Are you one of those potential homebuyers who is struggling with whether now is a good time to buy. You’ve been reading the news reports and hearing conflicting things from friends, relatives and others about whether you should buy now or wait. When I get the question – should I buy now or wait – I try to learn more about the person or couple’s desire to find a new place. I also ask them about what steps they’ve taken to prepare themselves to buy.

And that conversation leads us to why now may be the time to buy.

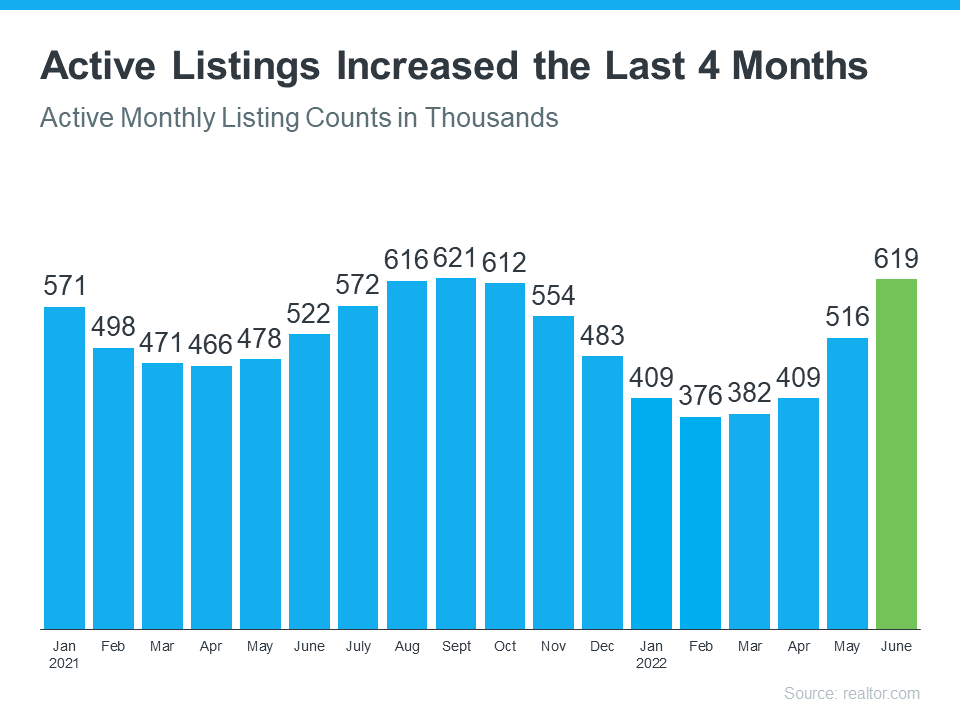

There are more homes for sale today than at any time last year. So, if you tried to buy a home last year and were outbid or out priced, now may be your opportunity. The number of homes for sale in the U.S. has been growing over the past four months as rising mortgage rates help slow the frenzy the housing market saw during the pandemic.

Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), explains why the shifting market creates a window of opportunity for you:

“This is an opportunity for people with a secure job to jump into the market, when other people are a little hesitant because of a possible recession. . . They’ll have fewer buyers to compete with.”

Two Reasons There Are More Homes for Sale

The first reason the market is seeing more homes available for sale is the number of sales happening each month has decreased. This slowdown has been caused by rising mortgage rates and rising home prices, leading many to postpone or put off buying. The graph below uses data from realtor.com to show how active real estate listings have risen over the past four months as a result.

