they were 7.24%.

From June 1991 through May 2001, mortgage interest rates averaged 7.81%. Consumers may have felt comfortable taking on a mortgage in the 7% range. However, there’s a big difference between 22 years ago and today: home prices and inventory were more in line with wages and the population then. In June 2001, there were 2.11 million existing homes on the market. In data for July 2023, there were just 1.11 existing homes in the market.

The highest interest rate in 22 years translates into a monthly payment for the typical existing single-family home of $2,246 and a $1,948 payment for a condo. New home sales are on the rise while existing-home inventory is limited. However, the sales price is about $30,000 more than the typical existing home, which means a monthly mortgage payment of $2,379 for the typical new home. Until rates come down, this will hurt buyers’ opportunities to enter the market and the willingness of sellers to make a needed move.

There’s been talk about a recession for quite a while now. But the economy has been remarkably resilient. Why? One reason is employment and wages have stayed strong. Let’s look at the latest information on each one and why both are good news if you’re thinking about selling your house.

More Jobs Are Being Created

Instead of facing the job losses typical of any recession, the economy has been growing and adding jobs. According to the Bureau of Labor Statistics (BLS), 187,000 jobs were created in July, which is up from the 185,000 created in June. That means more people are finding work. In fact, so many jobs are being added that the unemployment rate is far lower than the long-term average of 5.7% (see graph below):

A low unemployment rate means that most people who want to work are finding jobs. When people have jobs, they have steady incomes – and that can help set them up to consider homeownership.

People Are Making More Money

And data also shows hourly earnings have been going up pretty steadily over the past few years (see graph below):

When wages rise, people have more money that they could save or use toward buying a home. This increase in income helps offset some of the affordability challenges in the housing market today. Affordability depends on three main factors: wages, home prices, and mortgage rates. With higher home prices and mortgage rates right now, Builder Onlinesummarizes how growing wages can help:

“The housing market has been a beneficiary of the strong economy and labor market. Many of those employed have saved money over the past few years and used those funds toward a down payment on a home.”

If you’re thinking about selling your house, a strong job market, growing wages, and the resulting buyer demand is fantastic news. It means there’s a larger pool of potential buyers out there who are in a position to pursue their dreams of homeownership.

Bottom Line

With more jobs and rising wages creating eager buyers, there’s a lot going in your favor. Let’s connect so you have someone who can guide you through the process of selling your house, from setting the right price to getting your home ready to show.

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link