Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

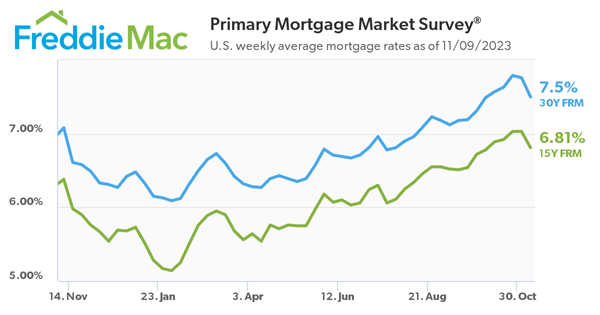

Freddie Mac today released the results of its Primary Mortgage Market Survey® (PMMS®), showing the 30-year fixed-rate mortgage (FRM) averaged 7.5 percent.

“As Treasury yields decline, the 30-year fixed-rate mortgage dropped a quarter of a percent, the largest one-week decrease since last November,” said Sam Khater, Freddie Mac’s Chief Economist. “Incoming data show that household debt continues to rise, primarily due to mortgage, credit card and student loan balances. Many consumers are feeling strained by the high cost of living, so unless mortgage rates decrease significantly, the housing market will remain stagnant.”

- 30-year fixed-rate mortgage averaged 7.5 percent as of November 9, 2023, down from last week when it averaged 7.76 percent. A year ago at this time, the 30-year FRM averaged 7.08 percent.

- 15-year fixed-rate mortgage averaged 6.81 percent, down from last week when it averaged 7.03 percent. A year ago at this time, the 15-year FRM averaged 6.38 percent.

The PMMS® is focused on conventional, conforming, fully amortizing home purchase loans for borrowers who put 20 percent down and have excellent credit.

Instant Reaction from Dr. Jessica Lautz the Deputy Chief Economist and Vice President of Research at the National Association of REALTORS®.

Housing consumers have a bit of relief this week as the 30-year fixed mortgage interest rate dipped lower to 7.5%, falling one-quarter of a percent and hitting the lowest point in a month.

Despite this, home buyers are facing a more expensive housing market than last year. Based on NAR’s Quarterly Report released today, home prices for single-family existing homes increased annually in 82% of markets. With elevated mortgage interest rates and the rise in home prices, buyers are facing the most challenging affordability conditions since the Housing Affordability Index started in 1989.

The 10-year treasury has also shown declines over the last week, averaging 4.5% after brushing 5%. The spread continues to be wider than the historical norm, with room to narrow, which would further help home buyers.

The U.S. needs more affordable housing inventory, and the Fed should strongly consider reducing the Fed Funds rate. In this housing market, homeowners continue to be the winners and gain the housing equity that would-be buyers desperately want.