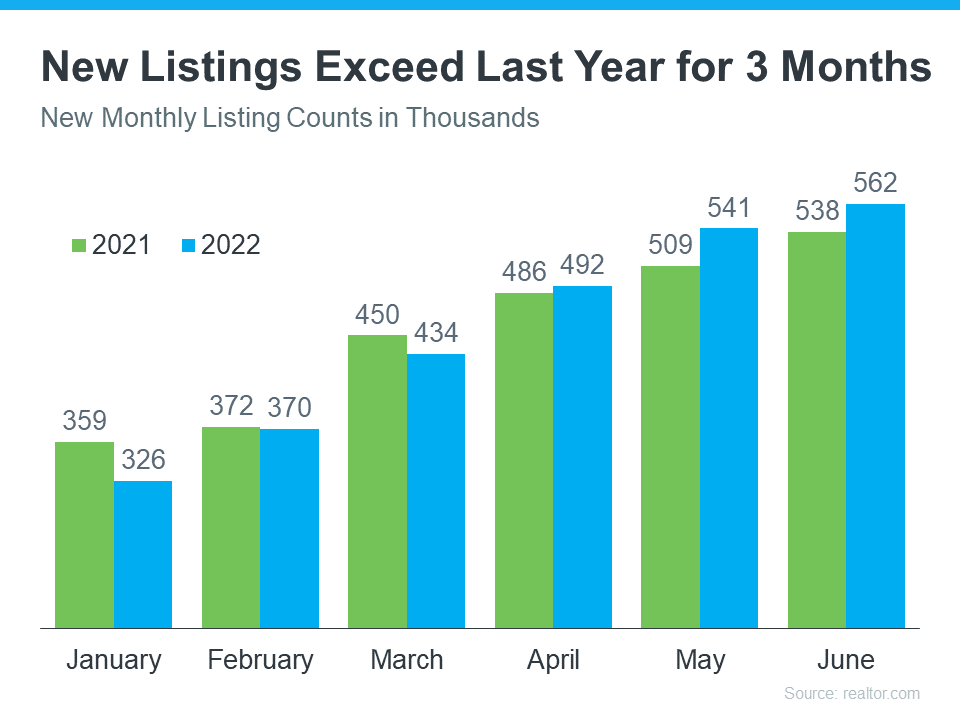

The second reason the market is seeing more homes available for sale is because the number of people selling their homes is also rising. The graph below outlines new monthly listings coming onto the market compared to last year. As the graph shows, for the past three months, more people have put their homes on the market than the previous year.

Bottom Line

The number of homes for sale across the country is growing, and that means more options for those thinking about buying a home. This is the opportunity many have been waiting for who were outbid or out priced last year.

This article provide by Keeping Current Matters. The information contained, and the opinions expressed, in this article are not intended to be construed as investment advice. Keeping Current Matters, Inc. does not guarantee or warrant the accuracy or completeness of the information or opinions contained herein. Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision. Keeping Current Matters, Inc. will not be liable for any loss or damage caused by your reliance on the information or opinions contained herein.

he latest date from Federal government agencies continues to show a slowdown in the housing market. The US Census Department and HUD reported today sales of new single family homes in June fell 8,1 per cent from the previous month of May. The report said that new single-family home sales were down 17.4 per cent from June of 2021.

Mounting evidence shows a slowdown in housing market activity. Is this a reason for pause? Or, does it represent a window of opportunity?

Mortgage rates are much higher today than they were at the beginning of the year, and that’s had a clear impact on the housing market. As a result, the market is seeing a shift back toward the range of pre-pandemic levels for buyer demand and home sales.

But the transition back toward pre-pandemic levels isn’t a bad thing. In fact, the years leading up to the pandemic were some of the best the housing market has seen. That’s why, as the market undergoes this shift, it’s important to compare today not to the abnormal pandemic years, but to the most recent normal years to show how the current housing market is still strong.

Higher Mortgage Rates Are Moderating the Housing Market

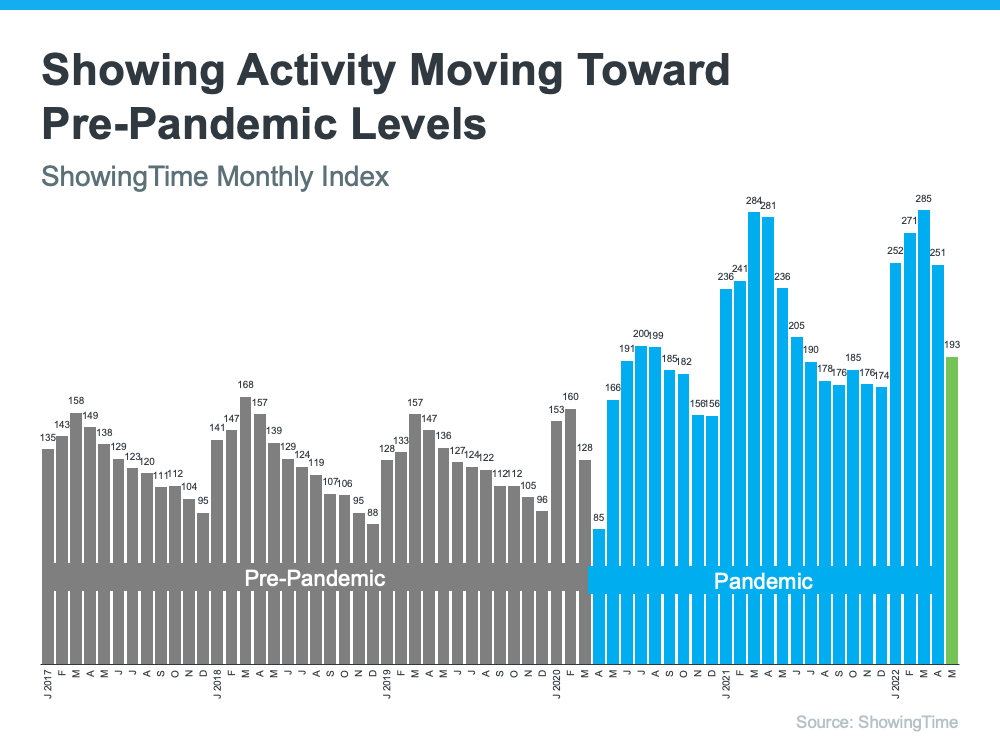

The ShowingTime Showing Index tracks the traffic of home showings according to agents and brokers. It’s also a good indication of buyer demand over time. Here’s a look at their data going back to 2017 (see graph below):

Here’s a breakdown of the story this data tells:

The 2017 through early 2020 numbers (shown in gray) give a good baseline of pre-pandemic demand. The steady up and down trends seen in each of these years show typical seasonality in the market.

The blue on the graph represents the pandemic years. The height of those blue bars indicates home showings skyrocketed during the pandemic.

The most recent data (shown in green), indicates buyer demand is moderating back toward more pre-pandemic levels.

This shows that buyer demand is coming down from levels seen over the past two years, and the frenzy in real estate is easing because of higher mortgage rates. For you, that means buying your next home should be less challenging than it would’ve been during the pandemic because there is more inventory available.

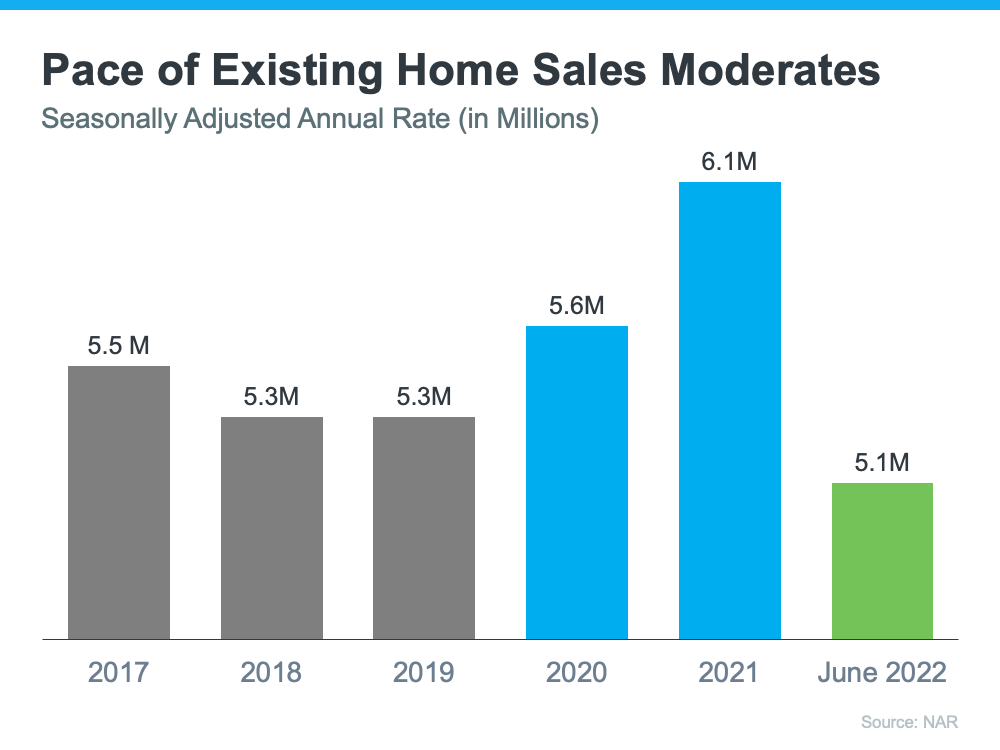

Higher Mortgage Rates Slow the Once Frenzied Pace of Home Sales

As mortgage rates started to rise this year, other shifts began to occur too. One additional example is the slowing pace of home sales. Using data from the National Association of Realtors (NAR), here’s a look at existing home sales going all the way back to 2017. Much like the previous graph, a similar trend emerges (see graph below):

Again, the data paints a picture of the shift:

The pre-pandemic years (shown in gray) establish a baseline of the number of existing home sales in more typical years.

The pandemic years (shown in blue) exceeded the level of sales seen in previous years. That’s largely because low mortgage rates during that time spurred buyer demand and home sales to new heights.

This year (shown in green), the market is feeling the impact of higher mortgage rates and that’s moderating buyer demand (and by extension home sales). That’s why the expectation for home sales this year is closer to what the market saw in 2018-2019.

Why Is All of This Good News for You?

Both of those factors have opened up a window of opportunity for homeowners looking to move and for buyers looking to purchase a home. As demand moderates and the pace of home sales slows, housing inventory is able to grow – and that gives you more options for your home search.

So don’t let the headlines about the market cooling or moderating scare you. The housing market is still strong; it’s just easing off from the unsustainable frenzy it saw during the height of the pandemic – and that’s a good thing. It opens up new opportunities for you to find a home that meets your needs.

Bottom Line

The housing market is undergoing a shift because of higher mortgage rates, but the market is still strong. If you’ve been looking to buy a home over the last couple of years and it felt impossible to do, now may be your opportunity. Buying a home right now isn’t easy, but there is more opportunity for those who are looking.

This article includes reporting by Keeping Current Matters.The information contained, and the opinions expressed, in this article are not intended to be construed as investment advice. Keeping Current Matters, Inc. does not guarantee or warrant the accuracy or completeness of the information or opinions contained herein. Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision. Keeping Current Matters, Inc. will not be liable for any loss or damage caused by your reliance on the information or opinions contained herein.

Let’s connect so you have the latest information on available homes in our area.

This article provided by Keeping Current Matters. The information contained, and the opinions expressed, in this article are not intended to be construed as investment advice. Keeping Current Matters, Inc. does not guarantee or warrant the accuracy or completeness of the information or opinions contained herein. Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision. Keeping Current Matters, Inc. will not be liable for any loss or damage caused by your reliance on the information or opinions contained herein.

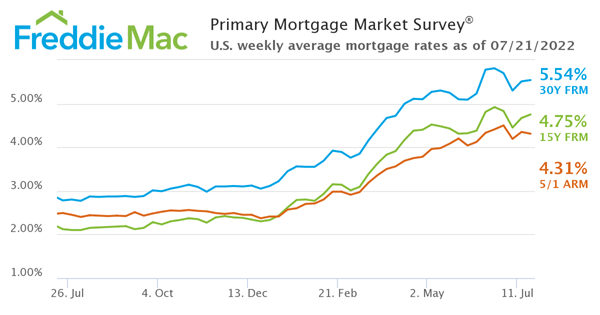

Freddie Mac (OTCQB: FMCC) today released the results of its Primary Mortgage Market Survey® (PMMS®) for the week ending July 21, 2022. The survey showed the 30-year fixed-rate mortgage (FRM) averaged 5.54 percent for the week.

“The housing market remains sluggish as mortgage rates inch up for a second consecutive week,” said Sam Khater, Freddie Mac’s Chief Economist. “Consumer concerns about rising rates, inflation and a potential recession are manifesting in softening demand. As a result of these factors, we expect house price appreciation to moderate noticeably.”

30-year fixed-rate mortgage averaged 5.54 percent with an average 0.8 point as of July 21, 2022, up from last week when it averaged 5.51 percent. A year ago at this time, the 30-year FRM averaged 2.78 percent.

15-year fixed-rate mortgage averaged 4.75 percent with an average 0.8 point, up from last week when it averaged 4.67 percent. A year ago at this time, the 15-year FRM averaged 2.12 percent.

5-year Treasury-indexed hybrid adjustable-rate mortgage (ARM) averaged 4.31 percent with an average 0.3 point, down from last week when it averaged 4.35 percent. A year ago at this time, the 5-year ARM averaged 2.49 percent.

For more information on daily mortgage interest rate movements, check with your mortgage lender. You can also check online sites such as Mortgage News Daily.

Do you think home prices will fall? Over the last two years, the rate of home prices appreciated at a dramatic pace. While that led to incredible equity gains for homeowners, it’s also caused some buyers to wonder if home prices will fall. It’s important to know the housing market isn’t a bubble about to burst, and home price growth is supported by strong market fundamentals.

To understand why price declines are unlikely, it’s important to explore what caused home prices to rise so much recently, and where experts say home prices are headed. Here’s what you need to know.

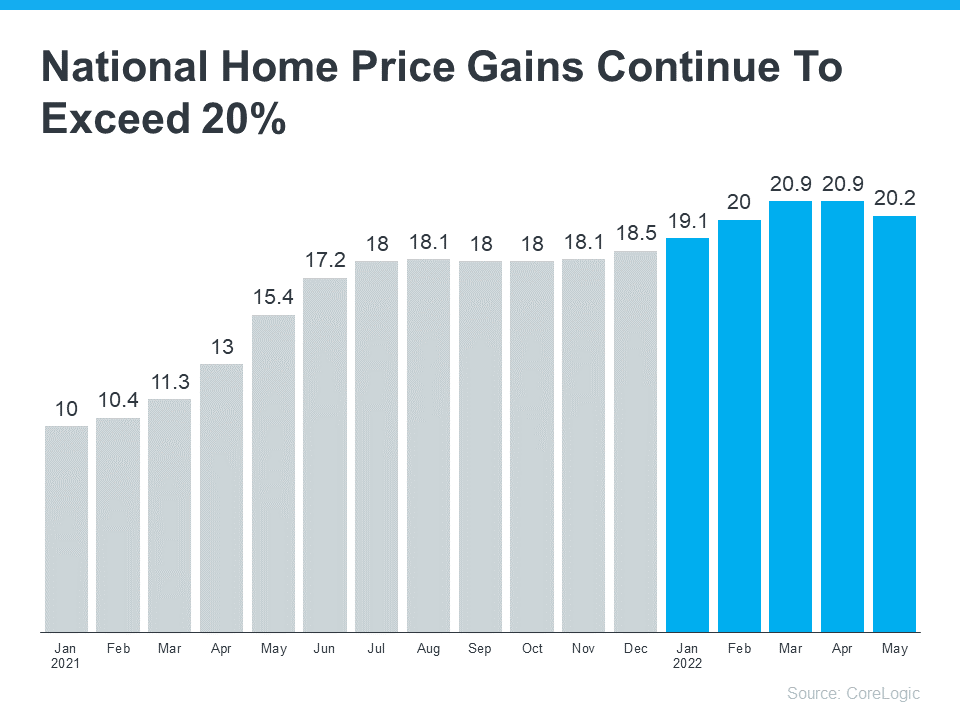

Home Prices Rose Significantly in Recent Years

The graph below uses the latest data from CoreLogic to illustrate the rise in home prices over the past year and a half. The gray bars represent the dramatic increase in the rate of home price appreciation in 2021. The blue bars show home prices are still rising in 2022, but not as quickly:

You might be asking: why did home prices climb so much last year? It’s because there were more buyers than there were homes for sale. That imbalance put upward pressure on home prices because demand was extremely high, and supply was record low.

Where Experts Say Prices Will Go from Here

While housing inventory is increasing and buyer demand is softening today, there’s still a shortage of homes available for sale. That’s why the market is seeing ongoing price appreciation. Mark Fleming, Chief Economist at First American, explains it like this:

“. . .we’re still well below normal levels of inventory and that’s why even with the pullback in demand, we still see house prices appreciating. While there is more inventory, it’s still not enough.”

As a result, experts are projecting a more moderate rate of home price appreciation this year, which means home prices will continue rising, but at a slower pace. That doesn’t mean prices are going to fall. As Selma Hepp, Deputy Chief Economist at CoreLogic, says:

“The current home price growth rate is unsustainable, and higher mortgage rates coupled with more inventory will lead to slower home price growth but unlikely declines in home prices.”

In other words, even with higher mortgage rates, moderating buyer demand, and more homes for sale, experts say home price appreciation will slow, but prices won’t decline.

If you’re planning to buy a home, that means you shouldn’t wait for home prices to drop to make your purchase. Instead, buying today means you can get ahead of future price increases, and benefit from the rise in prices in the form of home equity.

Bottom Line

Home prices skyrocketed in recent years because there was more demand than supply. As the market shifts, experts aren’t forecasting a drop in prices, just a slowdown in the rate of price growth. To understand what’s happening with home prices in our area, let’s connect today.

This article was provided by Keeping Current Matters.The information contained, and the opinions expressed, in this article are not intended to be construed as investment advice. Keeping Current Matters, Inc. does not guarantee or warrant the accuracy or completeness of the information or opinions contained herein. Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision. Keeping Current Matters, Inc. will not be liable for any loss or damage caused by your reliance on the information or opinions contained herein.

While the Federal Reserve is working hard to bring down inflation, the latest data shows the inflation rate is still going up. You no doubt are feeling the pinch on your wallet at the gas pump or the grocery store, but that news may also leave you wondering: should I still buy a home right now?

Greg McBride, Chief Financial Analyst at Bankrate, explains how inflation is affecting the housing market:

“Inflation will have a strong influence on where mortgage rates go in the months ahead. . . . Whenever inflation finally starts to ease, so will mortgage rates — but even then, home prices are still subject to demand and very tight supply.”

No one knows how long it’ll take to bring down inflation, and that means the future trajectory of mortgage rates is also unclear. While that uncertainty isn’t comfortable, here’s why both inflation and mortgage rates are important for you and your homeownership plans.

When you buy a home, the mortgage rate and the price of the home matter. Higher mortgage rates impact how much you’ll pay for your monthly mortgage payment – and that directly affects how much you can comfortably afford. And while there’s no denying it’s more expensive to buy and finance a home this year than it was last year, it doesn’t mean you should pause your search. Here’s why.

Homeownership Is Historically a Great Hedge Against Inflation

In an inflationary economy, prices rise across the board. Historically, homeownership is a great hedge against those rising costs because you can lock in what’s likely your largest monthly payment (your mortgage) for the duration of your loan. That helps stabilize some of your monthly expenses. Not to mention, as home prices continue to appreciate, your home’s value will too. That’s why Mark Cussen, Financial Writer at Investopedia, says:

“Real estate is one of the time-honored inflation hedges. It’s a tangible asset, and those tend to hold their value when inflation reigns, unlike paper assets. More specifically, as prices rise, so do property values.”

Also, no one is calling for homes to lose value. As Selma Hepp, Deputy Chief Economist at CoreLogic, says:

“The current home price growth rate is unsustainable, and higher mortgage rates coupled with more inventory will lead to slower home price growth but unlikely declines in home prices.”

In a nutshell, your home search doesn’t have to go on hold because of rising inflation or higher mortgage rates. There’s more to consider when it comes to why you want to buy a home. In addition to shielding yourself from the impact of inflation and growing your wealth through ongoing price appreciation, there are other reasons to buy a home right now like addressing your changing needs and so much more.

Bottom Line

Homeownership is one of the best decisions you can make in an inflationary economy. You get the benefit of the added security of owning your home in a time when experts are forecasting prices to continue to rise.

This article provided by Keeping Current Matters. The information contained, and the opinions expressed, in this article are not intended to be construed as investment advice. Keeping Current Matters, Inc. does not guarantee or warrant the accuracy or completeness of the information or opinions contained herein. Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision. Keeping Current Matters, Inc. will not be liable for any loss or damage caused by your reliance on the information or opinions contained herein.

If you’re planning to buy a home this year, you might have heard that pre-approval is a necessary step to take before starting out on your journey. But why is that? And is it still important in today’s shifting market?

The truth is, getting a pre-approval letter from your lender is critical, and when it comes to your home search, it can be a game changer in so many ways.

To better understand why, it’s important to know what pre-approval is. Freddie Macdefines the process like this:

“A pre-approval is an indication from your lender that they are willing to lend you a certain amount of money to buy your future home. The lender you work with will provide you with a pre-approval letter, which is an official document that states the maximum amount they are willing to lend you, . . .”

Put simply, pre-approval from a lender helps you understand your true price range and how much money you can borrow for your loan. That can make it easier when you set out to search for homes. And since you’ll know what you’re approved for, it’ll also help once it’s time to submit an offer on the home of your dreams.

Another added benefit is that pre-approval lets the seller know you’re qualified to buy their house. Paul Centopani, Editor for the Mortgage Reports, explains:

“. . . most sellers won’t even consider an offer unless the buyer is pre-approved at the right price point. Sellers and their agents want to know you’re ready and able to finance your offer amount. So you’ll want to have your preapproval teed up as soon as you’re serious about bidding on a home you like.”

Every advantage you can gain as a buyer is crucial in a market that’s constantly changing. You’re going to need guidance to navigate these waters, so it’s important to have a team of professionals, such as a real estate advisor and trusted lender, on your side. They’ll help make sure you’re ready to put your best foot forward.

Bottom Line

Getting pre-approved for a mortgage helps you better understand what you can borrow and shows sellers you’re serious about purchasing their home. Let’s connect so you have the tools you need to succeed as a homebuyer in today’s shifting market.

This article was provided by Keeping Current Matters.The information contained, and the opinions expressed, in this article are not intended to be construed as investment advice. Keeping Current Matters, Inc. does not guarantee or warrant the accuracy or completeness of the information or opinions contained herein. Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision. Keeping Current Matters, Inc. will not be liable for any loss or damage caused by your reliance on the information or opinions contained herein.

I’ve heard the question. And, quite frankly I’ve asked the question. Where will I go if I sell my house today?

If you put a pause on your home search because you weren’t sure where you’d go once you sold your house, it might be a good time to get back into the market. That’s because today’s market is undergoing a shift, and the supply of homes for sale is increasing as a result. That means you may have a better chance of finding a home that will meet your current needs. Here are some options to consider.

Buying an Existing Home Can Give You That Lived-in Charm

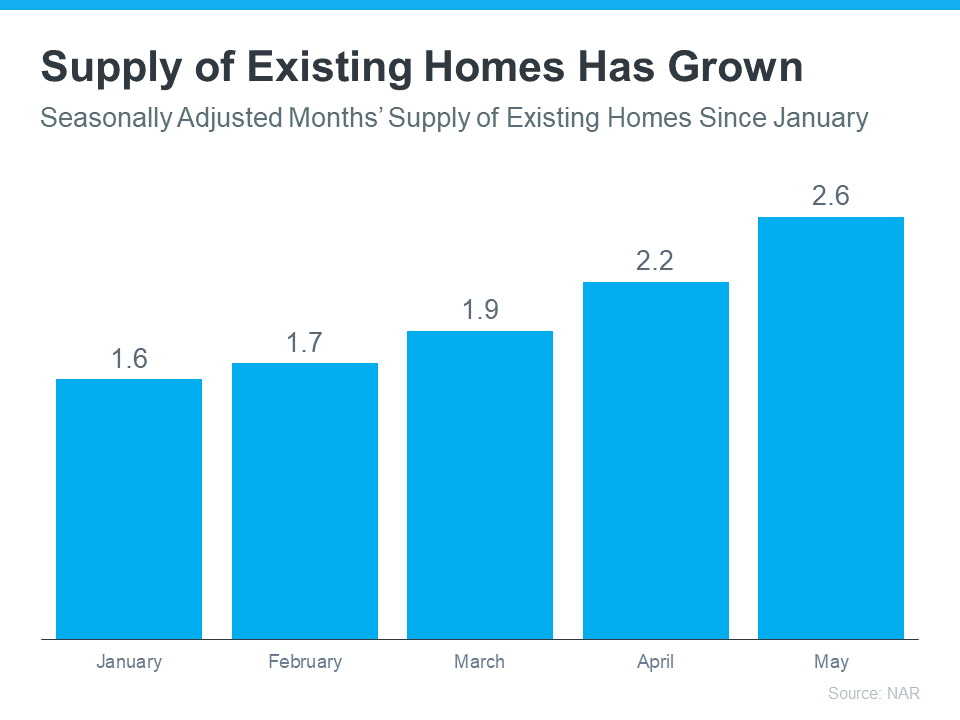

According to the National Association of Realtors (NAR), the supply of existing homes (a home that’s been previously owned) has steadily increased since the beginning of the year. The graph below indicates inventory levels are rising, and that’s largely due to more homes coming onto the market and the pace of sales slowing:

As the graph shows, if you’re looking for a home with lived-in charm, supply is rising, and that’s great news for you.

Danielle Hale, Chief Economist for realtor.com, gives insight into why more homeowners are listing their homes and adding to the growing supply of existing homes today:

“Home sellers in many markets across the country continue to benefit from rising home prices and fast-selling homes. That’s prompted a growing number of homeowners to sell homes this year compared to last, giving home shoppers much needed options. We’ve seen more homes come up for sale this year compared to last year . . .”

There are several benefits to buying an existing home. Many buyers want to purchase a home with history, and the character of older houses is hard to reproduce. Existing homes can often be part of an established neighborhood featuring mature landscaping that can give you additional privacy and boost your curb appeal.

Plus, timing can be a consideration as well. With an existing home, you can move in based on the timeline you agree to with the sellers, rather than building a new home and waiting for construction to finish. This is something to keep in mind, especially if you need to move sooner rather than later.

Just remember, while more sellers are listing their homes, supply is still low overall. That means you’ll have more options to choose from as you search for your next home, but you’ll still need to be prepared for a fast-moving market.

Purchasing a Newly Built or Under Construction Home Means Brand New Everything

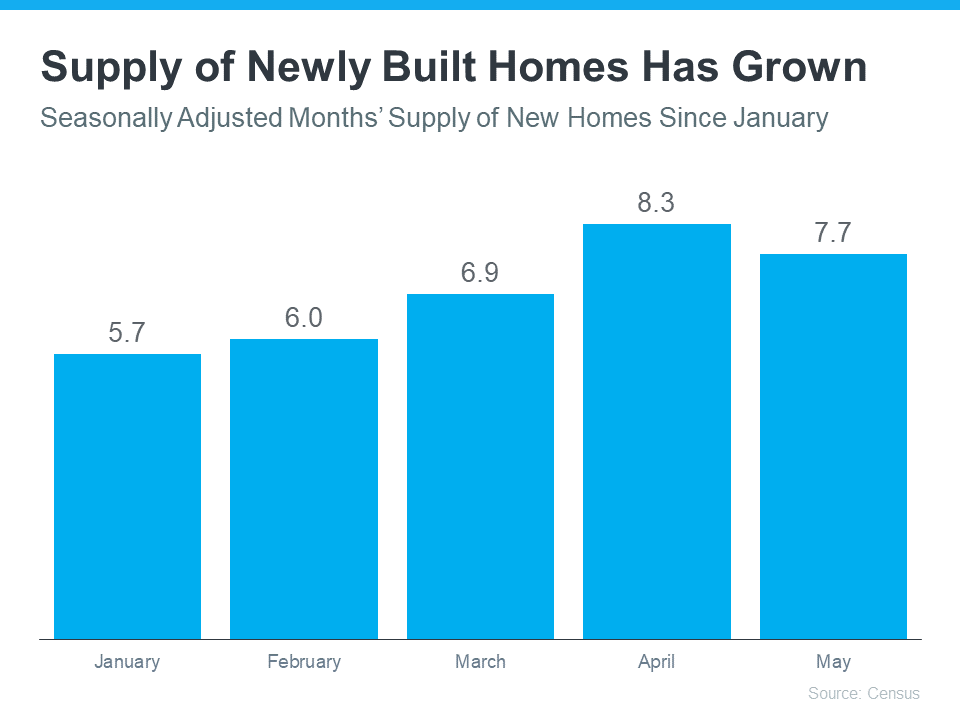

Census data shows there’s an increasing number of new homes available for sale. It includes homes that are under construction, soon to be completed, and fully built. As the graph below highlights, the supply of new homes for sale has also grown this year:

When building a new home, you can create your perfect living space and customize it to your lifestyle. That could mean everything from requesting energy efficient options to specific design features. Plus, you’ll have the benefit of all new appliances, windows, roofing, and more. These can all help lower your energy costs, which can add up to significant savings over time.

The lower maintenance that comes with a newer home is another great advantage. When you have a new home, you likely won’t have as many little repairs to tackle, like leaky faucets, shutters to paint, and other odd jobs around the house. And with new construction, you’ll also have warranty options that may cover portions of your investment for the first few years.

Keep in mind, purchasing a new home could mean waiting a considerable amount of time before you can move. Robert Dietz, Chief Economist and Senior Vice President for Economics and Housing Policy at the National Association of Home Builders (NAHB), explains:

“New single-family home inventory remained elevated at a 7.7 months’ supply. . . . However, only 8.3% of new home inventory is completed and ready to occupy. The remaining have not started construction (25.9%) or are currently under construction.”

That’s an important factor when making your decision and one you should discuss with a trusted real estate advisor. They’ll help you think through all the pros and cons of both new and existing homes to help you arrive at your best decision.

Bottom Line

With the supply of homes for sale rising, you have options for your next home no matter what your preferences are. If you have questions or want help deciding what’s best for you, let’s connect and start the conversation today.

This article provided by Keeping Current Matters. The information contained, and the opinions expressed, in this article are not intended to be construed as investment advice. Keeping Current Matters, Inc. does not guarantee or warrant the accuracy or completeness of the information or opinions contained herein. Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision. Keeping Current Matters, Inc. will not be liable for any loss or damage caused by your reliance on the information or opinions contained herein.

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

![Three Reasons To Buy a Home in Today’s Shifting Market [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2022/07/28132341/20220729-MEM-1046x1709.png)

![Great News About Housing Inventory [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2022/07/21111905/20220722-MEM-1046x2035.jpg)